This comprehensive DONG-A ST investment analysis dives deep into the recent corporate disclosures and financial health of DONG-A ST CO.,LTD. When the company’s largest shareholder, DONG-A Socio Holdings, filed a ‘Major Shareholding Status Report’, it prompted questions among investors. While the reported ownership change was minimal, the underlying details offer crucial signals about executive confidence, corporate governance, and the future trajectory of the DONG-A ST stock. We will thoroughly analyze this disclosure, review the company’s current fundamentals based on its 2025 half-year report, and provide a strategic outlook for investors seeking clear insights.

Unpacking the DONG-A ST Shareholding Disclosure

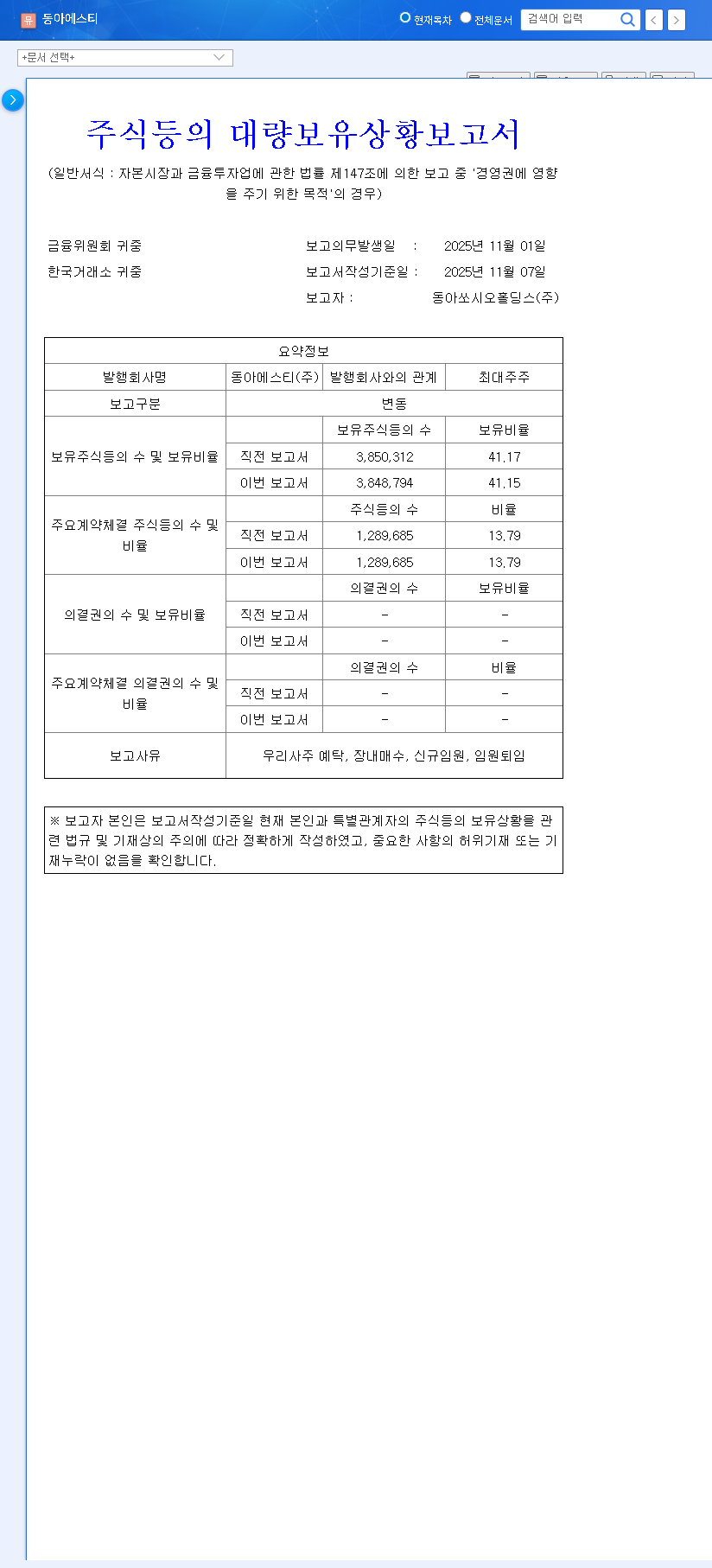

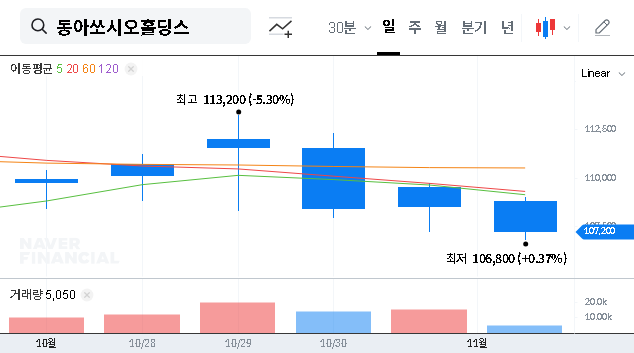

On November 7, 2025, DONG-A Socio Holdings filed a mandatory ‘Major Shareholding Status Report’. In financial markets, such filings are essential for transparency, even when the changes seem minor. The core of the report revealed a fractional decrease of 0.02%p in DONG-A Socio Holdings’ stake, shifting from 41.17% to 41.15%. The stated purpose of ownership remains ‘influence on management’, confirming their long-term strategic control.

Key Details of the Report

- •Reasons for Change: The shift was attributed to a combination of factors, including the deposit of employee stock ownership, strategic market purchases, and share reporting tied to the appointment and retirement of executives.

- •Key Personnel: Notably, executive Kim Hak-joon made a market purchase of 40 shares, while new executives Song In-sik, Jeong Seong-yeon, and others were newly reported.

- •Authoritative Source: The complete filing provides full transparency. You can view the Official Disclosure on the DART system.

The reporting of shares by newly appointed executives is a positive indicator, suggesting an alignment of interests and a commitment to responsible management and long-term value creation.

A Closer Look at DONG-A ST Fundamentals

To understand the context of the disclosure, a review of the current DONG-A ST fundamentals is essential. The 2025 half-year report paints a picture of a company in transition, balancing strong growth drivers with significant challenges.

For DONG-A ST, the path forward is a high-stakes balancing act: leveraging stable revenue streams to fund the high-risk, high-reward gamble of next-generation drug development.

The Bull Case: Growth and Innovation

- •Robust Sales: The company continues to see solid revenue growth, primarily driven by its growth hormone product ‘Grotropin’ and the strong performance of its overseas beverage division (Can Bacchus).

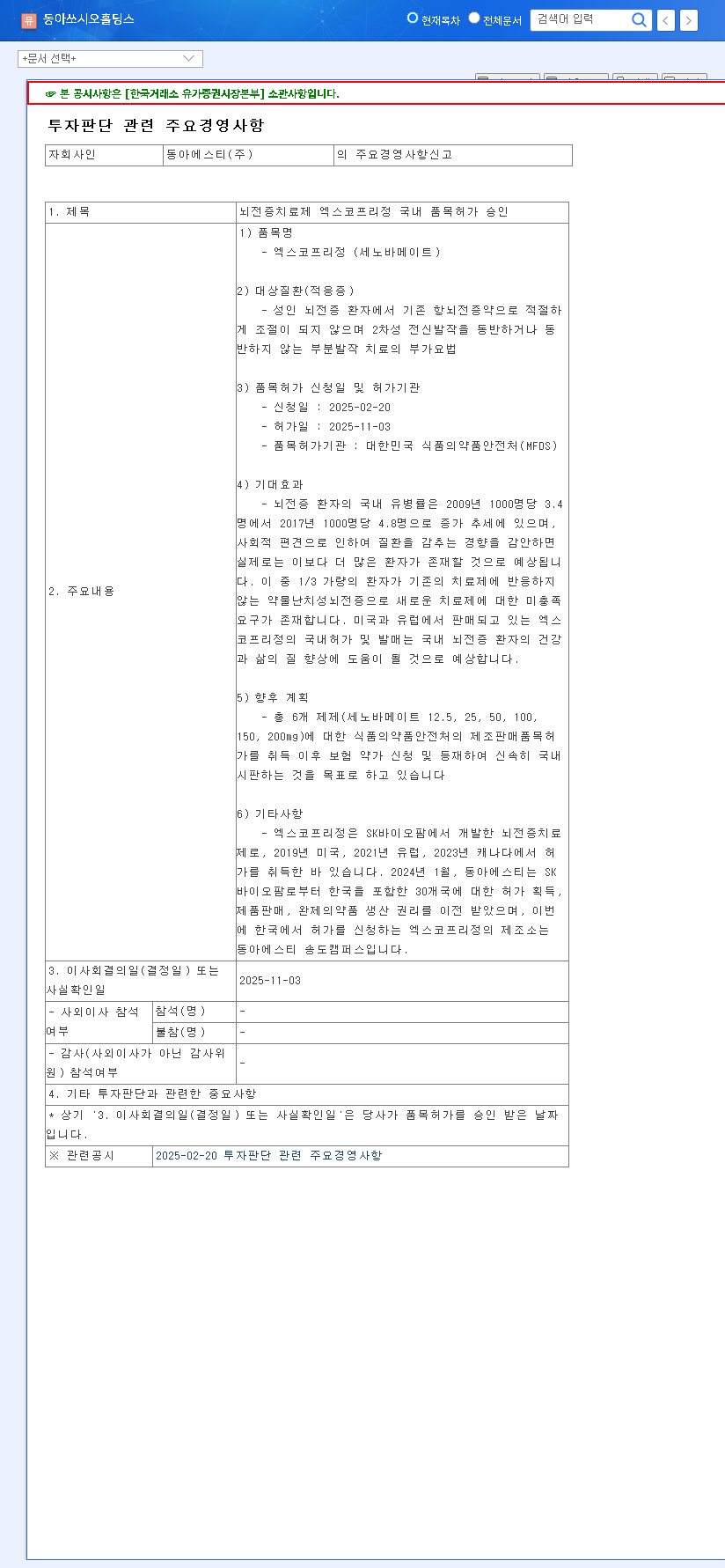

- •Aggressive R&D Investment: DONG-A ST CO.,LTD dedicates a significant portion of its budget (16.1% of sales) to R&D, signaling a strong commitment to securing future growth engines, including its promising entry into the Antibody-Drug Conjugate (ADC) field, a cutting-edge area of cancer therapy.

The Bear Case: Profitability and Risk

- •Profitability Concerns: Despite growing sales, the company remains in an operating loss position, with the net loss expanding year-over-year. This is a critical concern for investors focused on bottom-line performance.

- •R&D Uncertainty: High R&D spending comes with inherent risk. The discontinuation of some development projects (e.g., DA-8010) highlights that not all investments will yield returns, posing a risk to future profitability.

- •Macroeconomic Headwinds: As a global company, DONG-A ST is exposed to currency fluctuations (EUR/KRW, USD/KRW) and global economic uncertainty, which can impact overseas earnings and financial stability.

Investment Outlook & Strategic Considerations

The recent DONG-A ST shareholding disclosure is best viewed as a signal of stability rather than a cause for alarm. The largest shareholder’s control is unchallenged, and executive share participation reinforces a commitment to the company’s mission. However, this stability does not directly impact the short-term DONG-A ST stock price.

The company’s investment attractiveness hinges entirely on its ability to navigate the path from R&D spending to tangible, profitable products. Investors should consider a cautious but watchful approach. For further reading on this sector, you can review our guide on How to Analyze Pharmaceutical Stocks.

Key Monitoring Points for Investors:

- •R&D Pipeline Progress: Watch for announcements on clinical trial advancements and results for key pipeline candidates. Success here is the primary long-term value driver.

- •Path to Profitability: Scrutinize quarterly earnings reports for improvements in operating margins and any concrete strategies aimed at cost efficiency and achieving a positive net income.

- •Commercialization Success: As new drugs get approved, their market adoption and sales figures will be critical indicators of the company’s long-term health.

In conclusion, this DONG-A ST investment analysis suggests that while governance is stable, the company’s future is firmly tied to its scientific and commercial execution. The current fundamentals present a classic risk/reward scenario common in the biopharmaceutical industry.