A recent disclosure regarding a major shareholder equity change at PharmaResearch Co., Ltd. (214450) has sparked interest across the investment community. This detailed PharmaResearch investment analysis dissects the recent 0.42%p increase in major shareholder equity, evaluates the company’s robust H1 2025 performance, and explores the fundamental strengths and potential risks that will define its future trajectory. Is this a signal of bolstered management confidence, and what does it mean for prospective investors?

We will unpack the company’s leadership in regenerative medicine, its stellar financial health, and the strategic investments shaping its growth. This comprehensive guide provides the critical insights necessary to understand the current state and future potential of this healthcare leader.

Event Overview: Deconstructing the Shareholding Change

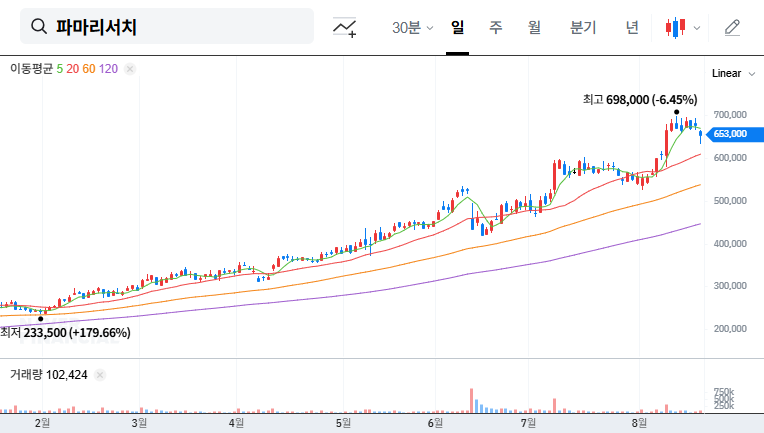

On November 12, 2025, a regulatory filing revealed a shift in the ownership structure of PharmaResearch. According to the Report on the Status of Major Shareholdings, the collective stake of major shareholder Mr. Sang-soo Jung and his special affiliates increased from 41.12% to 41.54%. You can view the Official Disclosure here.

While a 0.42 percentage point increase may seem minor, its stated purpose—to influence management rights—makes it significant. This move suggests a consolidation of control and a strong vote of confidence from the company’s core leadership. The change was attributed to several factors:

- •On-market trading activities by special affiliates.

- •The execution of major contracts involving these affiliates.

- •Adjustments reflecting changes in the total number of outstanding shares.

Interestingly, this overall increase occurred despite a small sale of 500 shares by a special affiliate, Mr. Rae-joon Jung, highlighting a net accumulation by the controlling group.

Unpacking PharmaResearch’s Robust Fundamentals (H1 2025)

Core Business: A Pioneer in Regenerative Medicine

PharmaResearch has carved out a dominant niche in the regenerative bio-medicine sector, built upon its proprietary PDRN/PN-based technology. This technology, derived from salmon DNA, is a cornerstone of tissue regeneration and anti-aging treatments. The company’s diverse portfolio, which includes medical devices like Rejuran and Conjurun, pharmaceuticals, and cosmetics, leverages this core competency. This technological moat, combined with the powerful macro-trend of an aging global population seeking anti-aging solutions, positions PharmaResearch for sustained long-term growth. For more on the science, check out this overview of polynucleotide technology from a leading scientific journal.

Stellar Financial Performance

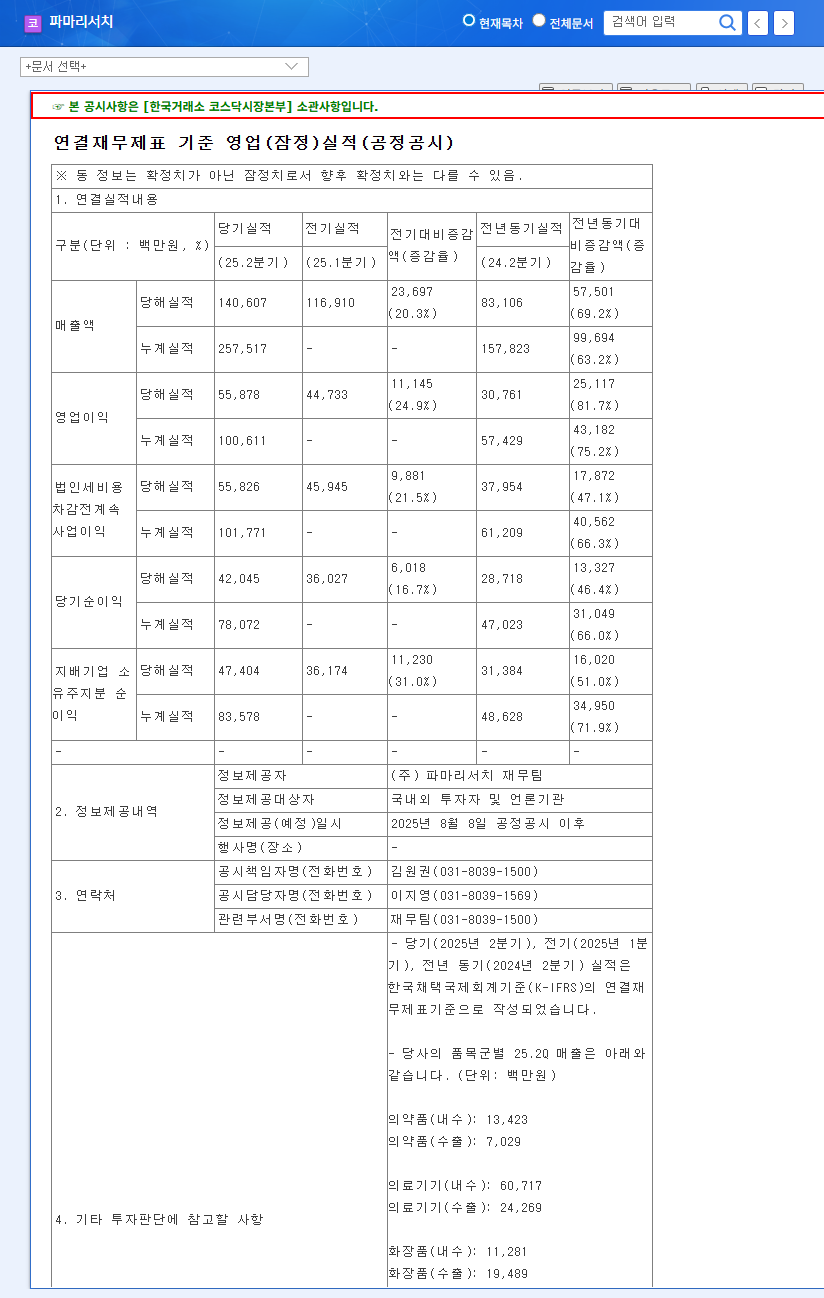

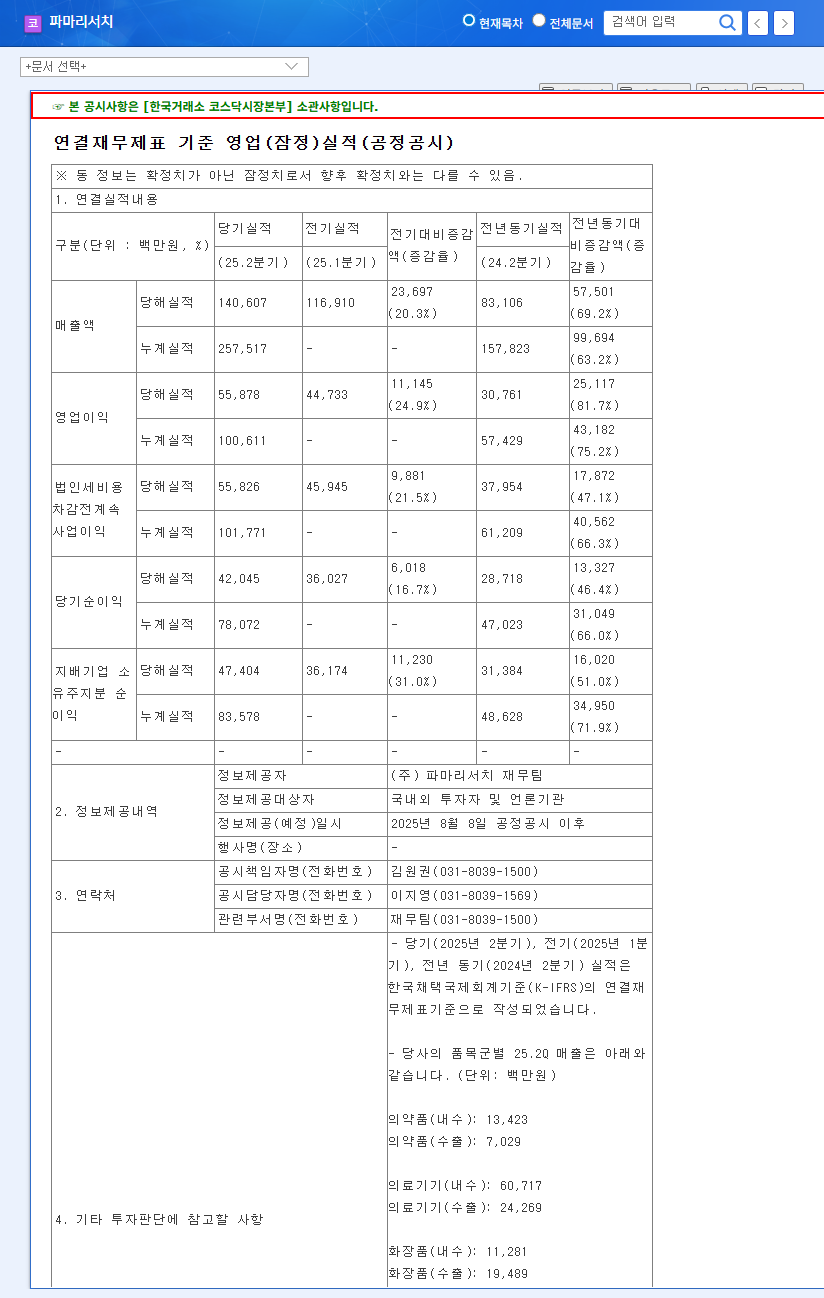

The financial results for the first half of 2025 underscore the company’s operational excellence. PharmaResearch reported revenue of KRW 257.5 billion, a remarkable 30% increase year-over-year. The medical device segment was the primary growth engine, contributing 60% of total revenue.

Even more impressive is the company’s operating profit margin of 39.1%, a figure that far surpasses many industry peers and demonstrates exceptional profitability and cost control.

Furthermore, a solid balance sheet with total assets of KRW 923.2 billion against total liabilities of KRW 285.7 billion, alongside a healthy cash reserve, indicates strong financial stability and liquidity for future investments.

Strategic Investments in Future Growth

PharmaResearch is actively reinvesting its profits into future growth drivers. The company dedicates approximately 6.62% of its revenue to Research & Development, focusing on securing new pipelines like IRC_D105 and IRC_M126. This commitment to innovation is crucial for long-term value creation. Paired with ongoing investments in expanding production facilities, the company is preparing for increased global demand. You can explore our deep dive into the global anti-aging market to understand the scale of this opportunity.

A Balanced View: Opportunities and Risks

A thorough PharmaResearch investment analysis must weigh the positive catalysts against potential headwinds.

Positive Factors and Opportunities

The increase in PharmaResearch shareholding by its leadership strengthens management stability, allowing for consistent execution of its long-term vision. This internal confidence, backed by powerful financial performance and a strong market position, signals a robust foundation. The stable macroeconomic environment, with normalizing interest rates and predictable logistics costs, further supports this positive outlook.

Potential Risks to Monitor

Investors should remain vigilant of certain risks. The ongoing lawsuit related to PharmaResearch Bio Co., Ltd. could introduce short-term stock price volatility. Additionally, while a weaker Korean Won can boost export competitiveness, it also raises the cost of imported raw materials, potentially squeezing margins if not managed carefully. Finally, the success of the R&D pipeline is not guaranteed and requires continuous monitoring.

Conclusion: Investment Thesis for PharmaResearch

PharmaResearch presents a compelling case built on solid fundamentals: proprietary technology, a diversified and high-growth portfolio, and exceptional financial discipline. The recent shareholding increase by major stakeholders is a reaffirmation of their commitment and belief in the company’s bright future.

From a mid-to-long-term perspective, the company demonstrates significant growth potential. However, investors should balance this optimism by closely monitoring legal proceedings, foreign exchange fluctuations, and progress within the R&D pipeline. As always, all investment decisions should be made based on individual research and risk tolerance.