In a strategic pivot that has captured the market’s attention, GREEN LIFESCIENCE CO., LTD. has announced its formal entry into the booming AI semiconductor material sector. This move is substantiated by a massive supply contract, signaling a potential new era of growth beyond its traditional pharmaceutical business. This analysis will dissect the contract’s details, evaluate the company’s fundamentals, and explore the future trajectory for investors considering GREEN LIFESCIENCE stock.

The Landmark ₩13.6 Billion Supply Contract

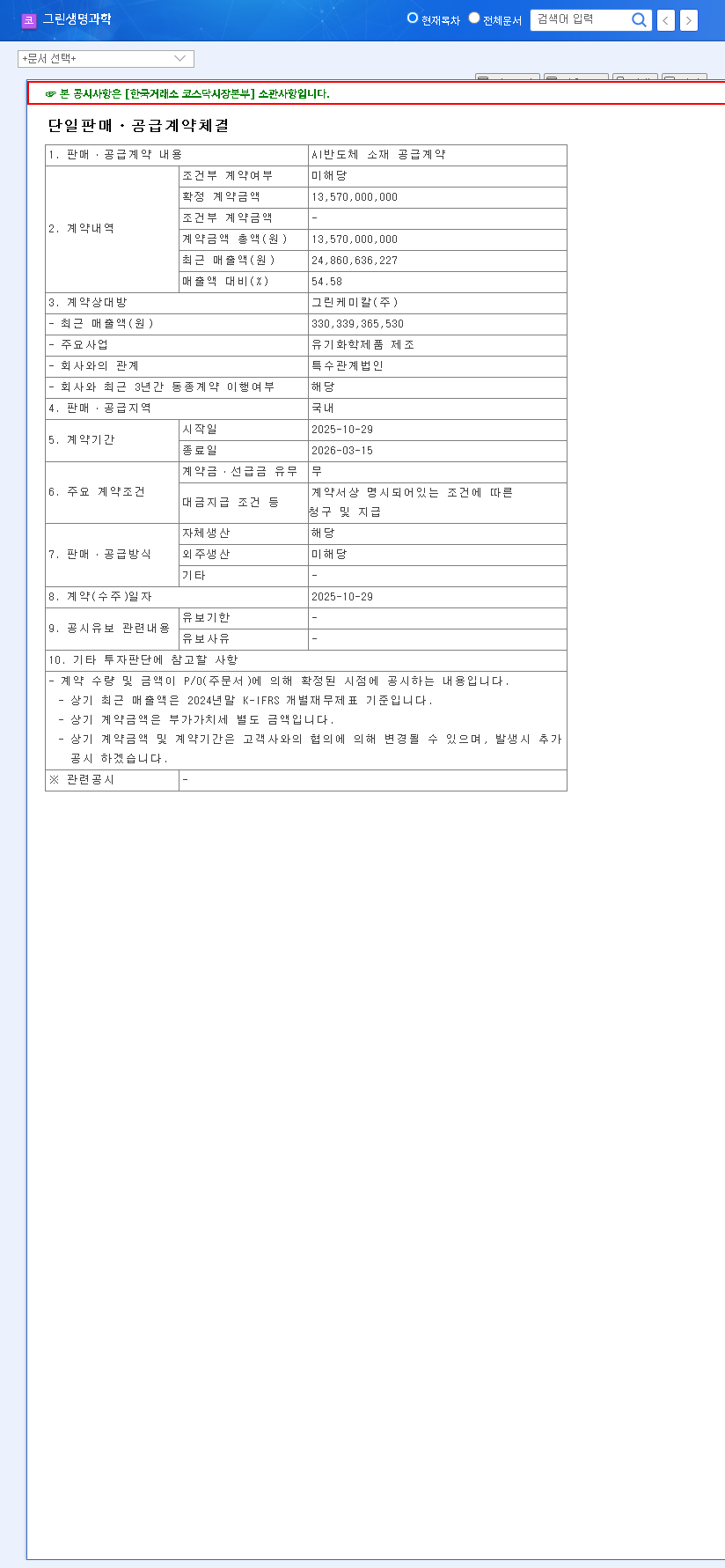

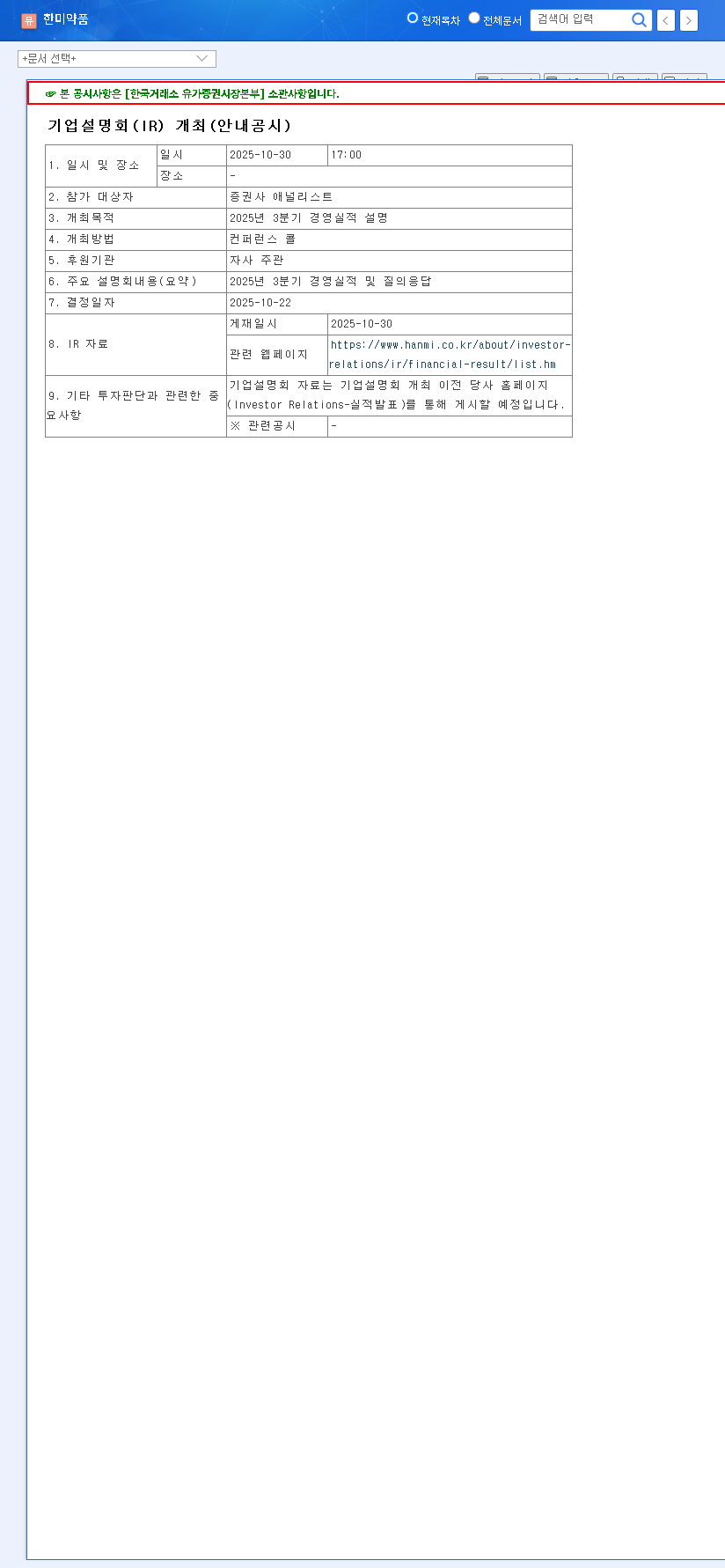

On October 30, 2025, GREEN LIFESCIENCE disclosed a supply contract for AI semiconductor materials worth a staggering ₩13.6 billion with Green Chemical Co., Ltd. The contract, which represents a remarkable 54.58% of the company’s recent annual revenue, is scheduled for domestic supply over a four-month period, from October 29, 2025, to March 15, 2026. This isn’t just a large order; it’s a statement of intent, validating the company’s diversification strategy and technological capabilities. For official verification, you can view the Official Disclosure (DART Report).

Fundamental Analysis: The State of GREEN LIFESCIENCE

Before this transformative deal, GREEN LIFESCIENCE presented a mixed but promising financial picture. A thorough stock analysis reveals both solid strengths and notable risks.

Core Strengths (Positive Factors)

- •Impressive Revenue Growth: The company’s half-year revenue for 2025 hit ₩16.351 billion, marking a 23.2% year-on-year increase.

- •Strategic Diversification: Proactive expansion into high-growth areas like electronic materials, secondary battery additives, and now AI semiconductor materials, showcases a forward-thinking growth strategy.

- •Technical Edge: Possession of unique technologies, including phosgene utilization, gives it a distinct competitive advantage within Korea.

- •CMO Competitiveness: With cGMP-compliant facilities, the company has strong potential for expanding its contract manufacturing organization (CMO) business.

Challenges and Risks (Negative Factors)

- •Profitability Concerns: Despite revenue growth, an operating loss of ₩-1.122 billion was recorded due to rising costs.

- •Inventory Management: A 53.8% increase in inventory assets raises questions about operational efficiency and potential write-downs.

- •Macroeconomic Headwinds: The business is susceptible to external factors like exchange rate volatility, high interest rates, and fluctuating raw material costs.

Impact of the AI Semiconductor Material Contract

This contract is a pivotal event. The AI semiconductor market is projected to grow exponentially, driven by advancements in machine learning and data centers. According to industry experts at McKinsey, this sector represents one of the most significant growth opportunities of the decade. For GREEN LIFESCIENCE, successfully entering this market could redefine its future.

This deal is more than just revenue; it’s a validation of GREEN LIFESCIENCE’s technological pivot. Success here could unlock access to a far larger, high-margin global supply chain.

Potential Upsides

- •Revenue and Profit Surge: The immediate ₩13.6 billion revenue boost is clear. If margins are favorable, it could significantly reverse the recent operating loss.

- •Market Re-evaluation: The contract enhances brand value and proves its capabilities, potentially leading to a higher stock valuation and attracting new high-profile clients.

- •Future Growth Engine: Establishes a strong foothold in a rapidly expanding industry, reducing reliance on the traditional pharmaceutical market.

Potential Downsides & Execution Risks

- •Margin Uncertainty: The profitability of this specific contract is unknown. High initial production costs for AI semiconductor material could squeeze margins.

- •Operational Risks: The semiconductor industry demands exceptionally high quality and supply chain stability. Any delays or quality issues could lead to severe penalties.

- •Short-Term Nature: The four-month contract duration provides a short-term boost, but long-term success hinges on securing follow-up orders and building lasting partnerships.

Comprehensive Outlook and Investor Strategy

The GREEN LIFESCIENCE AI semiconductor material deal is a powerfully positive catalyst. However, prudent investors should monitor several key performance indicators closely. Focus on the company’s ability to manage costs, maintain financial health amid rising interest rates, and demonstrate quality control. Future earnings reports will be critical for verifying the actual profit margins from this new venture.

For sustained, long-term growth, GREEN LIFESCIENCE must prove this is not a one-off contract but the beginning of a successful business division. Continued investment in R&D and securing additional orders will be the ultimate determinants of the company’s re-evaluation. For more insights, you can review our complete guide to investing in specialty chemical companies.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It does not constitute investment advice. All investment decisions should be made with the consultation of a qualified financial advisor.