A perfect storm appears to be gathering over Dong-A Socio Holdings Co., Ltd., a titan in the South Korean pharmaceutical landscape. Two significant developments have sent shockwaves through the market: a staggering decline in revenue revealed in their H1 2025 earnings report and a major institutional investor, Baring Asset Management, significantly reducing its stake. At the heart of this turmoil is the unprecedented sales plunge of its flagship energy drink, ‘Bacchus,’ raising serious questions about the company’s future. This comprehensive Dong-A Socio Holdings stock analysis will dissect these critical issues, explore the underlying causes, and provide a forward-looking perspective on what investors can expect.

The Dual Crises: Financial Shock and Investor Exodus

The current challenges facing the company can be distilled into two primary events that have collectively spooked the market and cast a long shadow over its valuation.

1. H1 2025: A Shocking Performance Collapse

The first half of 2025 delivered a financial report that can only be described as alarming. Dong-A Socio Holdings reported a consolidated revenue of KRW 675.3 billion, which represents a massive 50.6% decrease compared to the same period last year. This wasn’t just a slight miss; it was a fundamental collapse in top-line performance. The pain extended to the bottom line, with operating profit plummeting by 41.0% to KRW 48.5 billion. This sharp deterioration in profitability signals deep-seated issues across its core business segments, including both OTC/Quasi-drugs and its Biosimilar division.

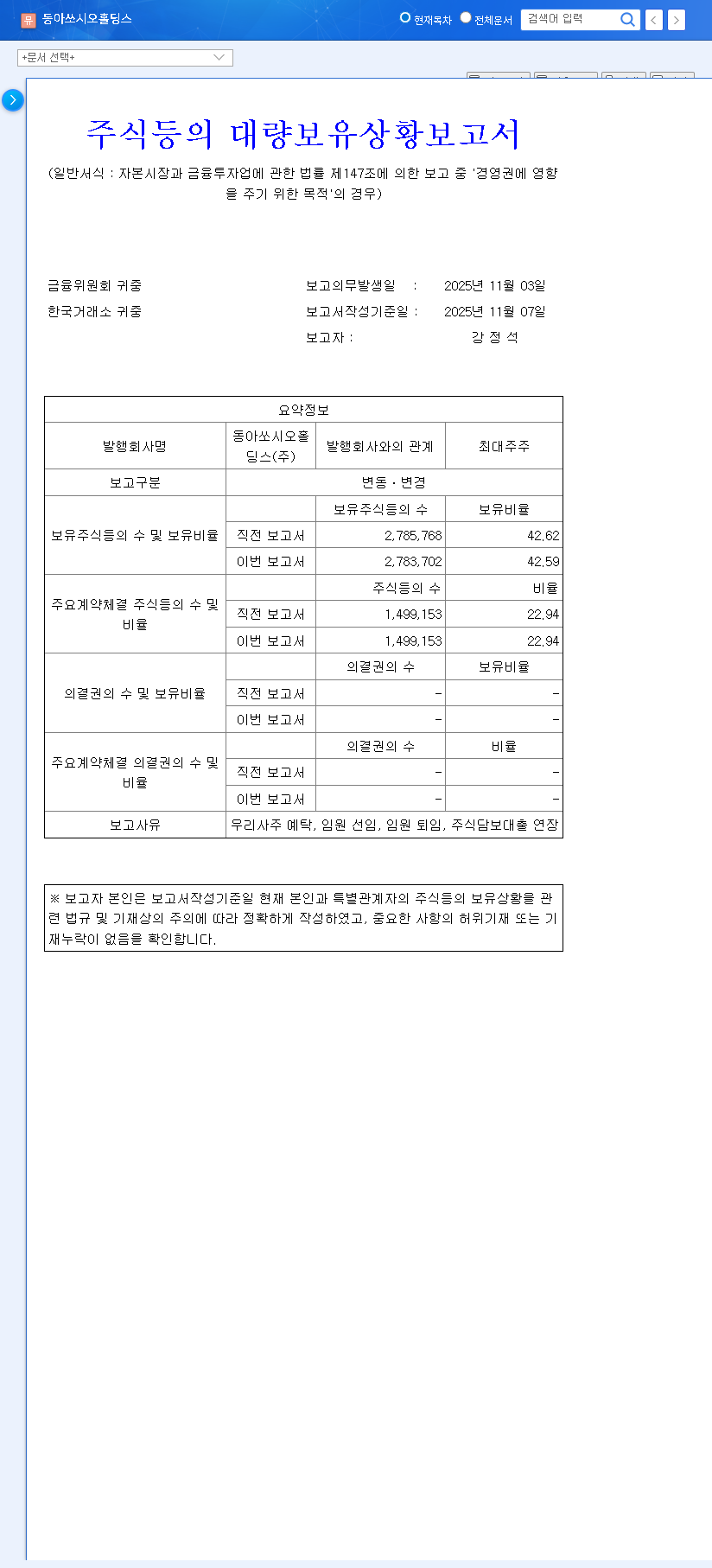

2. Baring Asset Management Reduces Its Stake

Adding to the fundamental concerns, a major institutional investor has voted with its feet. Baring Asset Management, a respected global investment firm, disclosed a reduction in its holdings from 8.45% to 7.40%. This 1.05 percentage point decrease, executed via open market sales, is a significant move. While the stated purpose was a “simple investment” adjustment, market analysts interpret such a substantial sell-off from a key stakeholder as a clear sign of waning confidence. You can review the Official Disclosure (DART) for more details. For a deeper understanding of market reactions, it’s often useful to see how this news is covered by authoritative sources like Bloomberg.

Analyzing the Root Causes of the Decline

Understanding why this is happening requires a closer look at the company’s core operations, particularly the dramatic failure of its most iconic product and weaknesses in other divisions.

The Unthinkable: Bacchus Sales Evaporate

The most critical factor behind the poor Dong-A Socio Holdings revenue is the catastrophic drop in ‘Bacchus’ sales. This product is not just a revenue stream; it’s a cultural icon and the company’s primary cash cow. Sales plummeted from KRW 125.3 billion to a mere KRW 54.07 million in the same period—a near-total collapse. The company must urgently determine if this is a result of temporary supply chain disruptions, a fundamental shift in consumer preference, or new, aggressive competition.

The failure to diagnose and reverse the Bacchus sales decline swiftly could have lasting and severe consequences for the company’s long-term corporate value and stock price.

Weakness Across the Portfolio

The problems don’t end with Bacchus. Other divisions are also underperforming, exacerbating the financial strain:

- •Biosimilars: While ‘Imuldosa’ saw increased sales, it was nowhere near enough to offset the massive revenue gap left by other products.

- •Other Segments: The Packaging and Mineral Water divisions continue to post operating losses, burdened by rising raw material costs.

- •Rising Costs: Selling and Administrative expenses rose by 7.0% year-on-year, further squeezing profitability in a time of falling revenue. Macroeconomic pressures like rising interest rates add to the financial burden.

Future Outlook and Impact on Dong-A Socio Holdings Stock Price

Given these severe headwinds, what does the future hold? The short-term outlook is undoubtedly bearish. The combination of dismal earnings and a public institutional sell-off is likely to create significant downward pressure on the Dong-A Socio Holdings stock price. Increased volatility is expected as the market digests this negative news. To learn more about market sentiment, you could read our guide on how to analyze institutional investor signals.

The mid-to-long-term recovery hinges on several key variables:

- •Bacchus Sales Revival: This is non-negotiable. The company’s ability to identify the cause of the sales drop and implement a successful recovery strategy is the single most important factor for its future.

- •New Growth Engines: The company must accelerate growth in its biosimilar pipeline and other ventures to diversify its revenue and reduce its over-reliance on a single product.

- •Restoring Investor Confidence: A return of institutional investment or a halt in the sell-off by firms like Baring Asset Management will be a critical signal that market confidence is being restored.

Strategic Considerations for Investors

For those conducting a Dong-A Socio Holdings stock analysis for investment purposes, a prudent and cautious approach is highly recommended. The company faces considerable uncertainty. Key indicators to monitor closely include:

- •Quarterly earnings reports for any sign of recovery in the OTC segment.

- •Company announcements regarding strategies to address the Bacchus sales issue.

- •Performance updates from the STGEN Bio division and other growth initiatives.

- •Future disclosures on institutional investor holdings.

Disclaimer: This analysis is based on publicly available information and is intended for informational purposes only. It should not be considered as financial advice. All investment decisions should be made based on your own research, judgment, and responsibility.