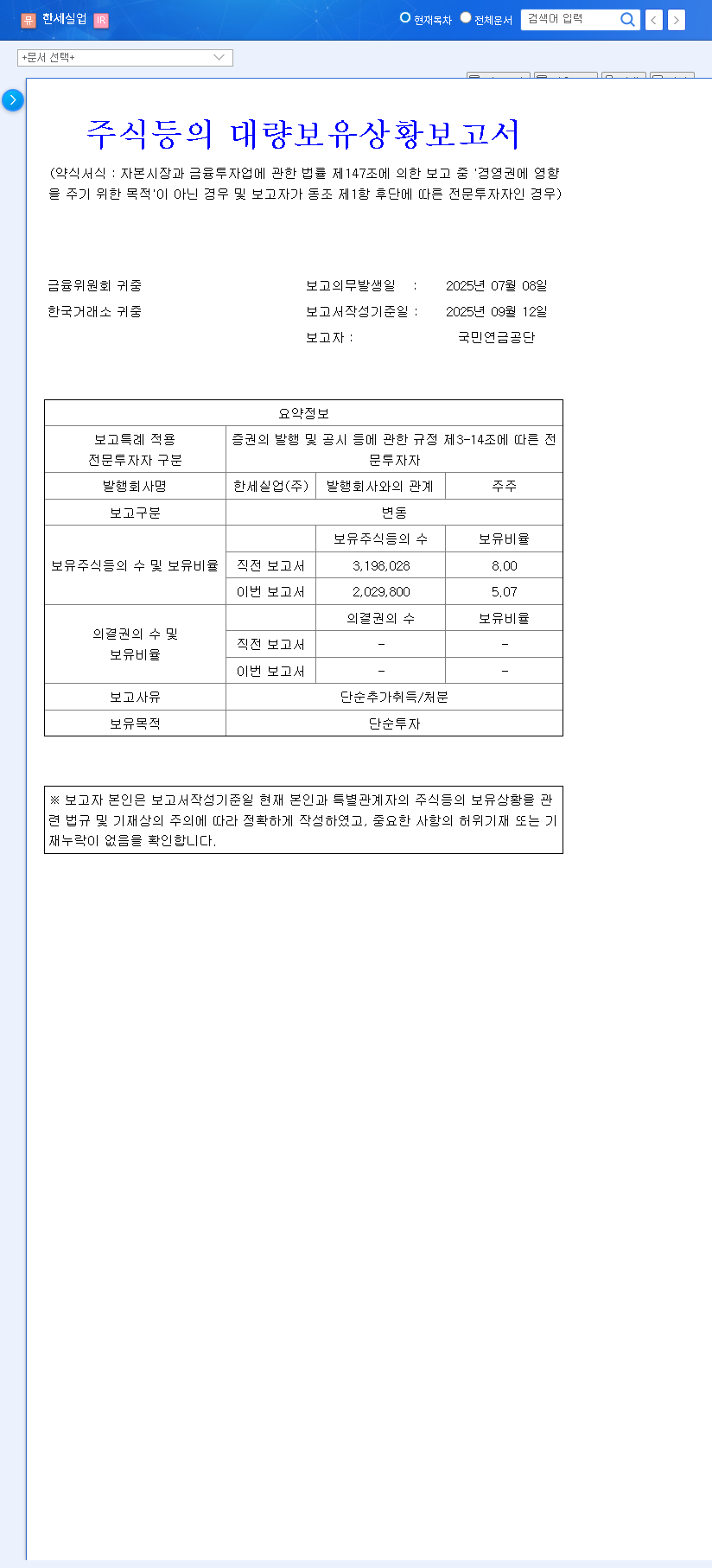

The recent news of the National Pension Service (NPS) reducing its stake in the Hansae Co Ltd stock has sent ripples through the market, leaving many investors wondering about the future. On October 1, 2025, Korea’s largest institutional investor announced a significant 2.93 percentage point reduction in its holdings. This article provides a comprehensive Hansae stock analysis, dissecting the implications of the NPS Hansae sell-off, evaluating the company’s core fundamentals, and outlining a clear Hansae investment strategy to navigate the path forward.

We’ll move beyond the headline to offer a practical, data-driven perspective, helping you make informed decisions about your investment in Hansae Co., Ltd.

The NPS Sell-Off: What Exactly Happened?

According to the ‘Report on Large-Volume Stock Holdings,’ filed on October 1, 2025, the National Pension Service (NPS) confirmed its stake in Hansae Co., Ltd. decreased from 8.00% to 5.07%. This divestment of approximately 2.93% of the company’s shares by such a prominent investor naturally raises questions about both short-term price stability and the long-term outlook for the Hansae Co Ltd stock. The official filing provides the direct details of this transaction (Source: Official Disclosure).

While an institutional sell-off can create short-term volatility, long-term value is ultimately dictated by a company’s fundamental strength and ability to execute its strategy. The key is to separate market noise from business reality.

Hansae’s Fundamental Analysis: A Resilient Growth Engine?

To truly understand the value of Hansae Co Ltd stock, we must look past the NPS’s decision and analyze the company’s intrinsic value. Based on its H1 2025 report, here is a detailed breakdown of its strengths and weaknesses.

Core Strengths and Positive Catalysts

- •Dominant OEM/ODM Business: Hansae maintains a powerful position in the apparel manufacturing industry. Its consistent sales in core categories are built on decades-long, stable relationships with major U.S. retail giants like TARGET, OLD NAVY, and GAP, ensuring a reliable revenue base.

- •Growing Fabric Business: The company is successfully diversifying its revenue streams. The fabric business, led by its subsidiary Color & Touch Co., Ltd., is increasing its contribution to overall revenue and enhancing profitability. The strategic acquisition of TEXOLLINI, INC. is set to further expand this high-margin segment.

- •Strategic Global Footprint: With diversified production bases across the globe, Hansae can effectively manage costs and mitigate geopolitical risks. Furthermore, its vertical integration projects in Central America are poised to become a significant long-term growth driver by streamlining supply chains.

- •Solid Financial Health: The company maintains a healthy balance sheet and strong short-term liquidity, providing resilience against economic downturns and the flexibility to invest in growth opportunities.

Headwinds and Factors to Monitor

- •Recent Profitability Slowdown: A notable concern is the significant decrease in operating profit in H1 2025 compared to the prior year. This dip is likely a combination of rising raw material costs, intensified market competition, and inventory adjustments by major clients.

- •Currency Exchange Risk: With a high proportion of sales denominated in U.S. dollars, Hansae’s profitability is sensitive to fluctuations in the USD/KRW exchange rate. This exposure contributed to foreign exchange losses in the first half of the year.

- •Macroeconomic Pressures: Broader economic conditions, such as high interest rates and fluctuating oil prices, impact consumer spending and operational costs. A high-interest environment, as reported by authoritative economic sources, can dampen consumer sentiment in the apparel sector.

Market Impact and Investment Strategy

The NPS’s move could be interpreted in several ways. It is most likely a routine portfolio rebalancing act rather than a direct vote of no confidence in Hansae’s long-term prospects. However, the market reaction is crucial.

Short-Term vs. Long-Term Outlook

In the short term, the large sell-off will likely create downward pressure on the Hansae Co Ltd stock price due to a simple supply-demand imbalance. It can also create negative investor sentiment as retail investors may follow the institutional lead. In the mid-to-long term, however, the stock’s performance will inevitably re-align with its fundamental business performance. If Hansae can demonstrate improved profitability and execute its growth strategy, the stock price will recover and trend upwards, independent of this single ownership change. For a deeper dive into market trends, you can review our analysis of the global apparel industry.

Investment Thesis: A Cautious ‘Hold’ with Key Monitors

Our current investment opinion is Neutral to Cautiously Optimistic. While Hansae’s business foundation is solid, the recent profitability dip and macroeconomic headwinds warrant a prudent approach. This is not a time for panic selling. Instead, it is a time for diligent monitoring.

Investors should focus on the following key points before making a decision:

- •Upcoming Earnings Reports: Pay close attention to Hansae’s Q3 and Q4 2025 results. Look for signs of margin recovery and improved operating profit.

- •Macroeconomic Indicators: Track trends in the USD/KRW exchange rate, raw material prices (like cotton), and global shipping costs.

- •Client Inventory Levels: Watch for commentary from major retailers about inventory normalization, which would signal a resumption of larger orders for Hansae.

In conclusion, the NPS sell-off is a notable event that creates short-term uncertainty for the Hansae Co Ltd stock. However, for the long-term investor, the focus should remain squarely on the company’s ability to navigate current challenges and capitalize on its fundamental strengths. Any significant dip in share price resulting from this news, if fundamentals begin to show improvement, could represent a compelling buying opportunity for those with a long-term horizon.