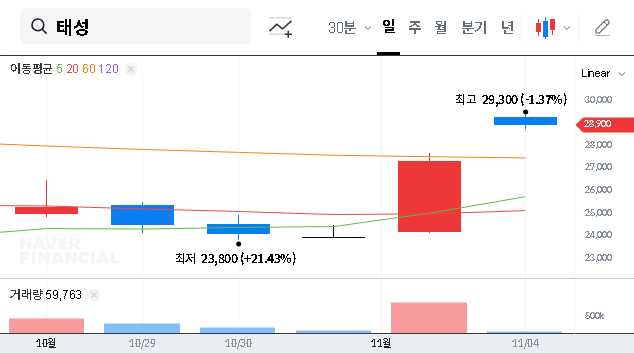

The upcoming TAESUNG Co., Ltd. Investor Relations (IR) event, scheduled for November 12, 2025, represents a critical moment for the company and its stakeholders. Following a period of sluggish performance in its core business, investors are keenly watching to see if TAESUNG can present a credible roadmap for recovery and unlock new avenues for TAESUNG future growth. This comprehensive analysis will delve into the company’s current financial standing, the potential of its new ventures, and the key factors that will influence investor sentiment following the IR presentation.

This deep-dive TAESUNG stock analysis aims to equip investors with the necessary insights to interpret the event’s outcomes and make informed decisions about the company’s long-term prospects.

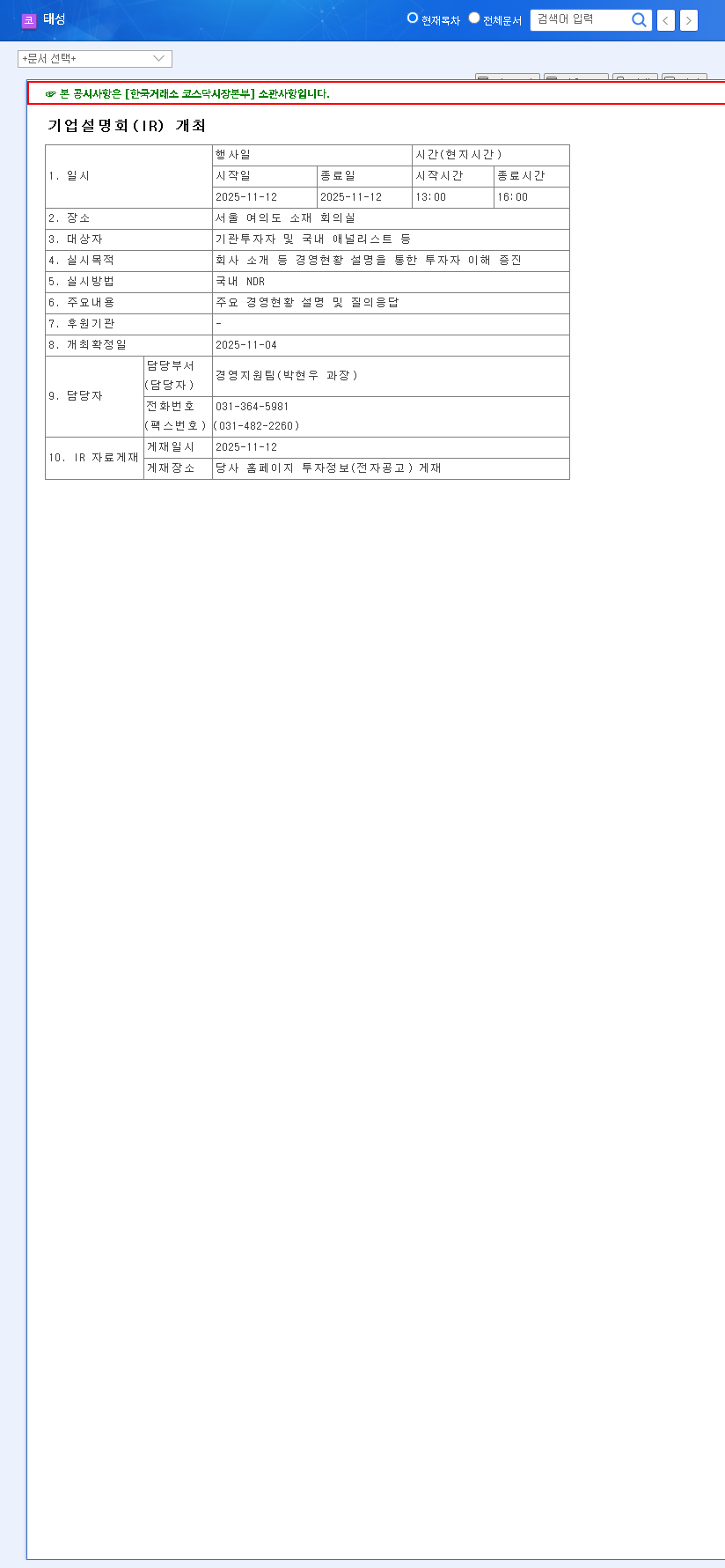

TAESUNG’s Pivotal IR Event: What to Expect

On November 12, 2025, at 1:00 PM, TAESUNG Co., Ltd. will host its corporate IR conference. The stated goal is to enhance investor understanding by providing a transparent overview of the company’s current management status and strategic direction. A key segment will be the Q&A session with senior management, offering a direct channel for investors to probe into the company’s strategy and address concerns regarding its present challenges and future ambitions. Investors should pay close attention to the specifics of their turnaround strategy for the core business and the projected timelines for their new growth initiatives.

The clarity and confidence with which management addresses its recent performance slump and outlines its vision for new markets will be the ultimate litmus test for restoring investor trust.

A Company at a Crossroads: Financial and Market Analysis

Mixed Signals: Poor Performance vs. Sound Financials

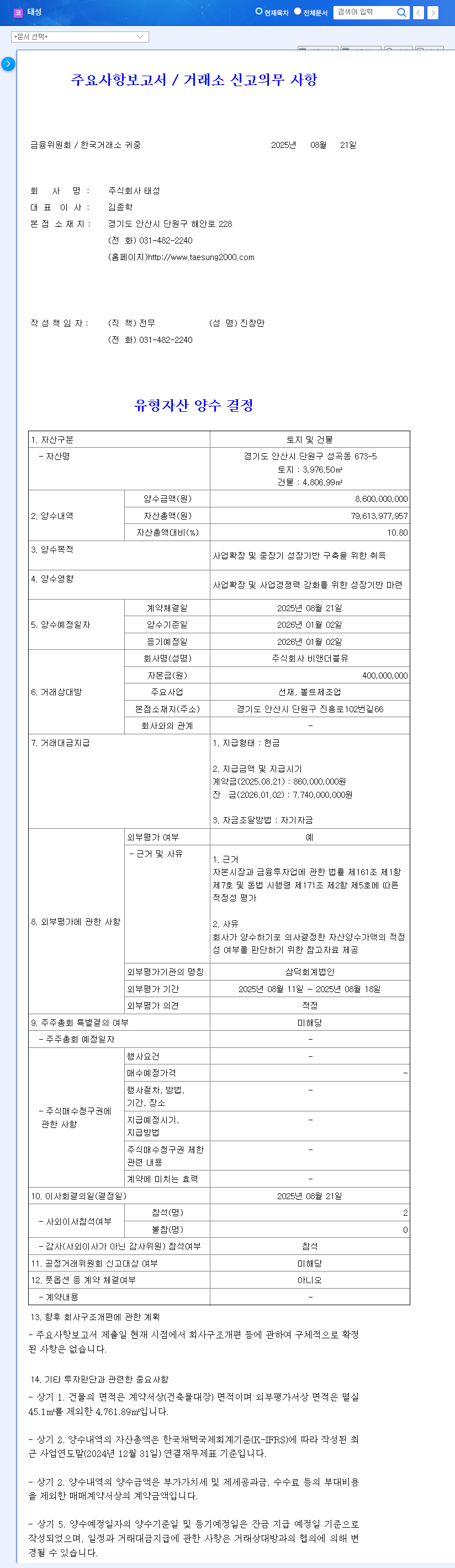

TAESUNG’s 2025 half-year results were undeniably disappointing, with revenue dropping nearly 50% year-on-year, leading to an operating loss. This was largely driven by a sharp decline in its primary PCB automation equipment business. However, the balance sheet tells a different story. A successful paid-in capital increase significantly bolstered total equity, and the company’s cash reserves now exceed its total borrowings. This financial stability provides a crucial cushion and the necessary capital to fund its strategic pivot into new sectors without taking on excessive debt.

Investing in the Future: TAESUNG’s New Business Ventures

To secure long-term growth, TAESUNG is aggressively investing in several high-potential areas. The success of this TAESUNG new business strategy is paramount. These ventures include:

- •Camera Modules & Secondary Batteries: Entering the competitive electronics component space, TAESUNG aims to leverage its manufacturing expertise. The global secondary battery market, in particular, is experiencing explosive growth, driven by the EV and energy storage sectors, as noted in industry reports from leading financial analysts.

- •Next-Generation Glass Substrate Equipment: This is a forward-looking investment in advanced packaging technology for the semiconductor industry. As chips become more complex, glass substrates offer superior performance, and establishing an early foothold could yield significant returns.

While promising, these ventures face headwinds, including intense competition from established players and the challenge of securing major clients as a new market entrant. The TAESUNG Co., Ltd. Investor Relations event must provide a convincing strategy to overcome these hurdles.

Navigating Macroeconomic Headwinds

The company’s turnaround efforts are set against a challenging global economic backdrop. Key external factors include rising interest rates that increase financing costs, volatile exchange rates impacting material import costs, and elevated energy prices affecting production and logistics. These macroeconomic pressures could dampen investor sentiment regardless of the company’s operational progress.

Investor Action Plan & Future Outlook

Recommendations for Investors

Investors should approach the IR with a critical mindset. Focus on the substance of the presentations, not just the rhetoric. Key questions to consider are: What are the specific revenue and profitability targets for the new business units? What is the tangible plan to regain market share in the PCB automation sector? For further guidance, you can review our guide to analyzing corporate growth strategies. Despite past performance, a long-term perspective is advisable, weighing the potential of these new ventures against the execution risks.

Key Monitoring Points Post-IR

Following the event, the focus will shift from promises to execution. Investors should monitor the following:

- •New Business Performance: Track announcements of new client contracts, order backlogs, and initial revenue contribution from the battery and glass substrate divisions.

- •Core Business Recovery: Look for signs of stabilization or recovery in the core PCB automation equipment market.

- •Official Filings: For a complete and official overview, investors are encouraged to review the company’s filings. Source: Click to view DART report.

Frequently Asked Questions (FAQ)

Q1: What are the main reasons for TAESUNG’s recent underperformance?

A1: The recent underperformance in 2025 stems primarily from a significant decrease in sales from its core PCB automation equipment business, compounded by an increase in selling, general, and administrative expenses.

Q2: What new businesses is TAESUNG Co., Ltd. pursuing for future growth?

A2: TAESUNG is diversifying into new high-growth sectors by establishing divisions for camera modules and secondary batteries. It is also making strategic investments in the development of next-generation glass substrate equipment.

Q3: How stable is TAESUNG’s financial health despite poor results?

A3: Despite the operational loss, TAESUNG’s financial position is sound. A recent capital increase significantly boosted its total equity, and its cash and cash equivalents currently exceed its total borrowings, indicating a healthy and stable balance sheet.