The JAEYOUNG SOLUTEC stock (049630) has entered a period of scrutiny following a significant disclosure. The ‘J&Moorim Jade New Technology Investment Association’ announced the sale of a substantial 6.46% stake in the company. This move, stemming from a strategic shift to exercise conversion rights and liquidate shares, has sent ripples through the investment community. As the sole South Korean manufacturer of all key smartphone camera components like OIS, ENCODER, and VCM, Jaeyoung Solutec’s market position is unique. This article provides a comprehensive analysis of the stake sale, its potential impact on the JAEYOUNG SOLUTEC stock, and a forward-looking investment strategy based on its fundamentals and industry landscape.

Deconstructing the Major Stake Sale Disclosure

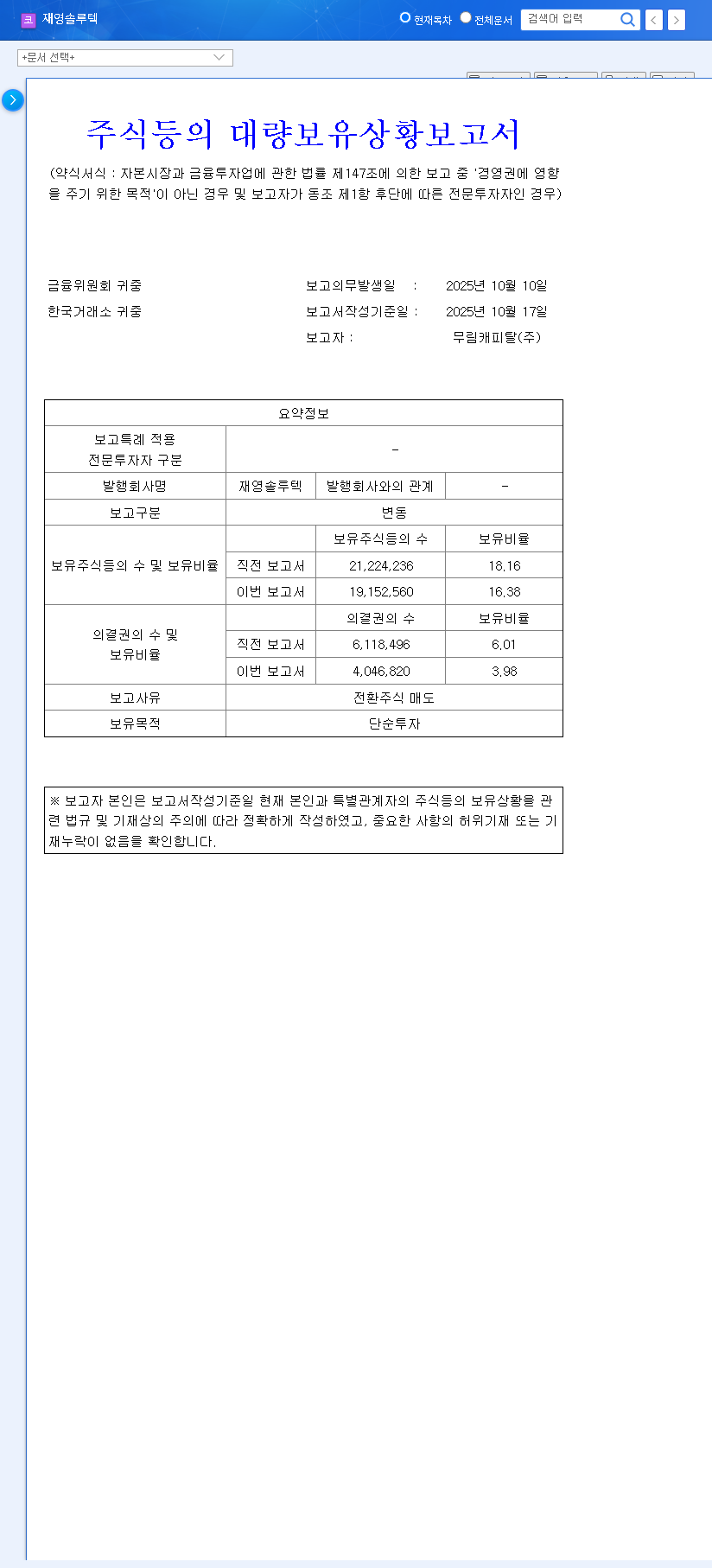

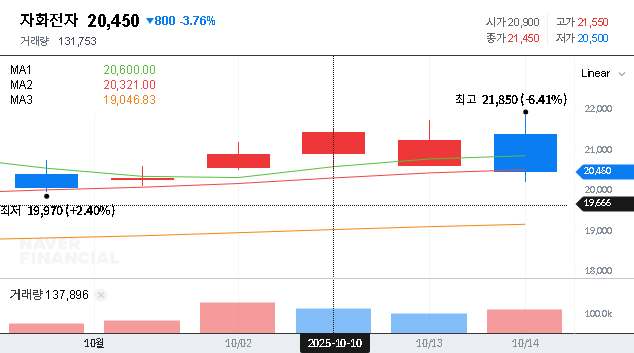

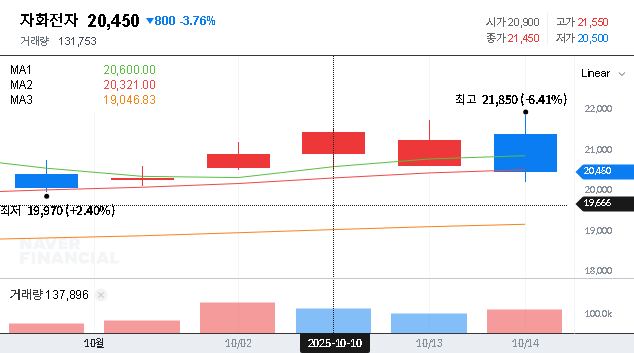

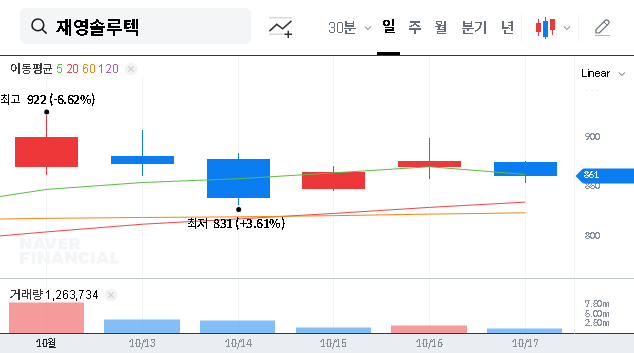

On November 13, 2025, a pivotal filing revealed that the ‘J&Moorim Jade New Technology Investment Association’ had significantly reduced its holdings in JAEYOUNG SOLUTEC. Their stake was halved from 12.92% down to 6.46%. The reason cited was a change in holding purpose from ‘simple investment’ to the ‘exercise of conversion rights and sale of converted shares.’ This essentially means the investment fund converted its debt-based securities into equity and immediately sold them on the open market. You can view the Official Disclosure (DART) for precise details. This action often signals an investor’s desire to realize profits or exit a position, creating potential short-term supply pressure on the stock.

While the sale creates short-term uncertainty, the long-term trajectory for JAEYOUNG SOLUTEC stock will ultimately be dictated by its fundamental performance and its ability to capitalize on the growing high-performance camera market.

Deep Dive: Company Fundamentals and Market Environment

Analyzing JAEYOUNG SOLUTEC’s Financial Health

The company’s financial picture is a mixed bag, showing signs of both strength and areas requiring close monitoring.

- •Strong Revenue Growth: Cumulative sales for Q3 2025 surged by an impressive 33% year-over-year. This growth is directly tied to the increasing complexity and demand for advanced smartphone camera modules, a trend that plays to the company’s strengths.

- •Profitability Pressures: Despite higher sales, cumulative operating profit saw a sharp decline. This compression in margins is attributed to a trio of factors: rising raw material costs, unfavorable exchange rate fluctuations, and strategic increases in R&D spending to maintain a technological edge.

- •Encouraging Q3 Turnaround: On a positive note, the third quarter itself saw a successful return to profitability. This suggests that cost control measures or favorable pricing may be starting to take effect, a key trend for investors to watch in Q4.

- •Financial Structure Concerns: The debt-to-equity ratio, while improving, remains high at around 150%. Furthermore, a negative operating cash flow indicates the company is currently spending more to run its business than it’s bringing in, a situation that warrants careful monitoring. Investors should look for improvements in the company’s cash flow management strategies in upcoming reports.

Industry Tailwinds and Macroeconomic Factors

JAEYOUNG SOLUTEC operates within a dynamic global market influenced by several key factors.

Smartphone Camera Market Evolution: The demand for high-performance smartphone cameras is relentless. The market is rapidly moving towards multi-camera systems, larger sensors, and advanced optical image stabilization (OIS). As the only Korean firm producing all critical components (OIS, ENCODER, VCM), Jaeyoung Solutec is uniquely positioned to benefit from these advanced camera technology trends.

Economic Climate: Stable interest rates in the US and Korea could ease corporate financing burdens. Meanwhile, relatively stable oil prices and shipping costs help contain operational expenses. However, the depreciation of the Korean Won is a double-edged sword: it boosts the value of export revenues but also increases the cost of imported raw materials.

Investment Outlook: Navigating the Volatility

Short-Term vs. Long-Term Impact

The immediate aftermath of the stake sale is likely to be negative for the JAEYOUNG SOLUTEC stock price. The sudden influx of 6.46% of the company’s shares creates an ‘overhang,’ meaning there is significant selling pressure that can depress the price and dampen investor sentiment. However, it’s crucial to recognize that this is a technical event, not a fundamental one. The sale does not change the company’s technology, its customer base, or its role in the supply chain. Over the mid-to-long term, these fundamental factors will reassert themselves as the primary drivers of the stock’s value.

Investment Strategy: A Neutral Stance with Key Monitors

Given the short-term technical pressure balanced by long-term fundamental potential, a Neutral investment opinion is warranted. For prospective or current investors, a patient and watchful approach is recommended. Here are the key areas to monitor:

- •Sustained Earnings Improvement: The Q4 and subsequent earnings reports will be critical. Investors need to see if the Q3 profit turnaround was an anomaly or the beginning of a sustainable trend.

- •Financial Discipline: Look for concrete steps to improve the balance sheet, such as reducing the high debt-to-equity ratio and bringing operating cash flow back into positive territory.

- •Technological Innovation and Customer Wins: Pay attention to announcements regarding next-generation component development or contracts with new smartphone manufacturers, as these will be the primary long-term growth catalysts.

Conclusion: The major stake sale introduces short-term headwinds for the JAEYOUNG SOLUTEC stock. Cautious investors should wait for the market to absorb this new supply. However, the company’s unique technological position in a growing market presents a compelling long-term story. Diligent monitoring of its financial and operational progress is the most prudent path forward.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It should not be considered investment advice. All investment decisions should be made with personal discretion and responsibility.