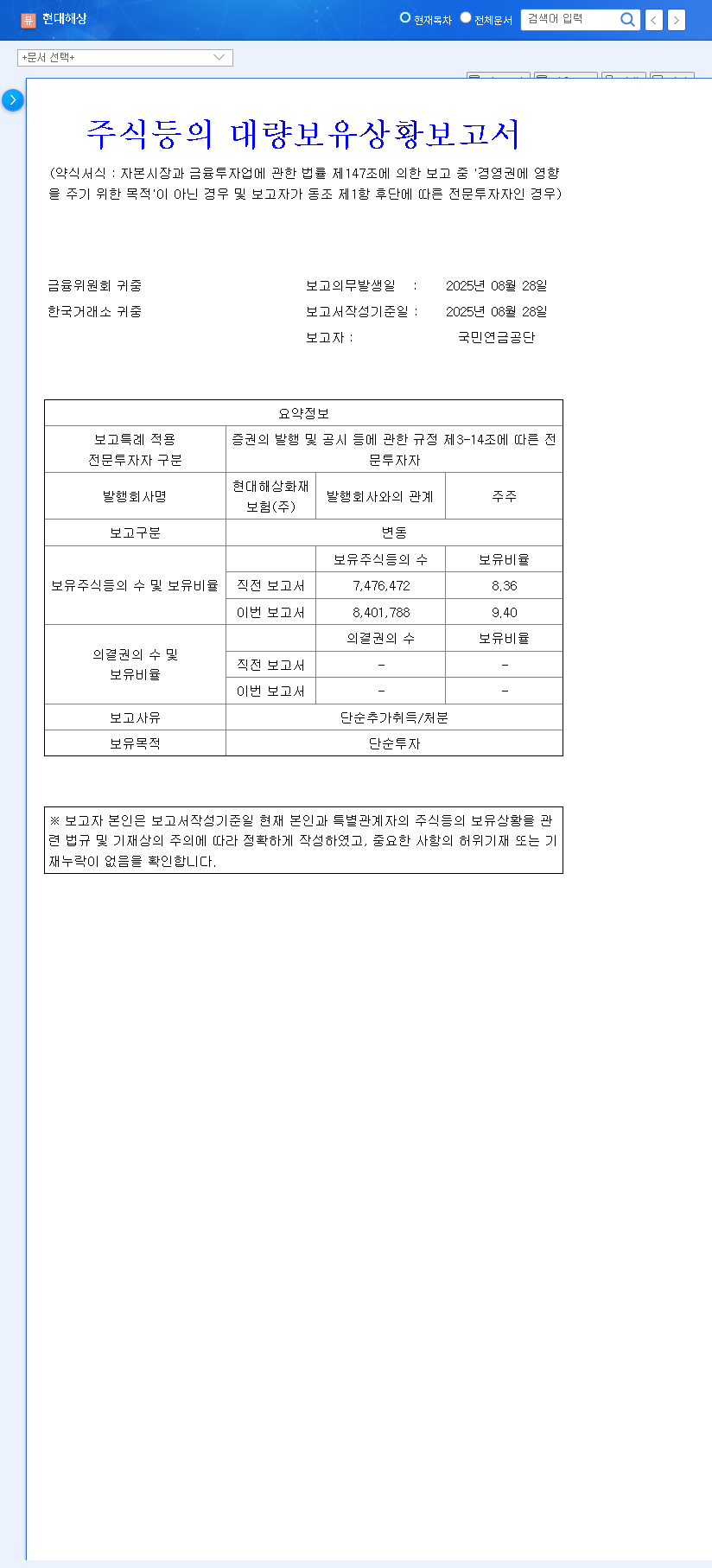

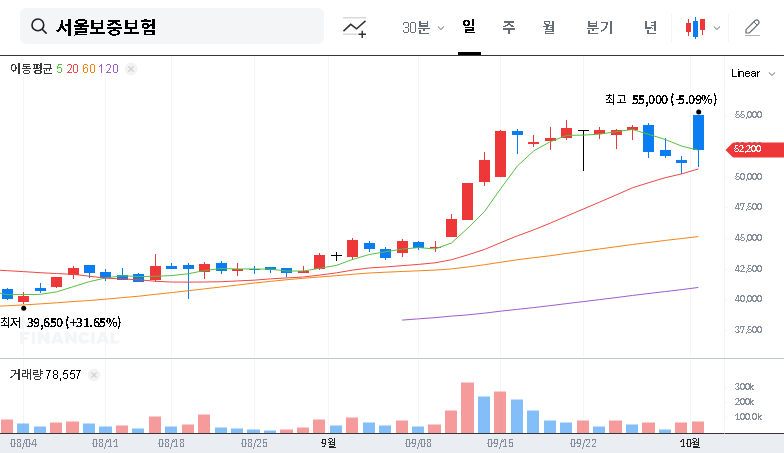

The market is taking notice as South Korea’s largest institutional investor, the National Pension Service (NPS), has significantly increased its stake in Hyundai Marine & Fire Insurance (001450). This move, raising their holding to 9.40%, is widely interpreted as a strong vote of confidence in the insurer’s financial health and future trajectory. For savvy investors, an NPS investment of this scale warrants a closer look.

What does this mean for the 001450 stock price and the company’s long-term value? This comprehensive analysis will break down the specifics of the NPS stake increase, delve into the core fundamentals of Hyundai Marine & Fire Insurance, and provide an actionable roadmap for investors considering their next move.

The Details: Analyzing the NPS Stake Increase

On October 1, 2025, the National Pension Service officially reported its increased shareholding in Hyundai Marine & Fire Insurance. The filing revealed a strategic acquisition that boosts the NPS’s ownership from 8.36% to a substantial 9.40%, an increase of 1.04 percentage points. The stated purpose of ‘Simple Investment’ underscores a belief in the company’s long-term value appreciation rather than a desire for management influence or short-term speculation. You can view the complete Official Disclosure on DART for precise details. This move solidifies the NPS’s position as a key long-term stakeholder in the company.

Is Hyundai Marine & Fire Insurance (001450) a Strong Bet?

To understand the conviction behind the NPS investment, we must dissect the company’s fundamentals. An analysis of its recent performance reveals a compelling picture of strengths balanced with manageable risks.

Key Strengths and Growth Drivers

- •Impressive Financial Performance: H1 2025 showed a 7.2% rise in operating revenue and a staggering 56.3% increase in net income year-over-year, signaling strong operational efficiency and profitability.

- •Solid Financial Health: The company’s solvency ratio stands at a healthy 170.0%, well above regulatory requirements. This is further validated by strong credit ratings from S&P (A/Stable) and A.M.Best (A+/Excellent), providing a cushion against market shocks.

- •Digital Transformation & Channel Diversification: Hyundai Marine & Fire is effectively expanding its online (CM) channels and strengthening its presence in GA channels, successfully targeting younger demographics like millennials and Gen Z. This strategy is crucial for future growth in a competitive market.

- •Commitment to Shareholder Value: The company’s active shareholding management and stated intentions for future shareholder return policies are clear positive signals for investors seeking returns through both dividends and capital appreciation.

Potential Risk Factors to Monitor

- •Market Competition: The non-life insurance sector is fiercely competitive. Price wars and aggressive strategies from rivals could potentially squeeze profit margins if not managed proactively.

- •Macroeconomic Volatility: Like all financial institutions, the company is exposed to fluctuations in interest and exchange rates. These external factors can impact investment income and overall profitability.

- •Insurance Income Sensitivity: Profitability can be affected by unforeseen events like natural disasters or changes in claim trends, highlighting the inherent cyclical nature of the insurance business.

Impact on the 001450 Stock Price

The National Pension Service‘s endorsement has both immediate and lasting implications for Hyundai Marine & Fire’s stock.

When an institution with the scale and research capacity of the NPS makes a move, the market listens. It’s not just about the capital inflow; it’s a powerful signal about the underlying quality and long-term potential of the asset.

In the short term, we can expect improved investor sentiment and a potential uptick in trading volume. This institutional confidence can create positive price momentum. In the long term, the impact is more profound. The NPS’s presence enhances the company’s credibility, can contribute to stock price stability, and may lead to a positive re-evaluation of the company’s intrinsic value by the broader market. This aligns with trends seen across global markets, as detailed in reports from authorities like Bloomberg on institutional investment patterns.

Investor Action Plan: Strategic Takeaways

The increased NPS investment in Hyundai Marine & Fire Insurance is a compelling data point, but it should be part of a holistic investment thesis. Here’s how to approach it:

- •Focus on the Long Game: View this news as a confirmation of the company’s fundamental strength. A mid-to-long-term investment horizon is most appropriate to capitalize on the potential for value revaluation and shareholder returns.

- •Monitor Key Metrics: Keep a close watch on the company’s solvency ratio, net income growth, and developments in their digital strategy. These are the core drivers that attracted the NPS in the first place. For more on this, see our guide on how to analyze insurance stocks.

- •Manage Risk: Acknowledge the industry’s competitive nature and macroeconomic sensitivities. A well-diversified portfolio is the best defense against sector-specific risks.

In conclusion, the decision by the National Pension Service to increase its holding in Hyundai Marine & Fire Insurance is a significant and bullish signal. It highlights a company with robust fundamentals, a clear growth strategy, and a commitment to its shareholders. For investors, this serves as a prime opportunity to re-evaluate the 001450 stock as a cornerstone of a long-term, value-oriented investment portfolio.