In a significant setback for Alzheimer’s research and investors in GemVax & KAEL Co.,Ltd. (KRX: 082270), the company has announced that its pivotal Phase 2 trial for GemVax GV1001 has failed to meet its primary endpoint. This news has sent shockwaves through the market, challenging the valuation of the company’s flagship biotech pipeline. For investors, this moment is critical. This comprehensive analysis will dissect the GemVax trial failure, explore its profound implications, and provide a clear, actionable strategy for navigating the path forward.

The failure of the GemVax GV1001 Alzheimer’s trial represents a major hurdle, forcing a fundamental re-evaluation of the company’s growth trajectory and investment thesis.

Deconstructing the GemVax GV1001 Trial Failure

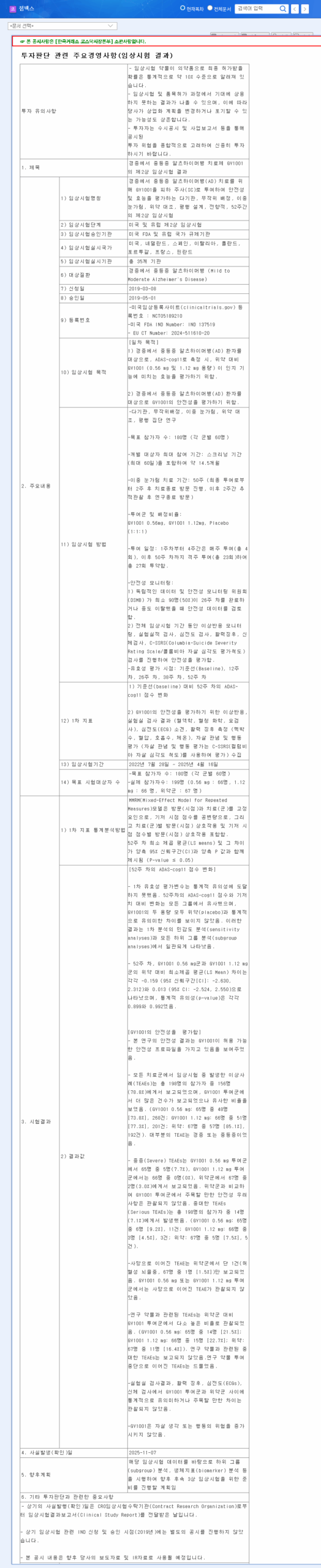

On November 7, 2025, GemVax released the top-line results from its multi-center, randomized, double-blind Phase 2 clinical trial for GV1001, an investigational treatment for mild to moderate Alzheimer’s disease. The study, conducted over 52 weeks, was meticulously designed to assess both the safety and efficacy of the drug candidate. The full details can be found in the Official Disclosure (DART).

The Critical Primary Endpoint Miss

The trial’s primary efficacy endpoint was the change in the Alzheimer’s Disease Assessment Scale-Cognitive Subscale (ADAS-cog11) score at week 52. This scale is a gold-standard metric used globally to measure cognitive decline in dementia patients. The results were unequivocal: GemVax GV1001 failed to achieve statistical significance, meaning it showed no demonstrable cognitive benefit over the placebo group. This is the most critical outcome of any clinical trial, as it directly addresses the drug’s core purpose.

While the drug did exhibit an acceptable safety profile with no new concerns, safety alone is insufficient for regulatory approval or commercial success. Efficacy is paramount, and in this regard, the trial was a clear failure.

Fundamental Analysis: Reassessing GemVax’s Strengths and Risks

Prior to this announcement, GemVax presented a complex investment profile. Understanding these factors is key to gauging the company’s resilience post-failure.

Pre-Trial Positives (Now Under Pressure)

- •Stable Environmental Business: A consistent revenue stream from its Chemical Air Filter division, serving the robust semiconductor industry, has acted as a financial anchor.

- •Pipeline Momentum: Prior to the failure, GV1001 had garnered FDA Fast Track and Orphan Drug designations, alongside a major domestic licensing deal, building significant market hype.

- •Improved Financials: Recent capital increases and narrowing operating losses showed a commitment to stabilizing the company’s financial footing.

Negative Factors and Amplified Risks

- •Realized Efficacy Failure: The primary risk has now materialized, effectively wiping out the near-term value of the GV1001 Alzheimer’s program.

- •Persistent R&D Burn: The biotech division remains a significant cash drain, and without a viable lead candidate, this spending now lacks a clear ROI.

- •High Debt Ratio: The company’s existing debt becomes more precarious without the promise of future blockbuster revenue to service it.

- •External Headwinds: Ongoing litigation risks and macroeconomic pressures on exchange rates and material costs further compound the company’s challenges.

The Cascade Effect: Impact on Business & Stock Price

The fallout from the GemVax trial failure will be swift and severe. The core value of its biotech pipeline has been decimated, raising questions about future Phase 3 trials and the validity of its licensing deal with Samsung Pharm. This uncertainty will make securing future funding significantly more difficult and expensive.

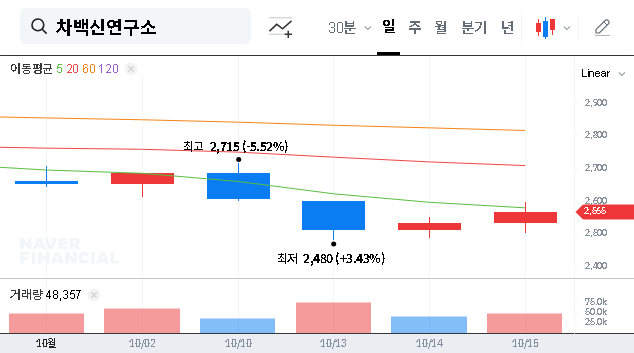

For investors, the most immediate impact will be on the stock price. The loss of the company’s primary growth engine will trigger a massive re-rating by the market. Given the high market capitalization built on the promise of GemVax GV1001, a substantial and sustained drop in share price is all but certain. For more context on biotech investing, see this guide from a leading financial news source.

Strategic Guidance for GemVax (KRX: 082270) Investors

This event is classified as ‘High Negative Impact.’ The stability of the environmental business is a positive but is unlikely to cushion the catastrophic blow to the biotech division. A proactive approach is required.

Recommendations for Action

- •Suspend New Investment: It is strongly advised to halt any new capital allocation to GemVax until the company provides a clear and credible strategic plan for its future.

- •Existing Investors – Monitor & Re-evaluate: For those with existing positions, monitor the market’s reaction and management’s communications closely. Watch for announcements regarding a pivot to other indications (like Progressive Supranuclear Palsy), a major business restructuring, or changes to the R&D leadership. Your decision to hold or sell should be based on this new strategic direction. You may want to read our guide to managing high-risk portfolio assets.

- •Prioritize Risk Management: This event underscores the inherent risks in biotech. Re-evaluate your overall portfolio’s exposure to such high-volatility assets and ensure your strategy aligns with your risk tolerance.

Future Outlook

The road ahead for GemVax is fraught with challenges. The company’s future now hinges on its ability to successfully pivot its R&D efforts, manage its cash burn, and maintain the profitability of its environmental business. Without a clear success in another clinical program, the company’s valuation will likely remain under severe pressure.