CJ SEAFOOD CORPORATION Q3 Earnings: A Mixed Signal for Investors

The latest CJ SEAFOOD CORPORATION earnings report for Q3 2025 presents a complex picture for current and potential investors. While the company posted a notable quarter-over-quarter revenue increase, the persistent operating loss and stagnant net profit have cast a shadow over its performance, leaving many to question the future of CJ Seafood stock. This article provides a comprehensive fundamental analysis of the results, explores the underlying challenges, and outlines a potential investor action plan based on the available data.

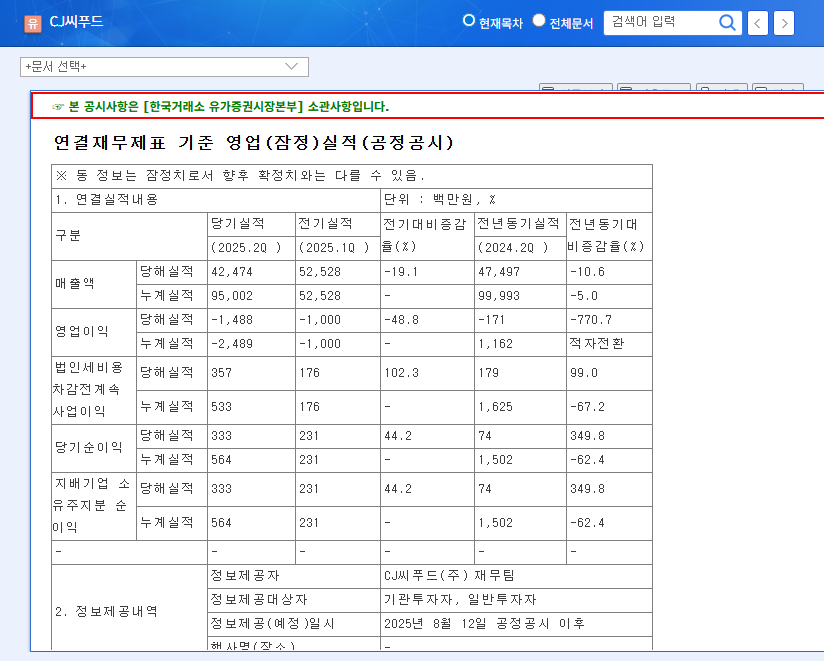

According to the Official Disclosure filed on November 11, 2025, the preliminary consolidated financials reveal a company at a critical crossroads. Let’s break down the key figures.

Q3 2025 Financial Highlights

- •Revenue: KRW 49.4 billion, a promising 16.2% increase from the previous quarter, but still down 7.8% year-over-year.

- •Operating Profit: A loss of KRW 0.6 billion. While this is an improvement from the previous quarter’s loss, it marks a worrying shift to a deficit compared to the same period last year.

- •Net Profit: KRW 0 billion. This break-even result represents a significant decline both quarter-over-quarter and year-over-year, indicating a complete stall in bottom-line profitability.

Fundamental Analysis: Unpacking the Underperformance

To understand the trajectory of CJ Seafood stock, we must look beyond the headline numbers. Several internal and external factors are contributing to this challenging period, forming the basis of our fundamental analysis.

Core Business and Financial Weaknesses

The company’s core operations, particularly in the seaweed and fishery product divisions, have seen a significant slump. This isn’t just about revenue; it’s about profitability. Despite the quarterly revenue bump, a higher cost of goods sold and rising selling & administrative expenses have effectively erased any gains, preventing a return to operating profit. Furthermore, the company’s financial health is a major concern. A high debt-to-equity ratio, coupled with diminishing operating cash flow, creates a precarious situation, making the company vulnerable to market shocks.

While investments in affiliated companies signal an effort to find future growth, these initiatives have yet to deliver tangible results, adding to investor uncertainty surrounding the latest CJ SEAFOOD CORPORATION earnings.

Navigating Macroeconomic Headwinds

CJ SEAFOOD CORPORATION is also battling a difficult macroeconomic environment. Persistently high interest rates, driven by the US benchmark, directly increase the cost of servicing its significant debt. As reported by major financial news outlets, global economic conditions remain challenging. The high KRW/USD exchange rate exacerbates this by inflating the cost of imported raw materials, putting constant pressure on profit margins. On a brighter note, key logistics cost indicators like the Baltic Dry Index (BDI) have stabilized, offering some relief on the expense side, but this has not been enough to offset the other financial pressures.

Investor Action Plan & Stock Outlook

Given the disappointing Q3 results, the market’s reaction is likely to be negative. The continued operating loss is a major red flag that could lead to downward pressure on the stock in the short term as investor sentiment wanes. Many of these fundamental weaknesses may already be priced in, but this report could accelerate a decline if confidence erodes further.

Investment Thesis: A Cautious ‘Hold’

At this juncture, a proactive investment is difficult to recommend. The lack of positive momentum and clear profitability pathways suggests a cautious approach is warranted. For a more detailed look at industry trends, see our analysis of the broader consumer staples sector.

- •For Current Shareholders: Consider holding your position but monitor the Q4 report and 2026 business plan closely. Look for concrete strategies on margin improvement, debt reduction, and a tangible return from affiliated company investments.

- •For Potential Investors: It is prudent to remain on the sidelines. The risk currently outweighs the potential reward. A potential entry point would only emerge after the company demonstrates a sustained turnaround with at least one to two quarters of positive operating profit and a clear, credible growth strategy.

In conclusion, while the quarterly revenue uptick provides a sliver of hope, the overall financial picture from the CJ SEAFOOD CORPORATION earnings report is concerning. Until the company can prove it has a viable plan to restore profitability and manage its financial burdens, exercising caution is the most sensible investor action plan.