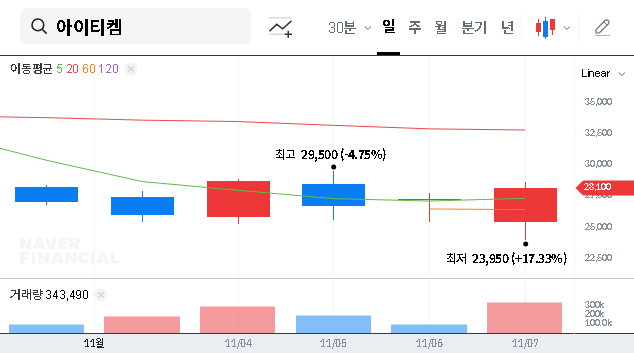

A significant development has captured the attention of investors monitoring IT-CHEM Co., Ltd. (IT-CHEM, 309710). On November 13, 2025, a major shareholder, Oculus Private Equity Fund No. 1, disclosed the sale of a substantial block of shares. This move has understandably created uncertainty and raised a critical question: What does this signal for the future of IT-CHEM stock?

This comprehensive IT-CHEM analysis moves beyond the headlines to provide a deep dive into the company’s fundamental value, its powerful growth engines, and the potential risks on the horizon. Our goal is to equip you with the clarity needed to make informed investment decisions amidst short-term market volatility.

The Catalyst: Unpacking the Oculus Private Equity Share Sale

The event that triggered market ripples was detailed in a public filing. According to the Official Disclosure (DART), Oculus Private Equity Fund No. 1 executed an off-market sale of IT-CHEM Co., Ltd. shares. Here are the key facts:

- •Stake Reduction: The fund’s ownership decreased from 28.39% to 25.37%, a divestment of approximately 3.02 percentage points.

- •Stated Purpose: The reason cited for the transaction was purely for investment purposes, likely portfolio rebalancing or profit-taking.

While a large institutional sell-off can create short-term downward pressure, it’s crucial to analyze the context. The fund still retains a significant 25.37% stake, indicating continued belief in the company’s long-term value proposition. For a deeper understanding of how private equity firms operate, you can review our guide on understanding private equity exit strategies.

The key for investors is to distinguish between a short-term liquidity event and a fundamental change in the company’s outlook. Our analysis suggests IT-CHEM’s core growth story remains intact.

Core Business & Growth Drivers of IT-CHEM Co., Ltd.

IT-CHEM operates at the intersection of two high-growth industries: pharmaceuticals and advanced electronics. Its competitive advantage is built on differentiated technology and strategic diversification.

1. Advanced Pharmaceutical Materials

The company’s foundation is in producing APIs (Active Pharmaceutical Ingredients) and intermediates for chronic disease treatments, providing a stable revenue stream. However, the future excitement lies in next-generation materials:

- •Oligopeptides & Oligonucleotides: These are the building blocks of modern therapeutics, including gene therapies and mRNA technologies. IT-CHEM’s investment in this area positions it to capitalize on the booming biotech sector.

2. High-Performance Electronic Materials (OLED)

IT-CHEM is a key supplier of core materials for OLED displays. Its competitive edge is being sharpened by strategic technological advancements:

- •Domestic Heavy Water (D2O) Technology: Developing a domestic source for D2O is a significant moat. Heavy water is used to improve the lifespan and efficiency of OLED materials, a critical factor for display manufacturers. For more on this, see this article on advanced display technologies.

- •Major Supply Contracts: A mass production contract with a giant like LG Chem not only validates IT-CHEM’s technology but also secures a significant revenue pipeline.

Financial Health Check: An IT-CHEM Analysis (H1 2025)

The financial snapshot from the first half of 2025 presents a mixed picture, reflecting a company in a heavy investment phase.

- •Revenue & Profitability: Revenue saw a year-over-year decrease, leading to a consolidated operating loss. This was primarily driven by a dip in commodity sales and increased financial costs related to its recent KOSDAQ listing.

- •Debt Ratio: The debt ratio rose to 166.63%. While high, this is largely attributable to strategic capital expenditures for facility expansion and R&D—investments crucial for future growth.

- •Cash Flow: Encouragingly, operating cash flow remained positive, indicating the core business is still generating cash. Negative investment cash flow confirms the heavy spending on future-proofing the company.

Investor Action Plan: What to Do with IT-CHEM Stock Now?

The recent IT-CHEM investment landscape is defined by a tug-of-war between short-term headwinds and long-term potential. Prudent investors should adopt a cautious but watchful approach, focusing on these key performance indicators:

- •Path to Profitability: Monitor the next few quarterly reports for a return to operating profitability. Look for margin improvements as new, higher-value products come online.

- •New Business Traction: Watch for announcements related to the commercialization of oligopeptides and the domestic D2O production. Are these translating into tangible revenue?

- •Financial Deleveraging: Track the company’s efforts to manage its debt ratio. Is the capital raised from the KOSDAQ listing being deployed efficiently to generate returns that outpace its cost?

In conclusion, while the PE sell-off creates noise, the fundamental growth story for IT-CHEM Co., Ltd. remains compelling. The company possesses significant long-term potential but must navigate short-term financial pressures. For investors with a longer time horizon, any price weakness could present a strategic entry point, provided that diligent monitoring confirms the company is executing on its growth strategy.

Disclaimer

This report is for informational purposes only and is based on publicly available information. It does not constitute investment advice. The ultimate responsibility for investment decisions lies with the individual investor.