This comprehensive SK eternix financial analysis delves into the company’s challenging Q3 2025 performance ahead of its pivotal Investor Relations (IR) event. With a dramatic decline in revenue and a precarious surge in debt, investors are keenly watching to see if management can present a credible turnaround strategy. We will break down the numbers, analyze the external pressures, and provide a checklist of what to watch for during the SK eternix IR event.

As SK eternix Co., Ltd. prepares for its Q3 2025 earnings release on November 17, 2025, the stakes have never been higher. The company is at a critical juncture, facing significant financial headwinds that threaten its stability. This event is not just a routine update; it’s an opportunity to rebuild trust and chart a new course for the future. For any serious investor, understanding the details of the SK eternix Q3 2025 earnings is essential for making informed decisions.

Deep Dive: SK eternix Q3 2025 Earnings Breakdown

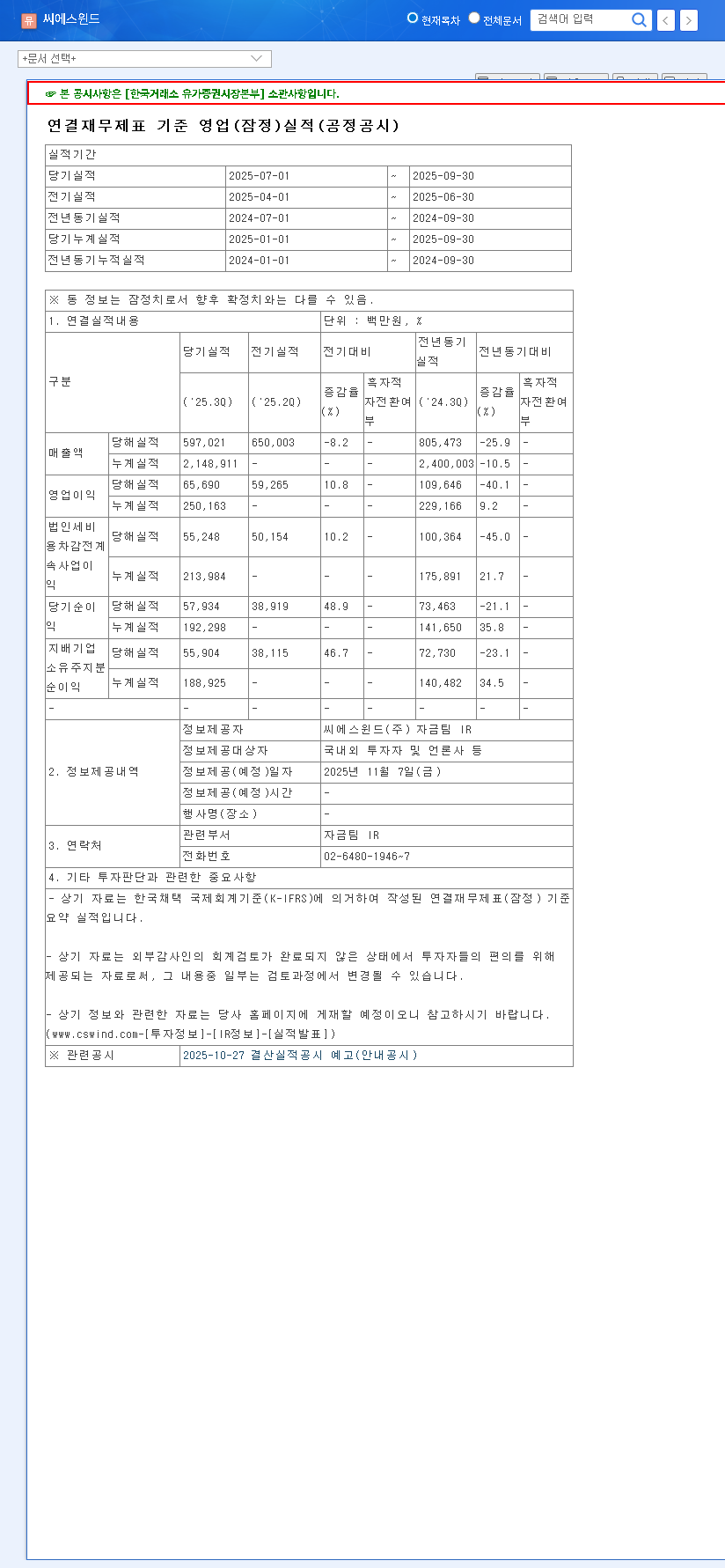

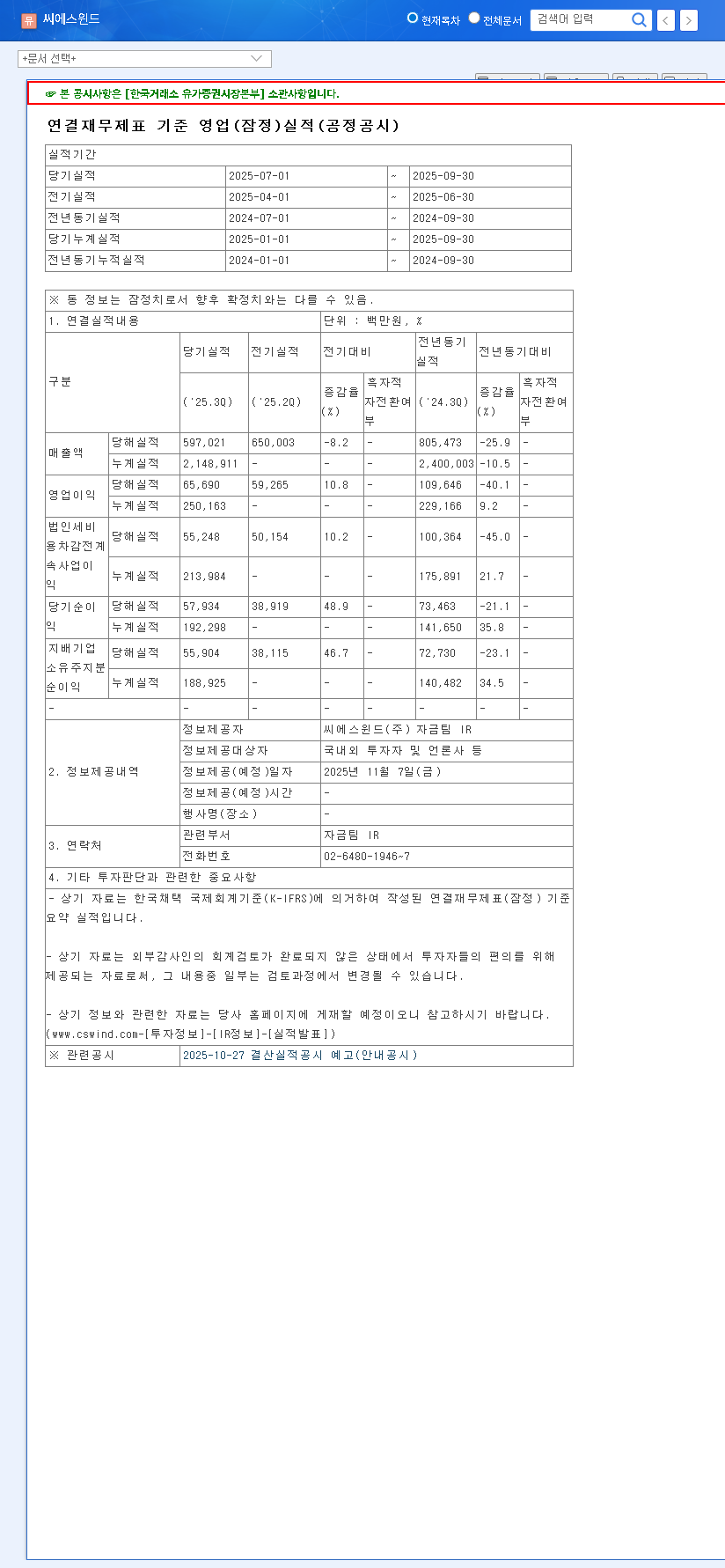

The preliminary numbers, detailed in the official disclosure (Source), paint a concerning picture. Let’s examine the core financial changes that are causing alarm among stakeholders.

1. Alarming Decline in Revenue and Profitability

The top-line and bottom-line figures are stark. For the first nine months of 2025, cumulative revenue fell by a staggering 58.6% year-on-year to KRW 137.7 billion. The impact on profitability was even more severe, with operating profit declining by 68.6% to just KRW 11.8 billion. The primary driver behind this collapse is the complete absence of product sales in its renewable energy business segment, a cornerstone of its operations. This raises fundamental questions about demand, project pipelines, and market competitiveness.

2. Precarious Financial Health: Soaring Debt and Bloated Inventory

The balance sheet reveals equally troubling trends that compound the profitability issue:

- •Skyrocketing Debt Ratio: Total liabilities have ballooned by 143%, pushing the debt ratio to a dangerous 472.13%. A high debt-to-equity ratio can signal excessive risk and limit a company’s ability to secure future financing. The high concentration of current liabilities puts immense pressure on short-term cash flow.

- •Exploding Inventory: Inventory assets swelled by an incredible 9.7 times to KRW 576.9 billion. This suggests either a dramatic miscalculation of demand or significant project delays, tying up valuable capital and risking future write-downs.

Despite these challenges, a notable improvement in operating cash flow to KRW 81.4 billion and a net inflow from financing activities of KRW 79.6 billion offer a sliver of hope, indicating the company is still able to secure capital and manage its day-to-day cash needs. The key question is how this new capital will be used.

The IR Event: A Turning Point for the SK eternix Stock?

The upcoming SK eternix IR event is a make-or-break moment. The company’s management must address investor concerns head-on. The market’s reaction will hinge on the clarity and credibility of their strategic response.

Short-Term Impact: Rebuilding Confidence

A positive outcome requires a transparent explanation for the poor performance and, more importantly, a detailed, actionable plan. If management presents a concrete strategy for deleveraging the balance sheet and reigniting growth in new ventures like offshore wind power, it could stabilize the SK eternix stock price. Conversely, vague promises or a failure to address the inventory and debt issues will likely lead to further sell-offs.

Long-Term Impact: The Viability of New Growth Engines

Long-term success depends on the company’s pivot to new, sustainable revenue streams. Investors will be scrutinizing plans for ventures like offshore wind and Virtual Power Plant (VPP) platforms. A VPP is a cloud-based distributed power plant that aggregates the capacities of various energy resources. For a deeper understanding, you can review our guide to renewable energy technologies. If SK eternix can provide a credible roadmap with clear timelines, funding plans, and projected returns for these new businesses, it could set the foundation for a long-term recovery and re-rate the company’s valuation.

Investor Checklist: Key Questions for the SK eternix IR Event

Investors should go into the IR with a clear set of questions. A thorough SK eternix financial analysis demands answers to the following:

- •Profitability Recovery: What specific actions will be taken to restart product sales in the renewable energy sector?

- •Debt Management: What is the detailed, step-by-step plan to reduce the 472.13% debt ratio to a manageable level?

- •Inventory Strategy: How will the company liquidate KRW 576.9 billion in excess inventory without incurring massive losses?

- •New Business Roadmap: What are the concrete timelines, capital expenditure plans, and expected revenue contributions from offshore wind and VPP projects?

- •Risk Mitigation: What hedging strategies are in place to counter the negative impacts of currency volatility and sustained high interest rates?

In conclusion, the SK eternix investment thesis is currently under severe pressure. The Q3 2025 IR is a critical test of leadership’s ability to navigate this crisis. By listening carefully for clear, data-driven answers to these crucial questions, investors can determine whether this is a company in terminal decline or a value opportunity on the cusp of a major turnaround.