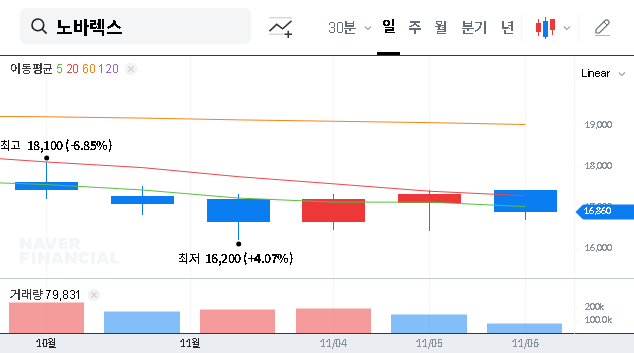

The recent NOVAREX shareholding disclosure has captured the attention of the investment community, sparking discussions about management’s confidence and the company’s future trajectory. While the report showed no change in the overall stake, a small open-market purchase by a related party, with the stated purpose of influencing management, offers a nuanced signal. This article provides a comprehensive NOVAREX investment analysis, delving into the disclosure’s details, the company’s robust fundamentals, and the strategic outlook for investors.

We will move beyond the surface-level numbers to uncover what this event truly signifies for NOVAREX stock and its position as a leading health functional food OEM powerhouse.

Deconstructing the NOVAREX Shareholding Disclosure

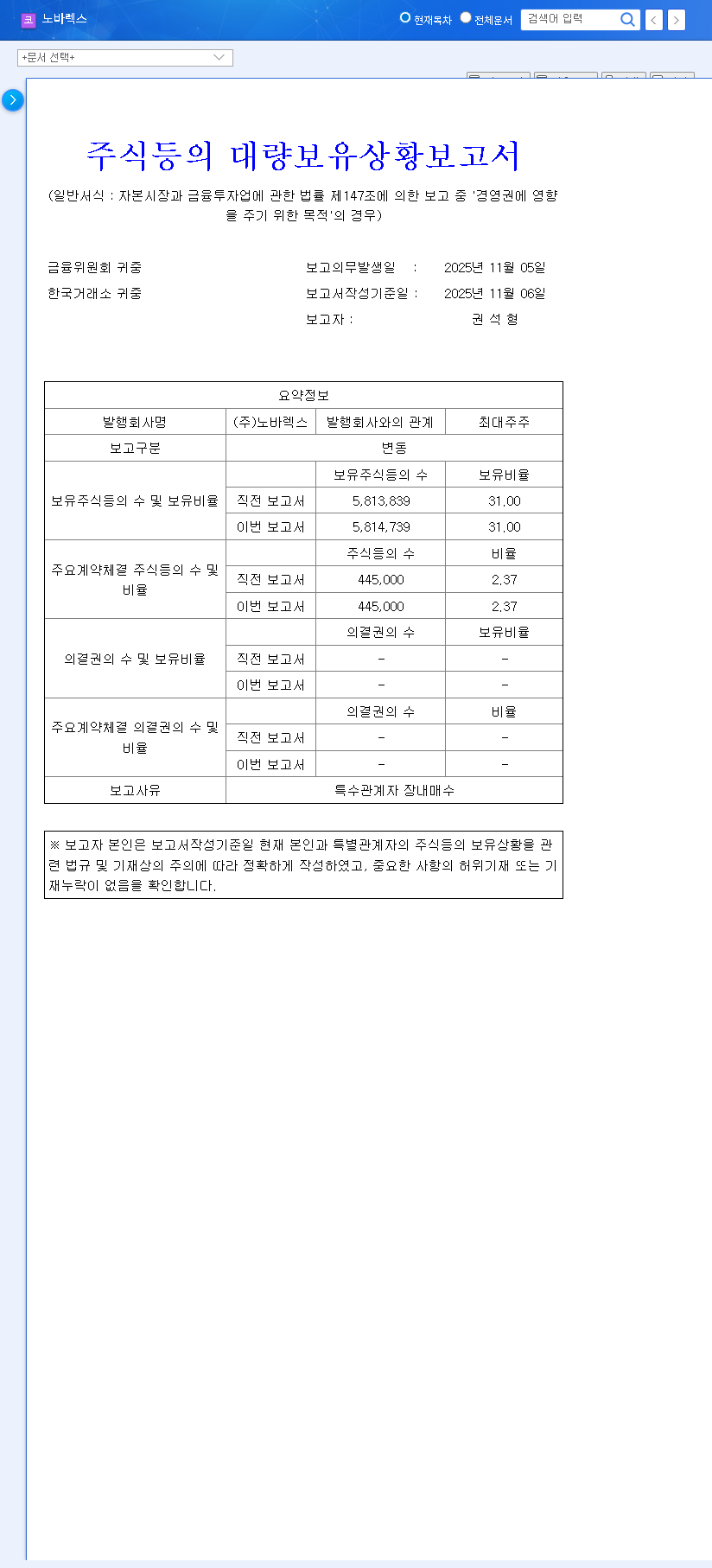

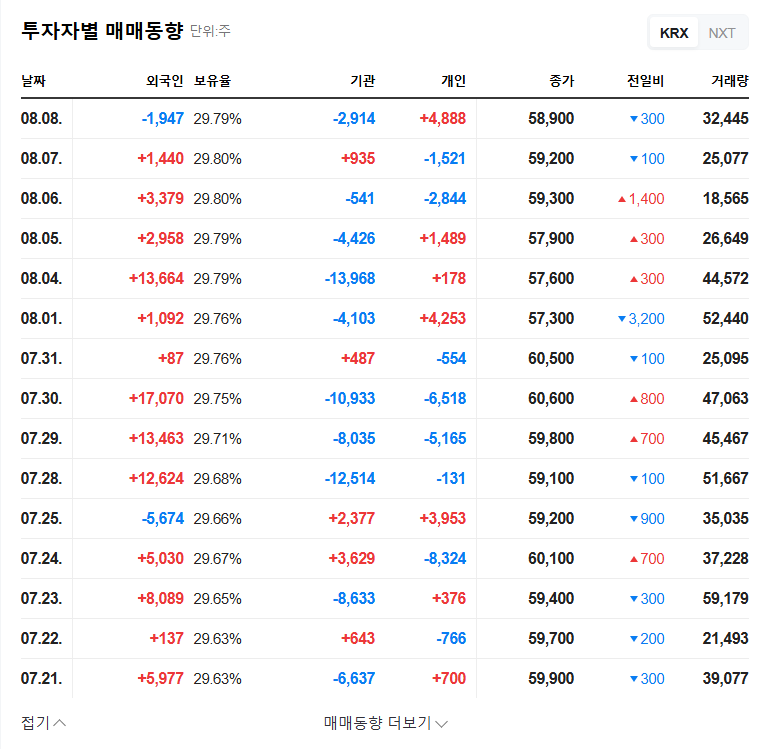

On November 6, 2025, NOVAREX (stock code: 194700) filed its ‘Report on the Status of Large Shareholdings’. The report, which can be viewed in its entirety via the Official Disclosure (DART), outlined the holdings of Chairman Kwon Seok-hyung and a related party, Lee Sang-gu. Here are the critical takeaways:

- •Reporting Parties: Chairman Kwon Seok-hyung and related party Lee Sang-gu.

- •Stated Purpose: To exert influence on management rights.

- •Change in Holdings: The total stake remained static at 31.00%.

- •Reason for Report: A minor open market purchase of 900 common shares by the related party.

While the transaction size is small, the context is key. Such an action, coupled with the explicit mention of ‘influence on management rights’, is often interpreted as a bullish signal from those with the most intimate knowledge of the company’s operations and future prospects.

Insider purchases, even minor ones, can be powerful indicators of management’s conviction in the company’s long-term value and growth strategy. It signals a belief that the stock is currently undervalued.

NOVAREX’s Strong Fundamentals: The Engine of Growth

The confidence demonstrated in the NOVAREX shareholding disclosure is well-supported by the company’s exceptional performance and strategic positioning within the thriving health and wellness sector. As a leading Original Design Manufacturer (ODM) and Original Equipment Manufacturer (OEM), NOVAREX has built a formidable business.

Dominant R&D and Market Leadership

NOVAREX’s primary competitive advantage lies in its unparalleled research and development capabilities. Holding 46 individually recognized ingredients—the most in Korea—allows the company to offer highly differentiated and effective products to its clients. This R&D prowess has translated into stellar financial results, with semi-annual sales in 2025 reaching KRW 189.7 billion (a 36.7% YoY increase) and operating profit soaring to KRW 19.4 billion (a 78.2% YoY increase).

Global Expansion and Strategic Innovation

The company is not resting on its domestic laurels. NOVAREX has made significant inroads into the global market, particularly in Asia, where it recorded an impressive export growth rate of 77.3%. Furthermore, its focus on innovation is evident in its marketing efforts targeting the MZ generation and the development of convenient formulations like ‘MiLi’. To learn more about this segment, you can read our deep dive into the Health Functional Food market.

Market Impact and Strategic Outlook

Given that there was no substantial change in shareholding, the immediate, direct impact on NOVAREX stock is expected to be limited. However, the long-term implications are more significant.

- •Boosted Investor Sentiment: This act of confidence can reassure existing shareholders and attract new investors looking for stable companies with committed leadership.

- •Long-Term Price Support: A strong insider presence can provide a floor for the stock price during market downturns and build momentum for future appreciation.

- •Focus on Governance: The ‘management rights’ clause may draw more attention to the company’s corporate governance and strategic long-term plans.

However, investors must also consider external macroeconomic factors. Global trends, such as fluctuating interest rates and currency exchange rates, can impact financing costs and export profitability. According to reports from leading financial analysts, supply chain stability and raw material costs remain key variables to monitor in the consumer goods sector.

Investor Action Plan & Conclusion

This NOVAREX investment analysis suggests that the recent disclosure should be viewed as a positive reaffirmation of the company’s long-term growth story. For prospective and current investors, the path forward involves:

- •Focus on Fundamentals: Continue to monitor NOVAREX’s sales growth, profit margins, and R&D pipeline as the primary drivers of value.

- •Monitor Financial Health: Keep an eye on operating cash flow and debt levels to ensure growth is sustainable.

- •Adopt a Long-Term Perspective: View this disclosure not as a short-term trading signal, but as a piece of a larger puzzle confirming a solid, long-term investment thesis.

In conclusion, NOVAREX is well-positioned to capitalize on the expanding health functional food OEM market. The management’s recent actions, though small, provide a compelling vote of confidence in the company’s bright future.