In a significant move that signals robust health amidst economic headwinds, DL E&C CO.,LTD. (375500) has announced a major contract win for a large-scale housing redevelopment project. For savvy investors, this news raises critical questions: How does this ₩386.8 billion deal fortify DL E&C’s market position, and what does it mean for its stock value moving into 2025? This comprehensive analysis will dissect the investment merits, potential risks, and financial outlook for DL E&C CO.,LTD., providing the crucial insights needed for informed decision-making.

This latest project win is not just another number in the order book; it’s a testament to DL E&C’s enduring brand power and its strategic positioning in the competitive metropolitan redevelopment market.

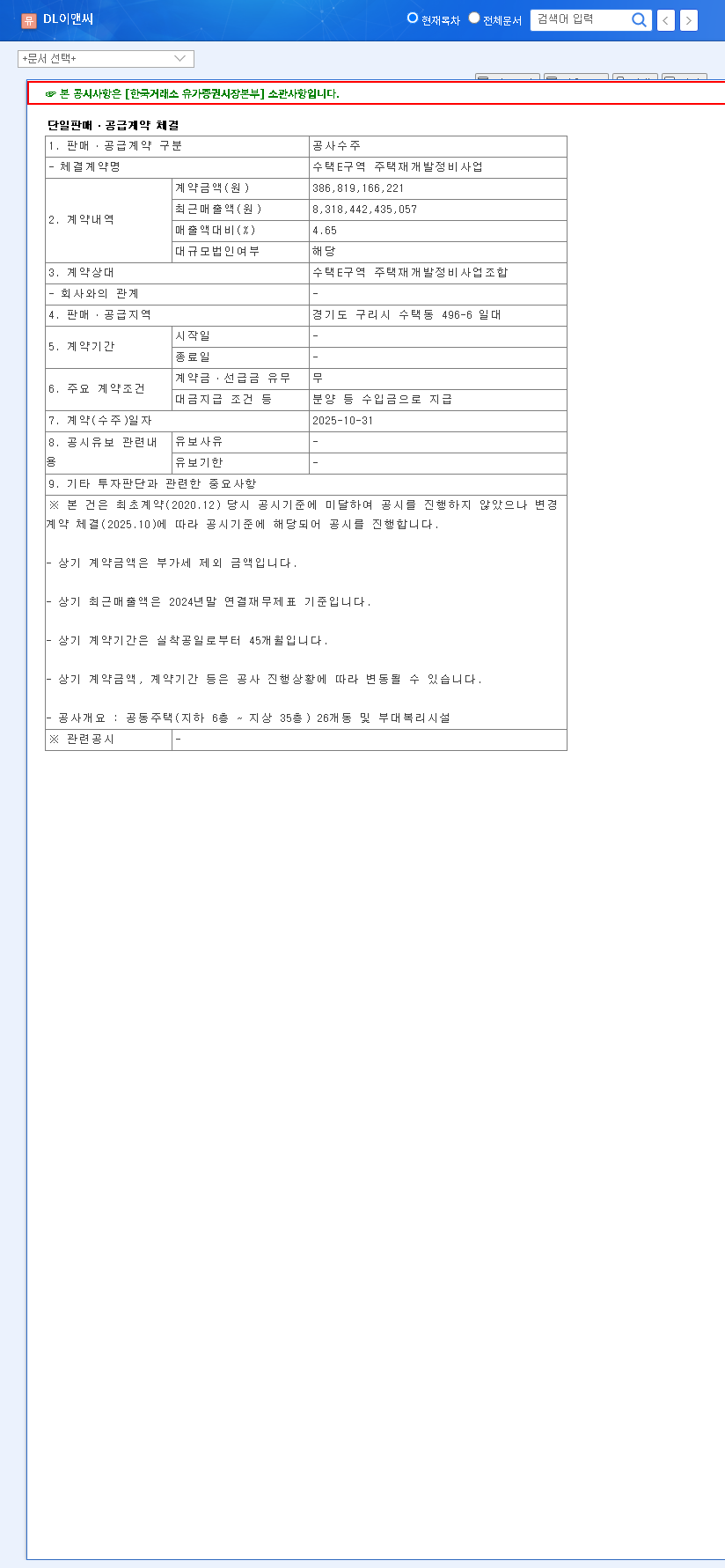

The Landmark Deal: Su-taek E District Project

On October 31, 2025, DL E&C CO.,LTD. formally announced the signing of a construction contract valued at an impressive 386.8 billion won with the Su-taek E District Housing Redevelopment Project Association. This strategically important project is located in Guri-si, Gyeonggi-do, a key satellite city in the Seoul metropolitan area. Representing 4.65% of the company’s recent annual revenue, this single contract provides a substantial boost to its order backlog and reinforces its dominance in the urban regeneration sector. For official confirmation, you can view the Official Disclosure (DART).

Why This Contract Matters for Investors

Solidifying an Already Robust Order Backlog

A stable order backlog is the lifeblood of any construction firm, providing visibility into future revenues and insulating against market downturns. As of late 2025, DL E&C CO.,LTD. maintained a formidable backlog of approximately 21.87 trillion won. The Su-taek E District project further cements this foundation, ensuring a steady stream of work and revenue, which is a highly positive signal for long-term investors.

Enhancing the High-Value Housing Portfolio

This project allows DL E&C to leverage the immense brand equity of its premium apartment brands, ‘e-Pyeonhansesang’ and ‘ACRO’. Securing redevelopment projects in prime metropolitan locations not only generates revenue but also acts as a powerful marketing tool, enhancing brand prestige and attracting future high-value contracts. This win strengthens the company’s position as a leader in the premium housing market, a critical component for a deeper look into the Korean construction market.

Analyzing the Financial Health and Potential Risks of DL E&C CO.,LTD.

While the new contract is a significant positive, a comprehensive investment analysis requires a balanced view of both the company’s financial strength and the external risks it faces.

Key Risk Factors to Monitor

- •Macroeconomic Volatility: Persistently high interest rates globally can increase borrowing costs for large-scale projects. Furthermore, as an international player, DL E&C is exposed to currency fluctuations (KRW/USD, KRW/EUR) which can impact the bottom line of its overseas plant projects.

- •Commodity and Supply Chain Pressures: Volatility in oil prices, shipping costs, and raw materials like steel and cement can directly squeeze profit margins on fixed-price contracts. Efficient supply chain management is crucial to mitigating this risk.

- •Domestic Housing Market Sentiment: The health of the domestic real estate market and the management of Project Financing (PF) risks are paramount. A slowdown in the housing market could impact sales velocity and project profitability.

A Positive Financial Trajectory

Despite the risks, DL E&C’s financial indicators show a company on a path of recovery and strengthening stability. Financial data, often cited by outlets like leading financial news sources, points to a positive trend.

- •Improving Stability: The company’s debt-to-equity ratio has seen a consistent decline, reaching a healthy 49.38% in late 2024. This indicates reduced financial leverage and a stronger balance sheet.

- •Profitability on the Rise: Forecasts for 2025 are optimistic, projecting significant improvements in operating profit margin (to 11.93%) and net profit margin (to 11.90%). This suggests operational efficiency and strong pricing power.

- •Growth and Shareholder Value: Revenue is projected to grow to 2.7987 trillion won in 2025, with Earnings Per Share (EPS) expected to see a substantial leap to 3,776 won, signaling strong potential returns for shareholders.

Conclusion: An Investor’s Action Plan

The successful bid for the Su-taek E District project is a clear positive catalyst for DL E&C CO.,LTD. It reaffirms the company’s competitive edge and provides a solid foundation for achieving its promising 2025 performance forecasts. The company exhibits a healthy blend of growth momentum and improving financial stability.

Investors should weigh this positive outlook against the backdrop of macroeconomic uncertainties. The key will be DL E&C’s ability to navigate these external pressures through prudent cost management and strategic project execution. For those considering an investment in DL E&C stock, the current trajectory appears favorable, but continuous monitoring of key market and company-specific indicators is essential.