The latest Dongwon Systems Q3 2025 earnings report presents a complex but crucial narrative for investors. Dongwon Systems Corporation (KRX: 014820) announced its provisional results for the third quarter, revealing a challenging period marked by declining revenue and profits. While these top-line figures may seem disappointing, a deeper analysis reveals a resilient growth story centered on its burgeoning secondary battery materials business. This comprehensive review will dissect the financial performance, explore the underlying market dynamics, and provide a strategic outlook for anyone following Dongwon Systems stock.

Despite facing macroeconomic headwinds like global economic slowdowns and raw material price volatility, the consensus is that the company’s long-term growth trajectory, powered by its investments in battery technology, remains intact. How should investors interpret these mixed signals? Let’s dive into the details.

Dongwon Systems Q3 2025 Earnings: The Official Figures

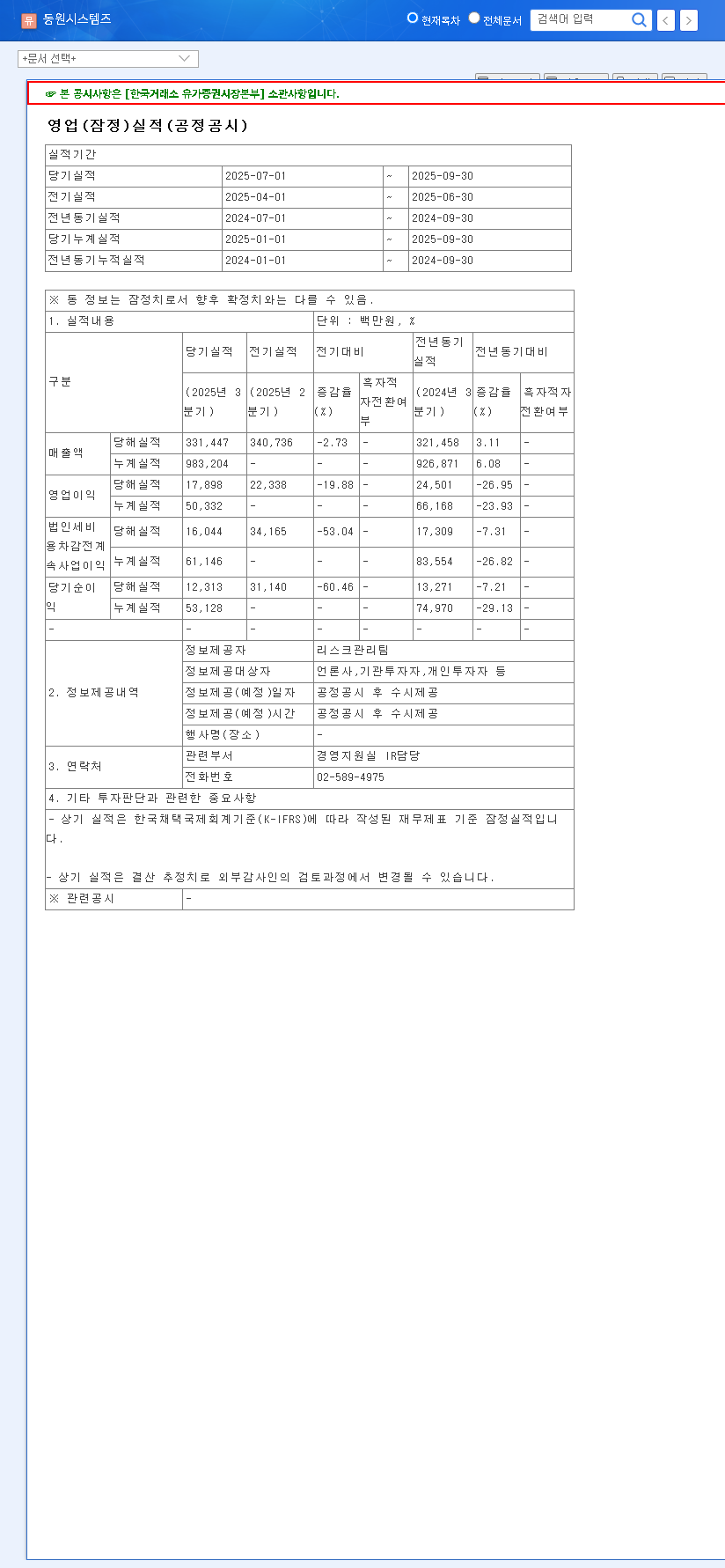

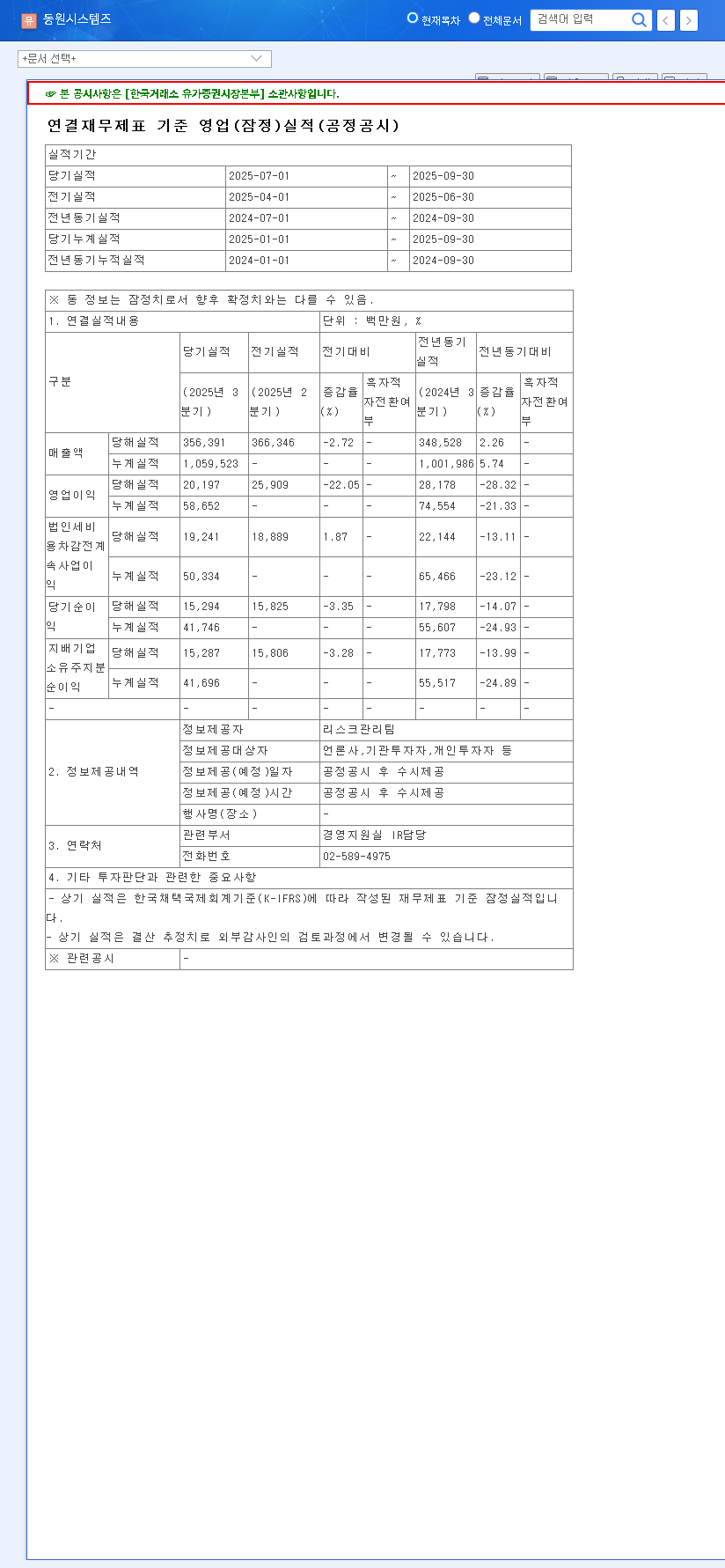

Dongwon Systems officially reported its Q3 2025 provisional operating results, which fell short of market expectations. The key figures, as filed in the Official Disclosure (DART), are as follows:

- •Revenue: KRW 331.4 billion (a decrease from KRW 366.3 billion in Q2 2025 and KRW 348.5 billion in Q3 2024).

- •Operating Profit: KRW 17.9 billion (a significant drop from KRW 25.9 billion in Q2 2025 and KRW 28.2 billion in Q3 2024).

- •Net Profit: KRW 12.3 billion (down from KRW 15.8 billion in Q2 2025 and KRW 17.8 billion in Q3 2024).

Key Factors Behind the Underperformance

The dip in performance can be attributed to several converging external pressures. The continued global economic slowdown, as reported by authoritative sources like major financial news outlets, has suppressed demand in traditional packaging sectors. Furthermore, profitability was squeezed by volatile raw material prices and unfavorable exchange rate fluctuations, which impacted margins in core business segments. This created a challenging environment that even the growth in the secondary battery division could not fully offset in the short term.

Despite the short-term headwinds affecting legacy segments, the market’s focus remains fixed on the long-term potential of Dongwon’s secondary battery materials division. Its strategic investments are positioning it as a key supplier in the booming global EV supply chain.

The Growth Engine: Secondary Battery Business Shines Bright

The most crucial part of any Dongwon Systems analysis is understanding the immense potential of its secondary battery materials business. While the overall Q3 earnings were down, this segment remains a powerful engine for future growth. The global market for lithium battery cans is projected to grow at a compound annual growth rate (CAGR) of 19.7%, driven by the explosive demand for electric vehicles (EVs) and energy storage solutions.

Strategic Positioning for Future Dominance

Dongwon Systems is not merely participating in this market; it is actively positioning itself as a leader. Key strategic initiatives include:

- •Technological Advancement: The development and impending mass production of the 4680 CAN Assy (a key component for next-generation cylindrical batteries) demonstrate its technical prowess.

- •Capacity Expansion: The acquisition of MKC and investments in its R&D center are building a robust production system capable of meeting future demand from major battery manufacturers.

- •Market Diversification: The company continues to leverage its technology to expand its global customer base, reducing reliance on any single market. You can learn more about this in our deep dive on the secondary battery market.

Investor Outlook: Balancing Risks and Opportunities

The disappointing 014820 earnings for Q3 may exert short-term downward pressure on the stock price. However, savvy investors will look beyond the immediate numbers to the long-term fundamentals. The key is to monitor whether the growth and improving margins in the secondary battery business can materialize into concrete earnings and offset the challenges in other divisions.

Key Checklist for Investors

- •Monitor Battery Segment Performance: Look for specific data on order volumes, revenue contribution, and profitability from the secondary battery division in upcoming reports.

- •Assess Financial Health: Keep an eye on the company’s debt levels and its strategies for managing increased borrowing costs amid rising interest rates.

- •Track Macroeconomic Indicators: Pay attention to exchange rate trends (Won vs. USD/EUR) and key raw material prices, as these directly impact profitability.