CITECH’s High-Stakes Bet: Analyzing the 15 Billion Won Hyeopjin Investment

The recent CITECH investment into Hyeopjin, a food processing machinery manufacturer, has sent ripples through the market. CITECH CO.,LTD (004920) has committed a substantial 15 billion Korean Won to acquire a 39.62% stake, a move that raises critical questions about its strategic direction. While the company is pivoting towards high-tech growth sectors like AI healthcare and advanced Public Address (PA) systems, this significant capital allocation into an unrelated industry demands a thorough CITECH financial analysis. Is this a savvy diversification play to unlock future value, or a risky gamble that could strain its already burdened finances? This deep dive will explore the fundamentals, risks, and potential rewards of the Hyeopjin acquisition.

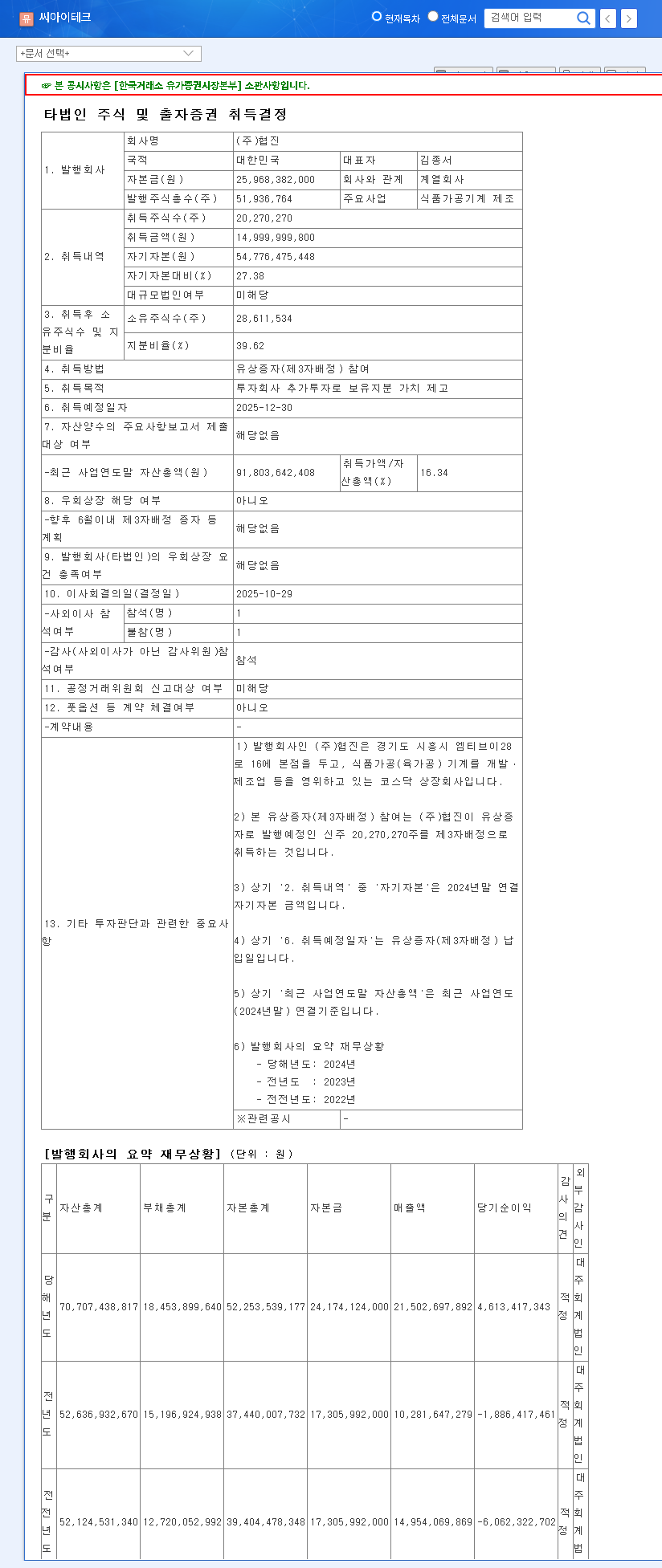

The Details of the Deal: What We Know

According to an official disclosure filed on October 30, 2025, CITECH will acquire its stake by participating in Hyeopjin’s third-party allocation paid-in capital increase, with the transaction scheduled for completion by December 30, 2025. This investment represents a significant 27.38% of CITECH’s own capital, making it a major financial event for the company. The officially stated purpose is to “enhance the value of its equity stake through additional investment in the investee company.” You can view the full details in the official filing. Official Disclosure (Source: DART).

This large-scale CITECH investment is a classic double-edged sword. It offers the potential for portfolio diversification and equity growth but simultaneously introduces considerable financial risk and a potential distraction from its core technology ventures.

CITECH’s Strategic Pivot vs. Financial Reality

To truly grasp the implications of the Hyeopjin acquisition, we must place it in the context of CITECH’s current business strategy and financial health. The company is at a crucial inflection point, investing heavily in what it deems its future.

Future Growth Engines: AI Healthcare & PA Systems

CITECH has clearly signaled its future lies in technology. Its primary new ventures are an AI healthcare platform and advanced PA systems, leveraging its proprietary ‘Hi-Fi Rose’ audio brand. Furthermore, a planned merger with its subsidiary, MOD Co., Ltd., aims to internalize smart hospital solutions, creating a vertically integrated health-tech service. This focus is evidenced by a consolidated R&D expense ratio of 10%. However, these ventures are still in their nascent stages and have yet to generate substantial revenue, making them a long-term play requiring sustained investment. For more on this, see our deep dive into CITECH’s AI strategy.

A Look at the Financials: The Burden of Debt

A critical part of any 004920 analysis is its balance sheet. CITECH is navigating a challenging financial landscape. With a reported debt-to-equity ratio of 66.9% and total debt obligations listed at a staggering 37.88 trillion Won, the company’s leverage is a significant concern. The recent issuance of 3 billion Won in convertible bonds further highlights its need for capital. This existing financial pressure makes the 15 billion Won cash outlay for the CITECH investment particularly noteworthy, as it could strain short-term liquidity and heighten financial risk.

Investor Action Plan: Key Factors to Monitor

Given the high degree of uncertainty, investors should adopt a ‘Neutral’ stance and closely monitor several key performance indicators. A prudent approach is essential to navigate the risks associated with the CITECH stock. As noted by analysts at authoritative financial publications like Bloomberg, assessing synergy is key in cross-industry acquisitions.

- •Hyeopjin’s Performance: Scrutinize Hyeopjin’s quarterly revenue, profit margins, and market position. Is the food machinery industry growing, and can Hyeopjin capture that growth?

- •Synergy Materialization: Look for concrete plans or announcements from CITECH’s management detailing how they plan to create synergy between their tech ventures and Hyeopjin. The absence of a clear plan is a major red flag.

- •CITECH’s Financial Health: Analyze CITECH’s upcoming financial reports for changes in cash flow, debt levels, and profitability. Are they managing their existing debt effectively while absorbing this new investment?

- •Core Business Momentum: Track the progress of the AI healthcare and PA system businesses. Are they hitting milestones, signing clients, and moving towards profitability? This CITECH investment is more justifiable if the core business is strong.

Conclusion: A Calculated Risk with an Uncertain Payoff

Ultimately, CITECH’s acquisition of a stake in Hyeopjin is a bold, contrarian move. If Hyeopjin performs exceptionally well, it could provide a stable, profitable anchor that funds CITECH’s more speculative tech ventures. However, if it underperforms, it will be a costly diversion of capital and management focus at a time when the company can least afford it. Only time will reveal whether this was a strategic masterstroke or a critical misstep. For now, diligent monitoring and a cautious outlook are the best tools for any investor considering CITECH stock.