The recent adjustment in the National Pension Service’s (NPS) holding of Hwaseung Enterprise stock has sent ripples through the investment community, prompting a closer look at the company’s trajectory. While institutional moves are noteworthy, a savvy investor knows that the real story lies deeper within the company’s core health. This comprehensive Hwaseung Enterprise analysis moves beyond the headlines to dissect the company’s fundamental strengths and weaknesses, evaluate the pressing macroeconomic challenges, and provide a clear, actionable outlook for anyone considering the 241590 stock.

We’ll explore whether the NPS’s decision is a minor portfolio tweak or a signal of underlying issues, giving you the insights needed to navigate your investment strategy with confidence.

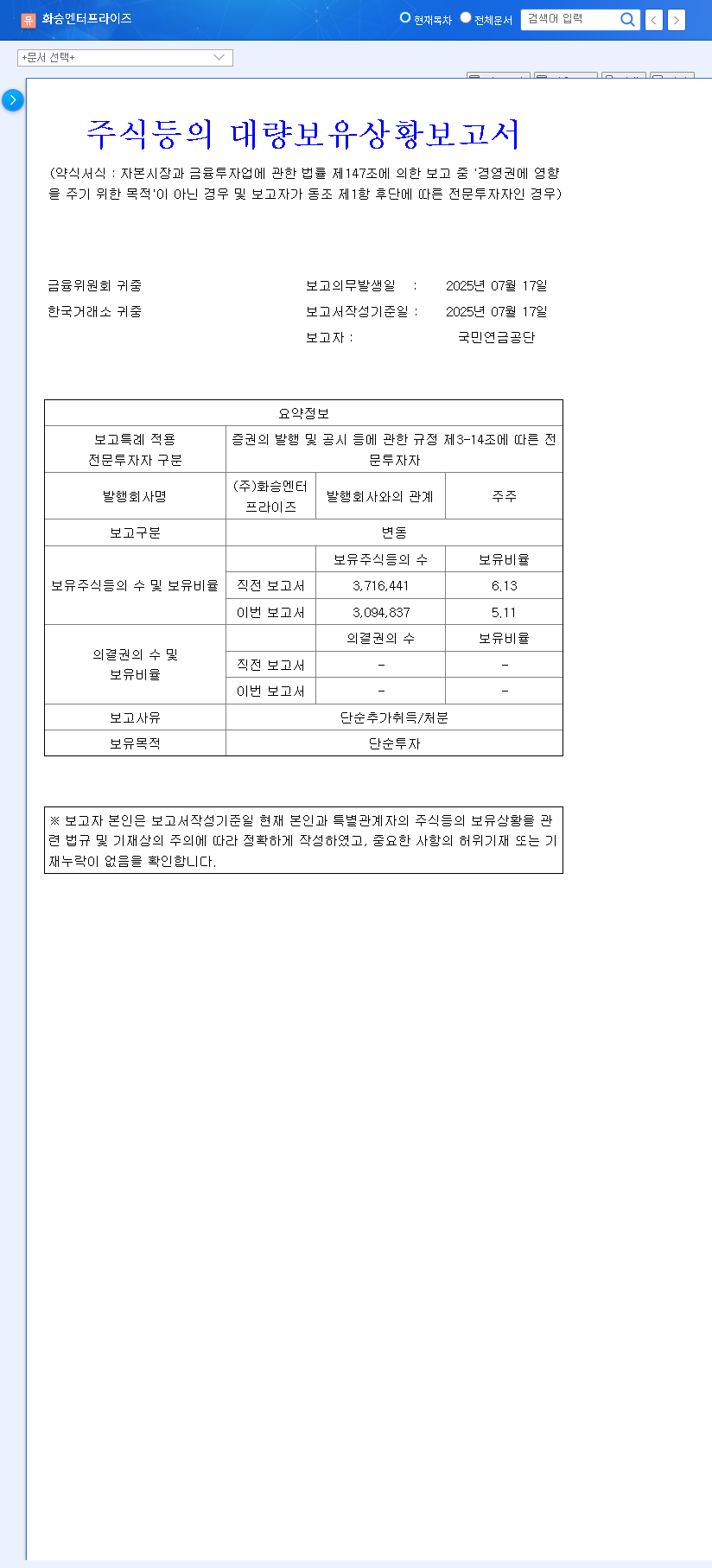

The Catalyst: Unpacking the NPS Stake Reduction

On October 1, 2025, the National Pension Service officially reported a change in its significant shareholding in Hwaseung Enterprise. The disclosure revealed a decrease in its stake from 6.13% down to 5.11%, a reduction of 1.02 percentage points. You can view the Official Disclosure on DART for complete details.

Crucially, the NPS maintained its holding purpose as ‘simple investment.’ This classification is significant. It implies the stake is held for capital gains and not for influencing management or exercising shareholder activism. Therefore, this reduction is most likely a strategic portfolio rebalancing or a simple profit-taking maneuver rather than a vote of no confidence in the company’s long-term Hwaseung Enterprise fundamentals.

Deep Dive: A Fundamental Analysis of Hwaseung Enterprise (241590)

The true value of any stock is rooted in its fundamentals. Based on the 2025 semi-annual report, Hwaseung Enterprise presents a mixed, but concerning, financial picture.

ODM Segment Growth vs. Profitability Squeeze

The company’s core ODM (Original Development Manufacturing) business, which designs and produces goods for other brands, continues to show resilience. Revenue from this segment hit 808 billion KRW, marking a solid year-over-year increase. This growth underscores a stable and robust partnership with its primary client, the Adidas Group.

However, top-line growth did not translate to bottom-line success. Consolidated net income alarmingly swung to a loss of 9.16 billion KRW. This stark decline was driven by significant translation losses from overseas operations (31 billion KRW) and escalating financial costs, eroding the gains made in revenue.

Financial Health and Adidas Dependency Risks

A closer look at the balance sheet reveals areas requiring urgent attention. The financial structure of the Hwaseung Enterprise stock is a key concern for investors.

- •High Debt Ratio: The debt-to-equity ratio stands at a concerning 168.23%. This level of leverage increases financial risk, especially in a high-interest-rate environment.

- •Liquidity Strain: With total borrowings of 616.2 billion KRW vastly outweighing cash and cash equivalents of just 95.7 billion KRW, the company’s liquidity position is tight.

- •Customer Concentration: The deep relationship with Adidas ensures stable orders, but this over-reliance is a double-edged sword. Any shift in Adidas’s performance, strategy, or supplier relationships could directly and severely impact Hwaseung’s revenue stream.

The Bigger Picture: Macroeconomic Headwinds

No company operates in a vacuum. For an exporter like Hwaseung Enterprise, global macroeconomic trends are a critical factor. Several external pressures are currently impacting profitability.

- •Exchange Rate Volatility: The volatile KRW/USD exchange rate has been a primary source of pain, leading to substantial foreign exchange translation losses. As revenue is often denominated in USD while some costs are in KRW, a fluctuating rate creates significant accounting and cash flow challenges.

- •Persistent High Interest Rates: Elevated benchmark rates globally directly increase the cost of servicing Hwaseung’s large debt pile. This is a direct drain on profitability that is unlikely to ease in the short term. To learn more, explore this overview of global interest rate policies from authoritative sources like Reuters.

Future Outlook & Investment Strategy for Hwaseung Enterprise Stock

Considering all factors, the future of the Hwaseung Enterprise stock price hinges less on the NPS’s minor stake adjustment and more on the company’s ability to navigate its fundamental and macroeconomic challenges. The market has likely priced in the NPS sale; the focus now shifts to operational execution.

Short-Term & Mid-Term Perspective

In the short term, investors should prioritize monitoring fundamental improvement indicators over institutional holdings. Watch for the company’s next quarterly report for any signs of cost control, improved profit margins, and effective currency hedging strategies. Any positive news in these areas could provide a much-needed catalyst for the stock.

Long-Term Investment Thesis

For a long-term position, the investment case rests on Hwaseung’s ability to enhance its intrinsic value. Key strategic initiatives to watch for include:

- •Efforts to diversify its client base beyond Adidas to mitigate concentration risk.

- •A clear and credible plan to reduce debt and strengthen the financial structure.

- •Continued innovation in its ODM segment to maintain its competitive edge. You can learn more by reading our guide to evaluating company fundamentals.

In conclusion, while the NPS’s move sparked this conversation, the real focus for any Hwaseung Enterprise stock analysis must be on the company’s profitability and balance sheet. The stable ODM revenue provides a solid foundation, but addressing the financial vulnerabilities is the critical task ahead for unlocking shareholder value.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The final responsibility for investment decisions rests with the investor.