An in-depth analysis of the Hyundai E&C stock reveals a company at a critical crossroads in 2025. Facing a challenging domestic construction market while simultaneously unlocking new growth overseas, investors are keenly observing every move. The release of the company’s 76th Half-Year Report adds a layer of complexity, compounded by the significant news of the National Pension Service (NPS) divesting a portion of its shares. For the official data, you can view the Official Disclosure (DART). This comprehensive analysis will dissect these factors to provide a clear Hyundai E&C stock price forecast and a strategic investment outlook.

Dissecting the H1 2025 Report: Performance & Key Issues

The first half of 2025 painted a mixed picture for Hyundai E&C. The company navigated a turbulent environment marked by a severe downturn in the domestic building and housing sector. High interest rates and persistent concerns over project financing (PF) defaults led to a stark 56.3% year-on-year decrease in domestic sales revenue. This highlights the company’s vulnerability to local market conditions.

However, the story isn’t entirely bleak. The overseas segment emerged as a powerful counter-balance. The Plant and New Energy sector showcased impressive resilience and growth, with sales revenue climbing by 21.2%. This surge is attributed to a strategic pivot towards high-demand global projects, cementing its role as a vital future growth engine for the company. The civil engineering division is also poised for a mid-to-long-term recovery, buoyed by government infrastructure spending and market diversification efforts. For a deeper dive into market trends, investors can review comprehensive construction sector reports for broader context.

Key Financial Highlights

- •Sales Revenue: Significantly decreased due to the domestic housing slump.

- •Operating Profit: Increased by a healthy 7.9%, showcasing the success of a profit-focused ordering strategy and effective cost controls.

- •Net Income: Declined by 8.1%, primarily impacted by unfavorable foreign exchange rates and rising miscellaneous expenses.

- •Financial Health: While total equity grew, a notable 56.1% increase in short-term borrowings raises a red flag regarding interest payment burdens in a high-rate environment.

The NPS Sell-Off: Reading the Institutional Tea Leaves

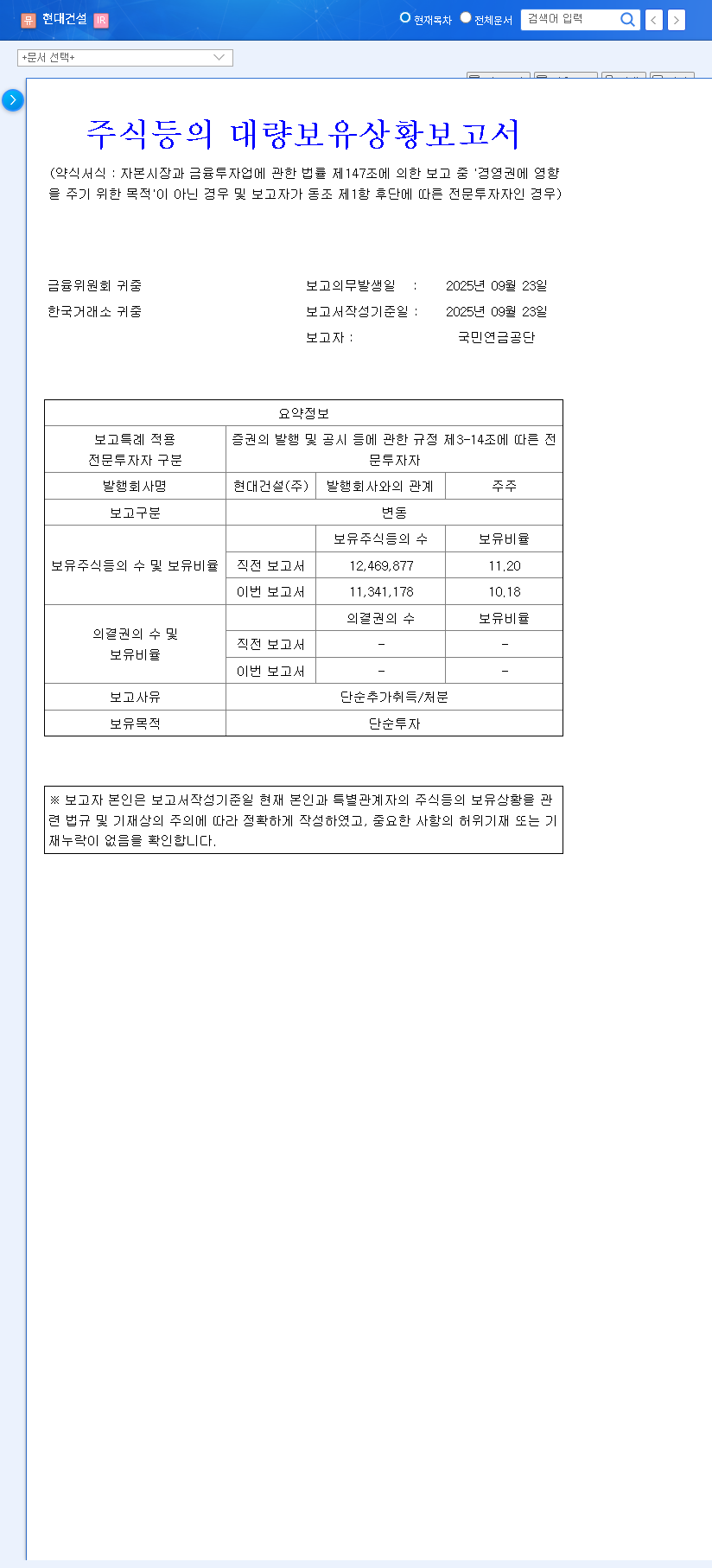

Perhaps the most significant market event was the news that the National Pension Service (NPS) sold 1.02% of Hyundai E&C shares, reducing its stake to 10.18%. While officially for ‘simple investment purposes’, a move of this magnitude by a major institutional investor inevitably sends ripples through the market. This can trigger short-term supply-demand instability and negatively impact investor sentiment, as other market participants may interpret it as a bearish signal. Any potential Hyundai E&C investment strategy must account for this increased volatility.

The current investment thesis for Hyundai E&C stock is ‘Neutral.’ The company’s long-term growth potential in new energy and overseas markets is promising, but it is overshadowed by immediate risks from the domestic market, PF liabilities, and institutional selling pressure.

Future Outlook: Risks and Growth Catalysts

Looking ahead, the Hyundai E&C outlook is a delicate balance of risks and opportunities. The company’s ability to navigate these dual realities will determine its trajectory.

Key Risk Factors

Several headwinds could impede performance:

- •PF Project Liabilities: Contingent liabilities from real estate project financing remain a significant financial risk.

- •Legal Issues: Ongoing litigation and arbitration related to subsidiary Hyundai Engineering could result in unforeseen costs.

- •Rising Debt: The sharp increase in short-term debt could strain financial stability if interest rates remain elevated. Authoritative resources like Bloomberg’s market analysis provide further insight into macroeconomic pressures.

Primary Growth Drivers

On the upside, Hyundai E&C is cultivating powerful growth catalysts:

- •Overseas Expansion: Continued success in securing high-margin overseas orders in renewable energy, next-gen nuclear power (SMRs), and data centers is crucial.

- •Profit-Centric Strategy: A disciplined approach to project selection and cost management can continue to bolster operating margins despite top-line pressures.

- •Infrastructure Investment: Global government initiatives to modernize infrastructure provide a steady pipeline for the civil engineering sector.

Action Plan for Hyundai E&C Stock Investors

For those considering an investment in Hyundai E&C stock, a watchful and patient approach is recommended. Closely monitor the following factors before making a decision:

- •Confirm sustained growth in overseas orders, particularly in the New Energy sector.

- •Watch for concrete plans to manage PF liabilities and reduce short-term debt.

- •Assess strategies to improve profitability within the domestic housing business.

- •Track the outcomes of ongoing legal disputes and their potential financial impact.

- •Continue to monitor trading activity from major institutional investors like the NPS.

In conclusion, while Hyundai E&C is making strategic investments for its future, investors should weigh the company’s execution capabilities against market headwinds before committing capital. A cautious, ‘Neutral’ stance is warranted until there is greater clarity on risk mitigation and a sustained recovery in key financial metrics.