The recent news of South Korea’s National Pension Service (NPS) divesting a significant stake in LG H&H stock has stirred the market, leaving many investors questioning the future trajectory of the company’s share price. Is this a signal of underlying weakness, or simply a strategic portfolio adjustment by a major institutional player? This comprehensive LG H&H stock analysis will dissect the situation, providing clarity on the NPS’s actions, the company’s fundamental health, and what it all means for your investment strategy in 2025 and beyond.

The NPS Share Sale: What Investors Need to Know

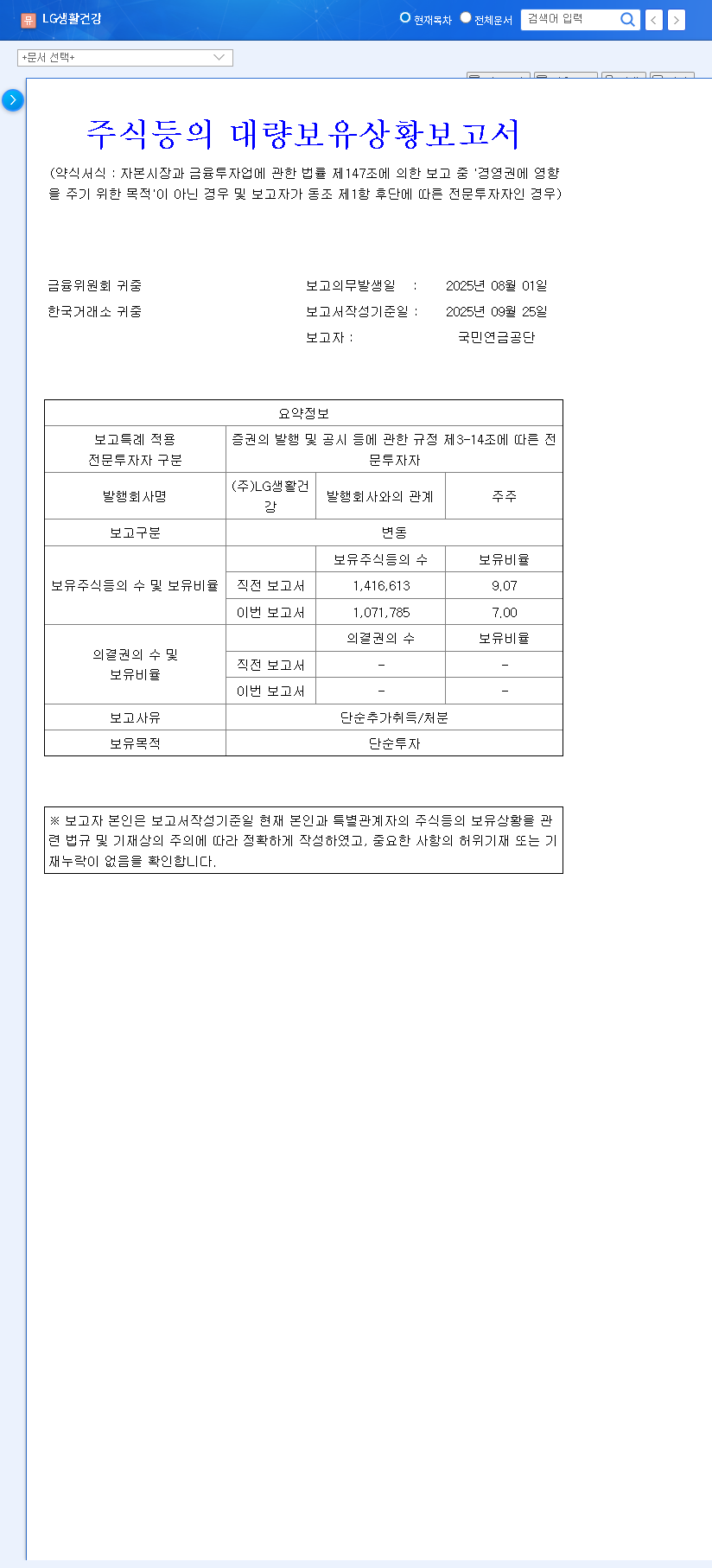

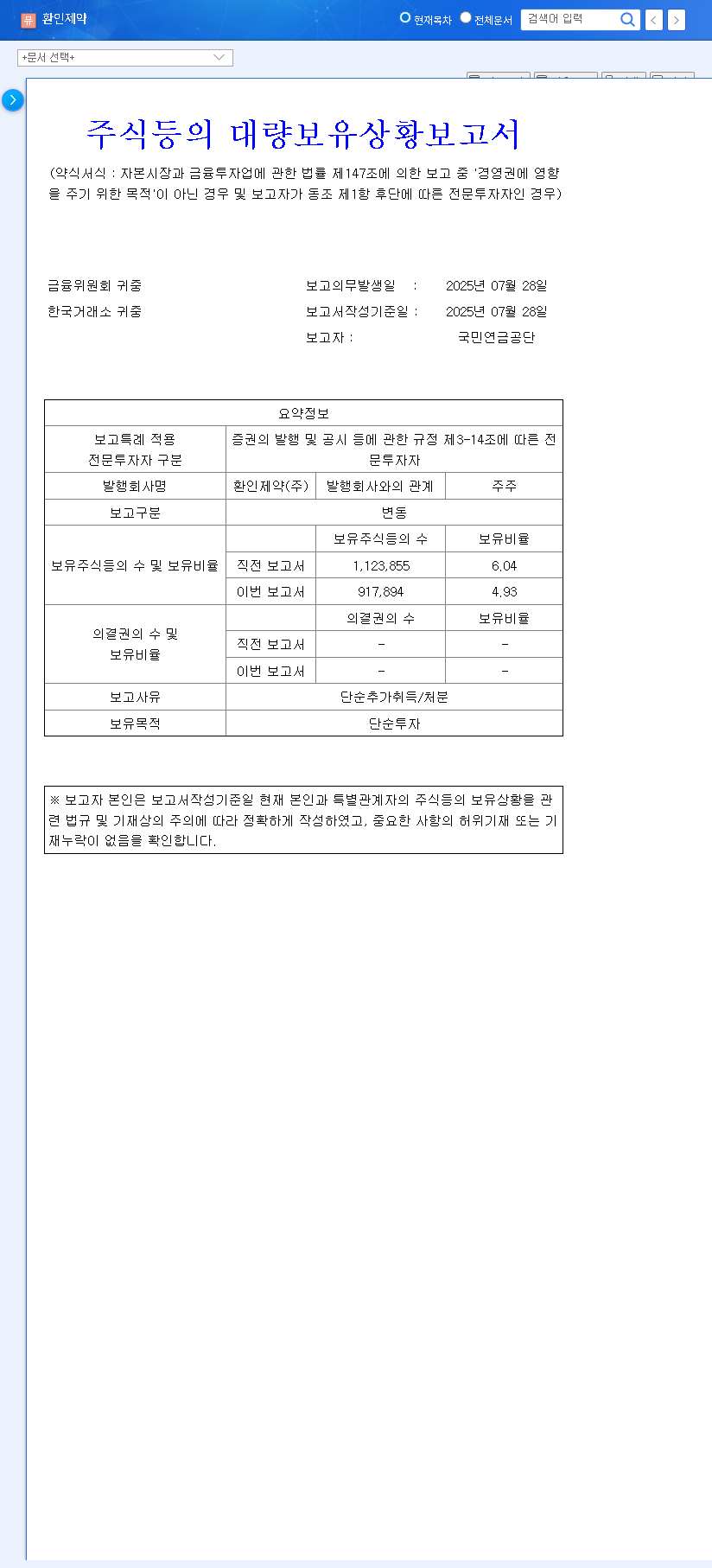

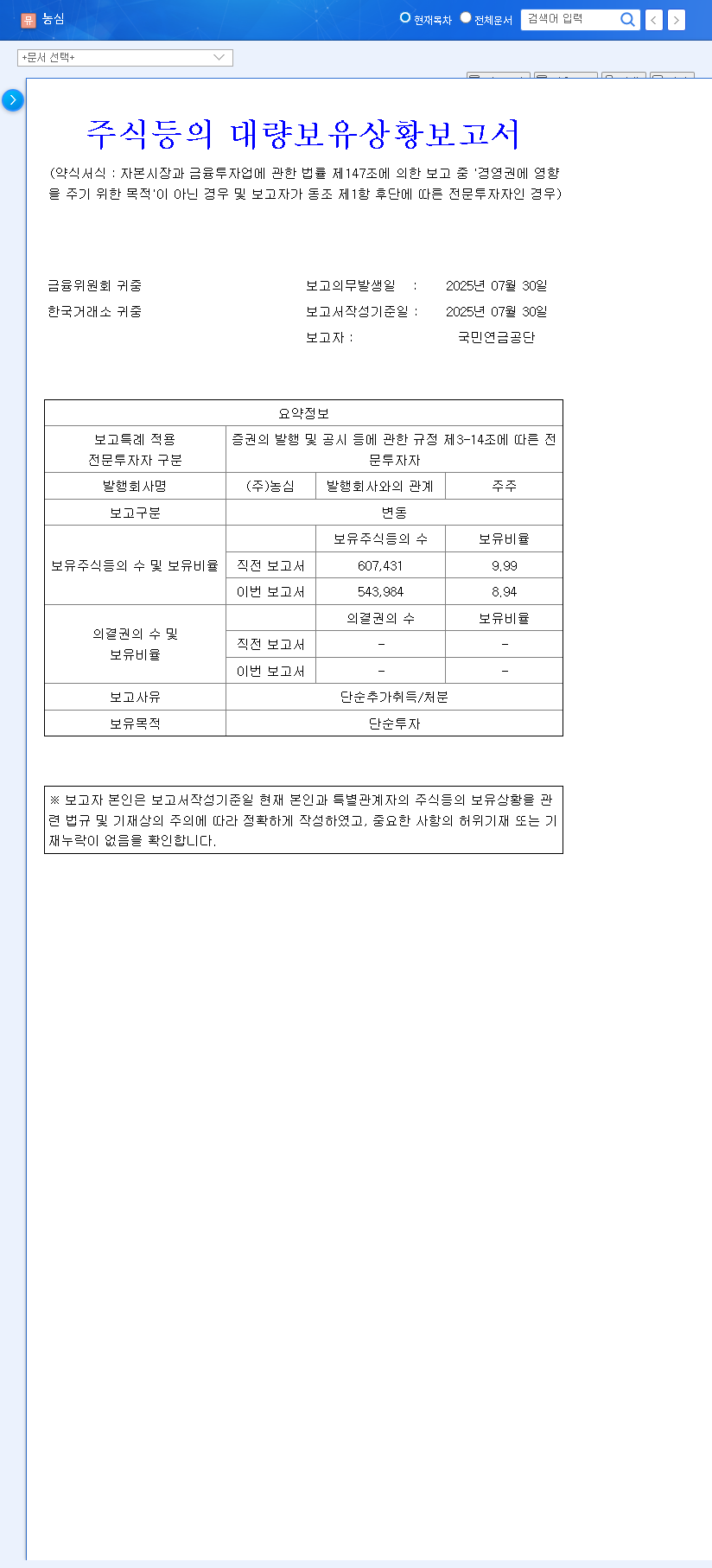

On October 1, 2025, a public disclosure revealed that the National Pension Service, one of the world’s largest pension funds, had reduced its holdings in LG H&H (ticker: 051900). The fund’s stake decreased from 9.07% to 7.00%, a notable reduction of 2.07 percentage points. According to the Official Disclosure, the stated purpose for the holding was ‘Simple Investment’.

This type of move by a major institution can often be interpreted in two ways. On one hand, it could be a strategic rebalancing of their portfolio, a common practice to manage risk or lock in profits after a period of growth. On the other hand, it could be perceived as a loss of confidence in the company’s future prospects. However, given the ‘Simple Investment’ classification, the former is the more probable scenario. The immediate impact is likely to be felt more in market sentiment and short-term volatility rather than as a reflection of a fundamental shift in the LG H&H stock value proposition.

Deep Dive into LG H&H Stock Fundamentals (H1 2025)

Beyond the headlines, a thorough LG H&H stock analysis requires a close look at the company’s core performance. The first half of 2025 painted a picture of resilience amidst challenges.

Revenue and Segment Performance

LG H&H reported total revenue of KRW 3.3 trillion, a marginal decrease year-over-year. The Beauty division, with KRW 1.3 trillion in revenue, felt the headwinds from a sluggish Chinese market, a key area of concern for investors. However, the HDB (Home Care & Daily Beauty) segment showed robust growth, reaching KRW 1.1 trillion, driven by the strong performance of its premium brands. The Refreshment segment remained a pillar of stability, maintaining its revenue at KRW 874.7 billion. This diversified portfolio demonstrates an ability to weather turbulence in specific markets.

Profitability and Financial Health

Operating profit saw a significant drop to KRW 197.2 billion, a 57% decrease year-over-year. This was primarily attributed to increased strategic investments aimed at revitalizing the Beauty segment and some one-off expenses. Despite this, the high-margin Refreshment business provided a crucial buffer, helping to defend overall profitability. Crucially, the company’s financial foundation remains rock-solid.

With a low debt-to-equity ratio of just 20.8% and a healthy reserve of cash equivalents, LG H&H is well-positioned to navigate economic uncertainties and fund future growth initiatives without financial strain.

Market Impact and Future Outlook

Short-Term Volatility vs. Long-Term Value

The immediate aftermath of the NPS news could introduce downward pressure on the LG H&H share price and increase trading volatility. Negative sentiment often follows when a major institution trims its position, a phenomenon frequently covered by leading financial news outlets. However, for long-term investors, this could represent a buying opportunity. The market’s short-term reaction is unlikely to impact LG H&H’s fundamental business competitiveness, brand equity, or its strategic growth plans.

Future Growth Catalysts

Management’s focus in H1 2025 was clearly on securing future growth. Investors should pay close attention to these initiatives, which are far more indicative of long-term value than a single institutional trade. For more on market trends, review our analysis of the global beauty industry.

- •Strengthening Luxury Brands: Continued investment in high-margin luxury cosmetics like ‘The History of Whoo’ and ‘Su:m37’ is key to improving profitability.

- •Strategic Acquisitions: The acquisition of new color cosmetics brands diversifies the portfolio and captures new market segments.

- •Beauty Tech Investment: Venturing into the beauty device business opens up a new, high-growth revenue stream.

- •Shareholder Returns: Ongoing share buybacks and dividends signal confidence from management and a commitment to enhancing corporate value.

Comprehensive Investment Strategy for LG H&H Stock

In conclusion, while the NPS share sale is a notable event, it should be viewed within the broader context of LG H&H’s solid fundamentals and strategic initiatives. The prudent investor will look past the short-term noise and focus on the underlying health and long-term growth trajectory of the business.

Investment Opinion: Neutral with Positive Long-Term Outlook

The current recommendation is ‘Neutral’ due to short-term market headwinds and macroeconomic uncertainties. However, the long-term potential for the 051900 stock remains attractive for patient investors.

- •Positives: Diversified business portfolio, powerful brand equity, stable financial structure, and clear investment in future growth engines.

- •Risks: Over-reliance on the Chinese market, intense competition in the beauty sector, and macroeconomic factors like interest rates and currency fluctuations.

Investors should monitor LG H&H’s H2 2025 earnings reports and management’s progress on their growth strategies. Decisions should be based on fundamental performance rather than a single institutional portfolio adjustment.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.