The latest JW PHARMACEUTICAL Q3 2025 Earnings report has sent a clear and powerful signal to the market. With a remarkable turnaround to net profitability and sustained revenue growth, investors are closely examining the company’s fundamentals and future trajectory. This comprehensive analysis will break down the provisional Q3 results, explore the core drivers of this success, and evaluate the opportunities and risks that lie ahead for JW Pharmaceutical’s stock.

JW PHARMACEUTICAL Q3 2025 Earnings: The Key Figures

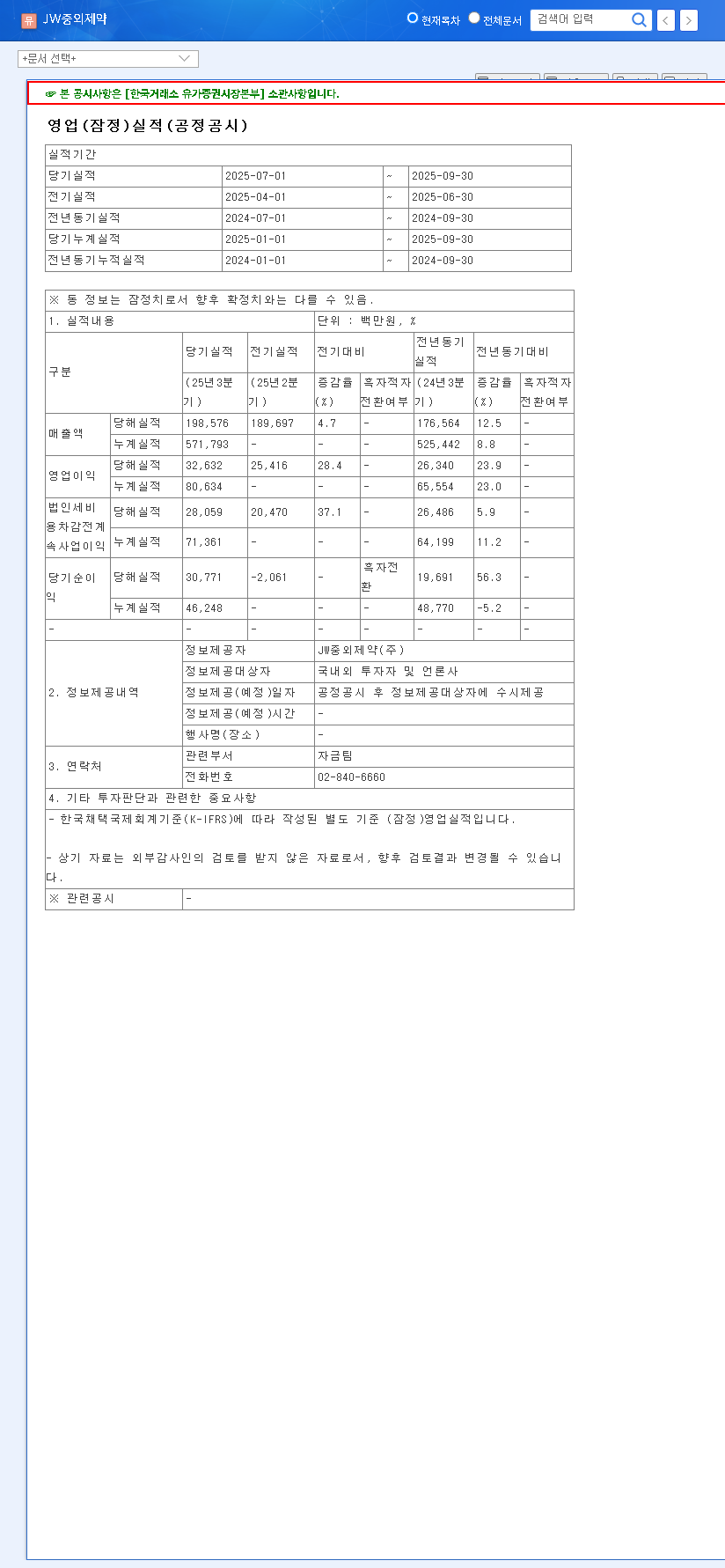

On November 3, 2025, JW Pharmaceutical released its provisional Q3 operating results, which painted a picture of robust health and strategic execution. These figures, sourced from the company’s Official Disclosure, exceeded many market expectations.

- •Revenue: ₩198.6 billion, a 3.92% increase compared to the previous quarter.

- •Operating Profit: ₩32.6 billion, marking an impressive 30.4% jump from Q2 2025.

- •Net Profit: ₩30.8 billion, a pivotal achievement representing a net profit turnaround from previous periods.

This surge in profitability, especially the shift to a positive net income, is the standout metric. It suggests that the company’s efficiency measures and high-margin product sales are not just sustaining the business but are actively driving significant bottom-line growth.

The Q3 net profit turnaround is more than just a number; it’s a testament to JW Pharmaceutical’s strengthening fundamentals and a potential catalyst for renewed investor confidence.

Deep Dive: The Pillars of JW Pharmaceutical’s Success

Understanding what’s behind these numbers is crucial for any potential investor. The company’s performance is not accidental; it’s built on a foundation of solid financial management and forward-looking R&D strategy.

Strengthening Financial Health

A stable financial base is essential for weathering market storms and funding future growth. JW Pharmaceutical has demonstrated remarkable fiscal discipline. The company’s debt-to-equity ratio has seen a significant improvement, falling to 82.54% from 115.10% at the end of last year. This reduction in leverage lowers financial risk and provides greater operational flexibility. Coupled with a healthy current ratio and consistently growing retained earnings, the balance sheet signals a company that is both profitable and prudently managed.

Aggressive and Strategic R&D Investment

The lifeblood of any pharmaceutical leader is its research and development pipeline. JW Pharmaceutical is investing heavily to secure its future, dedicating 13.1% of its revenue to R&D. This investment is not just about spending more; it’s about spending smarter. The development of ‘JWAVE’, an AI-based new drug development platform, is a prime example of this, promising to accelerate discovery and reduce costs.

The pipeline itself is promising, with several key candidates making progress:

- •URC102: A flagship candidate for a new gout treatment, URC102 is currently advancing smoothly through Phase 3 clinical trials. Success in this final stage before regulatory review could unlock a multi-billion dollar market. To learn more about this process, you can review the FDA’s drug development guidelines.

- •JW0061 & JW2286: These innovative drug candidates represent the company’s commitment to tackling unmet medical needs and diversifying its future revenue streams.

Investor Playbook: Outlook & Potential Risks

The positive JW PHARMACEUTICAL Q3 2025 Earnings report provides a strong basis for optimism, but a balanced investment thesis requires acknowledging potential headwinds.

Short-Term & Long-Term Outlook

In the short term, the market will focus on whether the company can sustain this level of profitability into Q4 and beyond. Continued strong performance and positive news flow from the R&D pipeline could provide further upward momentum for the stock.

From a long-term perspective, the ultimate value of JW Pharmaceutical will be determined by the successful commercialization of its innovative drug pipeline. The progress of URC102 and other key assets will be the primary driver of shareholder value over the next several years. For more details on our long-term views, you might want to read our annual pharmaceutical sector forecast.

Key Risks to Monitor

- •Market Competition: The pharmaceutical industry is intensely competitive. The success of JW’s products depends on their ability to stand out against established and emerging rivals.

- •Clinical Trial Outcomes: Drug development is inherently risky. Any setbacks in clinical trials, particularly for a late-stage asset like URC102, could significantly impact the stock price.

- •Economic Factors: As a global player, JW Pharmaceutical is exposed to exchange rate volatility, which can affect the cost of raw materials and the value of overseas sales.

Conclusion: A Cautiously Optimistic Verdict

The JW PHARMACEUTICAL Q3 2025 Earnings report is undoubtedly a positive development. The company has demonstrated its ability to generate strong profits while investing strategically for the future. While risks inherent in the pharmaceutical sector remain, the current trajectory suggests that JW Pharmaceutical is well-positioned to build on its recent successes. Investors should continue to monitor pipeline progress and financial performance closely.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and financial situation.