The recent divestment by Shinhan Asset Management from Symtek Holdings (036710) has sent shockwaves through the investment community. When a major institutional player completely exits a position, it naturally raises questions for every other shareholder. Is this a sign of impending trouble, or simply a strategic portfolio realignment? This comprehensive investment analysis will dissect the situation, explore the underlying fundamentals of Symtek Holdings stock, and provide a clear action plan for current and potential investors.

The Catalyst: Shinhan Asset Management’s Complete Exit

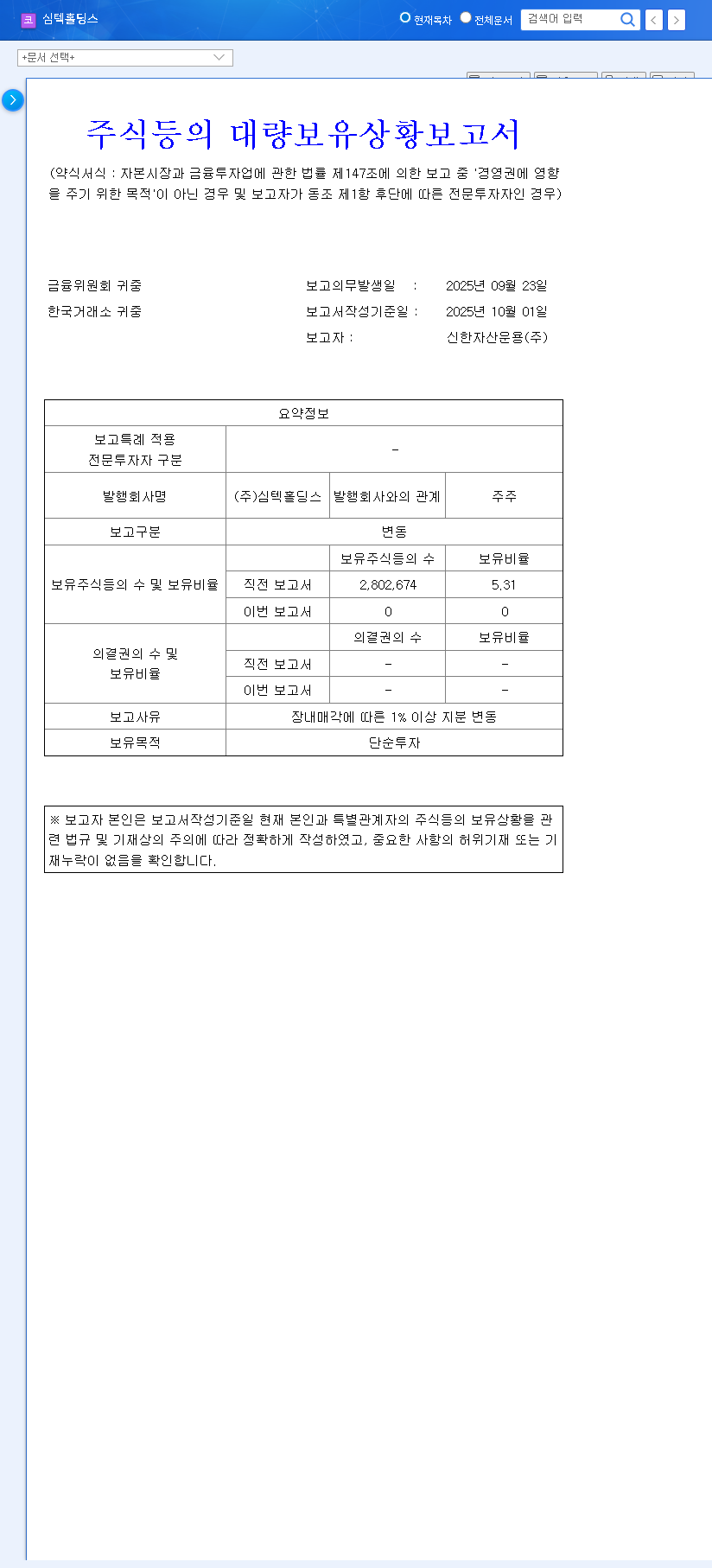

On October 2, 2025, a significant disclosure was made public: Shinhan Asset Management, a notable institutional investor, had sold its entire 5.31% stake in Symtek Holdings. This transaction reduced their ownership from a substantial position to zero, marking a definitive and complete withdrawal. This wasn’t a gradual reduction but a full divestment, a move that markets often interpret with caution. The official filing provides the concrete details of this major shift in ownership.

For full transparency, the transaction was documented in an official disclosure. Source: Click to view DART report. Understanding the ‘what’ is the first step; now we must delve into the ‘why’.

Why Now? Unpacking the Rationale Behind the Sale

An institutional exit is rarely based on a single factor. It’s typically a confluence of the company’s internal health, industry trends, and broader macroeconomic pressures. For Symtek Holdings, the picture is complex.

Corporate Fundamentals: A Precarious Financial State

At the heart of the concern lies the financial health of Symtek Holdings, a holding company whose fortunes are tied to its subsidiary, Symtek Co., Ltd., a PCB manufacturer. The H1 2025 report revealed several red flags that likely influenced Shinhan Asset Management‘s decision:

- •High Debt-to-Equity Ratio: The ratio has climbed to a concerning 464.12%. Such high leverage increases financial risk, making the company vulnerable to interest rate hikes and economic downturns.

- •Worsening Profitability: Declining sales have led to sustained consolidated operating and net losses. An expanding accumulated deficit signals ongoing struggles to achieve profitability.

- •Latent Risks: Liabilities from derivatives, convertible bonds, and bonds with warrants pose a threat of future stock dilution and financial strain.

Market Environment: A Mix of Headwinds and Tailwinds

While the company’s financials are a concern, the broader market provides a mixed outlook. The global PCB market is projected to grow, driven by demand in AI, 5G, and automotive sectors. However, the semiconductor and IT industries, which are key clients, are currently in a cyclical downturn, creating significant uncertainty, as reported by leading financial analysts (like those at Reuters). Furthermore, while potential interest rate cuts could offer some relief, Symtek’s heavy debt load means interest expenses will remain a major burden.

For investors, the core dilemma is whether Symtek Holdings’ long-term growth potential in the expanding PCB market can outweigh its immediate, and significant, financial vulnerabilities. Shinhan’s exit suggests that, for them, the risk was no longer worth the potential reward.

Projected Impact on Symtek Holdings Stock

Short-Term: Heightened Volatility & Negative Sentiment

The immediate market reaction to such a large stake sale is almost always negative. We can expect downward pressure on the Symtek Holdings stock price due to a simple supply-demand imbalance. The influx of shares into the market, coupled with weakened investor sentiment, is likely to increase volatility and test key technical support levels.

Mid-to-Long-Term: A Return to Fundamentals

While sentiment drives short-term prices, a company’s intrinsic value is determined by its long-term fundamentals. Shinhan’s sale does not alter Symtek’s business operations, its technological capabilities, or its client relationships. The long-term trajectory of the stock will depend on whether management can successfully navigate its financial challenges and capitalize on the growth opportunities we discussed in our deep dive into the PCB market outlook. The key will be the company’s ability to demonstrate a clear path to profitability and debt reduction in upcoming quarters.

Investor Action Plan: A Prudent Strategy Moving Forward

Panic selling is rarely a wise strategy. Instead, a measured approach based on careful monitoring is recommended for those holding Symtek Holdings stock.

- •Monitor Key Metrics: Watch stock price action and trading volume closely. Pay attention to upcoming earnings reports for any signs of improvement in profitability and debt management.

- •Track Industry Recovery: The timing of the semiconductor and IT market rebound is a critical catalyst. Positive news for the broader industry will be positive for Symtek.

- •Look for New Institutional Interest: The exit of one major investor creates a vacuum. Watch for filings that indicate a new major shareholder is taking a position, which could be a strong bullish signal.

Frequently Asked Questions (FAQ)

Q1: Does Shinhan’s sale mean Symtek Holdings is a bad investment?

A1: Not necessarily. It means that for Shinhan, the risk/reward profile no longer fit their strategy. It highlights existing financial risks but doesn’t erase the company’s market position or growth potential. Investors must weigh these factors for themselves.

Q2: What is the most critical factor for the Symtek Holdings stock recovery?

A2: The most critical factor is a tangible improvement in the company’s financial structure. This includes reducing its high debt-to-equity ratio and demonstrating a clear path back to sustainable profitability, likely tied to a recovery in the semiconductor industry.

Q3: Should I sell my Symtek Holdings stock now?

A3: This article provides analysis, not financial advice. The decision to sell depends on your personal risk tolerance, investment horizon, and belief in the company’s ability to overcome its current challenges. The short-term will likely be volatile.