A significant move in the Korean market has put F&F stock under the investor spotlight. The National Pension Service (NPS), one of the world’s largest pension funds, has increased its shareholding in the fashion powerhouse F&F. This decision signals strong institutional confidence and raises a critical question for stakeholders: What does this endorsement mean for the future of F&F’s corporate value and its stock price? This comprehensive F&F investment analysis will delve into the company’s robust fundamentals, address current challenges, and examine the potential impact of the NPS’s increased ownership.

Whether you’re a current shareholder or considering an investment, this deep dive provides the clarity needed to understand the forces shaping F&F’s trajectory in the competitive global fashion landscape.

The Catalyst: NPS Increases F&F Shareholding

A Clear Vote of Confidence

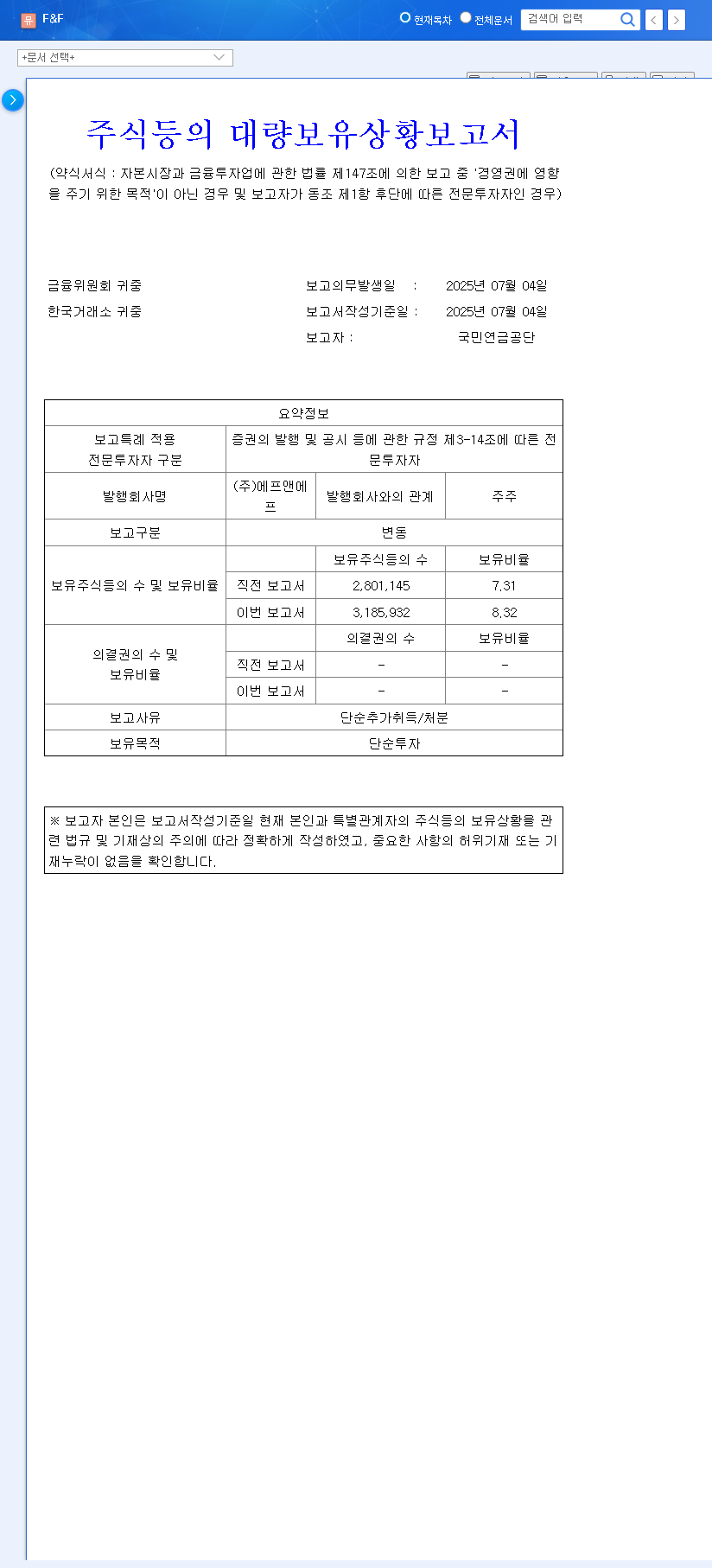

On October 1, 2025, the National Pension Service of Korea formally announced an additional acquisition of F&F shares, increasing its total holding from 7.31% to 8.32%. This 1.01 percentage point increase, detailed in the Official Disclosure (DART Report), is more than just a routine portfolio adjustment. As one of Korea’s most influential institutional investors, the NPS’s actions are closely watched and often interpreted as a strong belief in a company’s long-term viability and growth potential. For a company like F&F, with a market capitalization of KRW 2.47 trillion, such a move underscores institutional conviction in its underlying value.

When an institution with the scale and due diligence of the NPS increases its stake, it’s a powerful market signal. It suggests their analysis points to sustained growth and a favorable risk-reward profile, providing a tailwind for general investor sentiment.

Why F&F? Deconstructing the Core Fundamentals

Global Brand Power and Strategic Expansion

F&F is not just a domestic player; it’s a global fashion contender. The company’s strength lies in its portfolio of high-recognition brands, including MLB, MLB KIDS, DISCOVERY, DUVETICA, SUPRA, and SERGIO TACCHINI. The remarkable success of MLB and DISCOVERY, in particular, has cemented F&F’s reputation for creating culturally resonant and commercially successful products. The strategic expansion into overseas markets, especially China, is a key growth driver. The 2025 half-year report revealed that overseas sales now constitute over 40% of its fashion revenue, a clear indicator of its successful global strategy. For more on institutional investment strategies, see this overview from authoritative financial sources.

- •Proven Brand Portfolio: Brands like MLB have become status symbols, driving high demand and brand loyalty in key Asian markets.

- •Aggressive Global Growth: The focus on China and other international markets provides a massive runway for future revenue growth, diversifying away from the domestic market.

- •Digital Transformation: Ongoing investments in e-commerce and digital marketing are crucial for capturing the modern consumer and strengthening its brand portfolio.

Financial Fortitude vs. Short-Term Hurdles

A core part of this F&F investment analysis is its financial health. As of the first half of 2025, F&F exhibits an exceptionally strong balance sheet with a debt-to-equity ratio of just 10.7%. This financial stability provides a significant buffer against economic headwinds and rising interest rates, allowing the company to invest in growth without being overleveraged.

However, the company did face a profitability slowdown in the first half of 2025, with operating profit declining. This can be attributed to a mix of macroeconomic pressures on consumer spending, intense competition, and the upfront costs associated with its aggressive overseas expansion. Investors should also monitor risks from its outsourced manufacturing model and exchange rate volatility (USD/KRW and EUR/KRW), which can impact margins. If you are interested in this sector, you might also like our Guide to Investing in the Korean Fashion Market.

Investor Takeaways & Future Outlook

Interpreting the Market Signals

The increased F&F shareholding by the NPS is a significant positive indicator. It reinforces institutional confidence in the company’s long-term strategy and can lead to improved stock price stability and potential upward momentum. While this action doesn’t change the F&F fundamentals overnight, it validates the existing positive thesis held by many analysts.

Looking ahead, investors should keep a close watch on several key performance indicators:

- •Quarterly Earnings: Monitor for a rebound in profitability and sustained revenue growth.

- •China Market Performance: Success in this key region is critical to achieving long-term growth targets.

- •Margin Management: Watch how the company navigates exchange rate fluctuations and production costs.

In conclusion, while F&F faces short-term macroeconomic challenges, its strong brand equity, solid financial foundation, and clear global growth strategy present a compelling long-term picture. The NPS’s increased stake serves as a powerful reaffirmation of this potential, making F&F stock a noteworthy name for investors to monitor closely.