The latest Hecto Financial earnings analysis for Q3 2025 reveals a complex picture for investors. While the FinTech company announced provisional results showing operating and net profits that surpassed market expectations, a deeper dive into the numbers uncovers persistent challenges that could impact its long-term growth trajectory. Does this positive quarter signal a genuine turnaround, or is it a temporary reprieve from more fundamental issues?

This comprehensive report breaks down the Hecto Financial Q3 performance, evaluating the company’s fundamentals, financial health, and competitive landscape. We will explore whether the recent profitability is sustainable and what investors should monitor moving forward to make informed decisions about their Hecto Financial stock holdings.

Hecto Financial’s Q3 2025 Earnings: A Detailed Breakdown

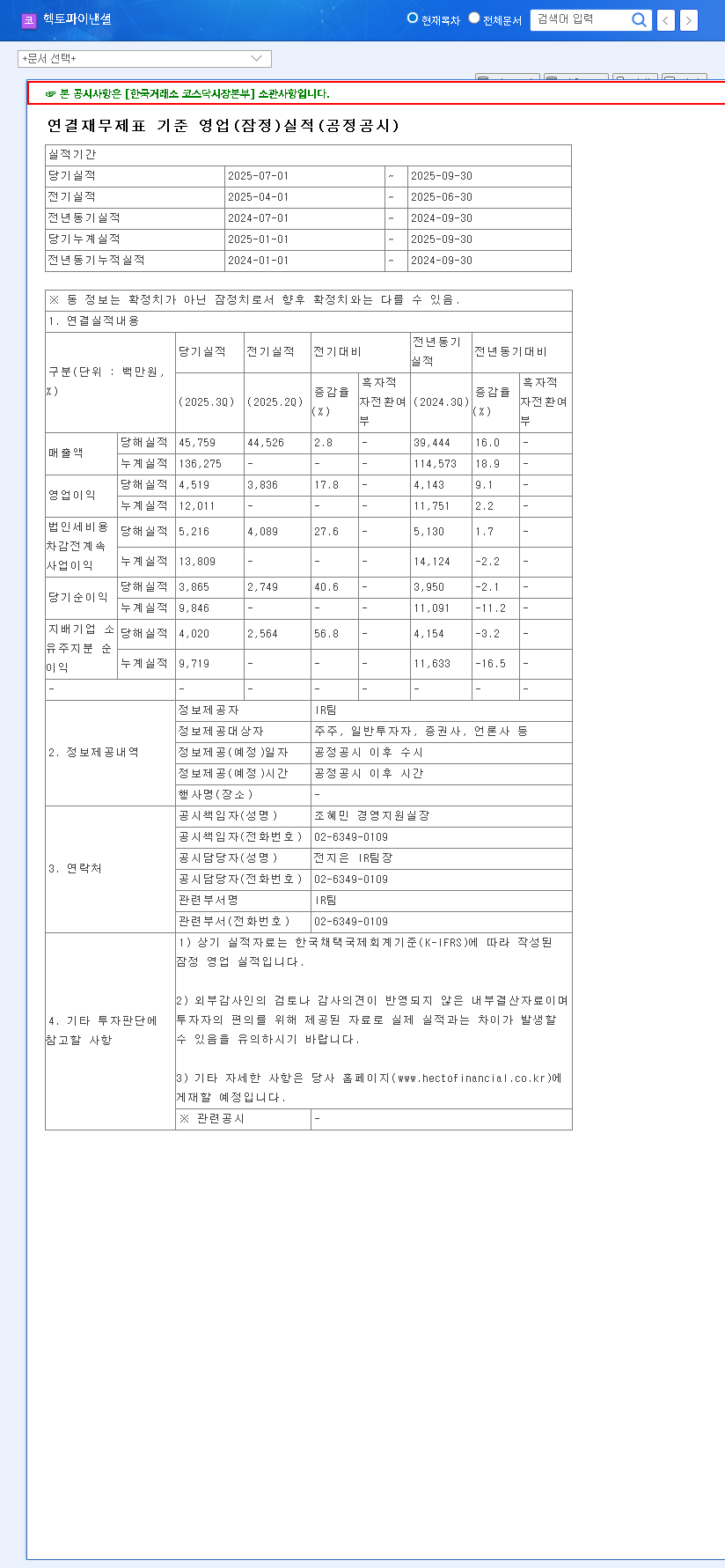

For the third quarter of 2025, Hecto Financial reported a welcome beat on its profitability metrics, offering a short-term boost to market sentiment. However, the top-line revenue figure continues to be a point of concern. The full details can be found in the official filing (Source: Official DART Disclosure).

- •Revenue: Reported at KRW 45.8 billion, a 1.0% miss against the KRW 46.2 billion estimate. While this represents a slight sequential increase, it fails to reverse the troubling downward trend observed since 2022.

- •Operating Profit: A bright spot at KRW 4.5 billion, which is a significant 7.1% beat over the KRW 4.2 billion estimate. This marks an improvement both quarter-over-quarter and year-over-year, suggesting a potential bottoming-out process after the Q4 2024 low.

- •Net Profit: Reached KRW 4.0 billion, a 3.0% beat on estimates of KRW 3.9 billion. The strength in operating profit flowed directly to the bottom line, showing a substantial sequential improvement.

While the market may celebrate the profit beat, the persistent revenue decline is a critical red flag that questions the sustainability of this recovery. True long-term growth for Hecto Financial must come from the top line.

Core Business Strengths and Future Growth Engines

At its core, Hecto Financial is a player in the competitive world of FinTech payment services. Understanding its foundation and future bets is key to a complete Hecto Financial earnings analysis.

Established Competitive Advantages

The company’s primary revenue streams—virtual accounts, firm banking, and Payment Gateway (PG) services—are supported by a strong competitive moat built on several pillars:

- •First-Mover Advantage: Early entry into the simple cash payment market has established strong brand recognition and a loyal user base.

- •Technological Superiority: Decades of experience in bank system operations have cultivated deep technical expertise.

- •Robust Security: A key differentiator in FinTech, with 24/7 real-time monitoring and dual-operated systems to ensure stability and trust.

Venturing into New Territories

To combat slowing growth, Hecto Financial is expanding its horizons into high-potential areas, though these come with their own uncertainties. These include data-driven businesses like MyData and an ambitious entry into the Security Token Offering (STO) market. While STOs offer a pathway to innovate in capital markets, their success is heavily dependent on a clear and favorable regulatory environment, which remains a significant variable. For more on this, read our deep dive into the evolving STO market.

Financial Health Check: A Tale of Two Ledgers

Despite the Q3 profit rebound, a look at Hecto Financial’s balance sheet reveals areas that warrant caution.

- •Solid Liquidity: As of mid-2025, the company boasts a healthy cash position of KRW 247.4 billion, indicating no immediate short-term liquidity risks.

- •Rising Debt Ratio: The concerning metric is the debt ratio, which surged from 92.27% in 2022 to 113.53% in 2023. This rise, coupled with declining revenue, could strain financial stability, especially if interest rates increase.

- •Macroeconomic Headwinds: While direct exposure to interest rate hikes is currently minimal due to fixed-rate borrowings, indirect effects are a risk. According to top economic analysts, shifts in oil prices and global interest rate volatility can dampen consumer sentiment, indirectly affecting transaction volumes.

Investment Outlook: Balancing Short-Term Wins with Long-Term Risks

In conclusion, this Hecto Financial earnings analysis paints a dual narrative. The short-term picture is encouraging, with the profit beat likely to provide temporary positive momentum for the stock.

The Bull Case (Positive Factors)

- •Profitability Turnaround: Exceeding profit estimates is a strong signal that cost-control measures may be taking effect.

- •Strong Core Tech: The company’s underlying technology and security infrastructure remain valuable assets in the growing FinTech space.

The Bear Case (Negative Risks)

- •Persistent Revenue Decline: The most urgent issue is the need for a sustainable revenue growth driver.

- •Deteriorating Financial Structure: The rising debt ratio is a significant concern that could limit future flexibility and increase risk.

- •New Business Uncertainty: The success of ventures like STO is not guaranteed and hinges on external regulatory factors.

Investors should look beyond the headline profit numbers and focus on whether Hecto Financial can address its structural challenges in the upcoming quarters. Close attention should be paid to the Q4 results and any strategic plans aimed at reigniting top-line growth and improving the company’s financial leverage.

Disclaimer: This report is based on provided information and independent analysis, and does not constitute a direct recommendation for any investment decision. Investment decisions should be made based on the investor’s own judgment and responsibility.