The latest BCnC Q3 2025 earnings report, released November 7, 2025, has sent a mixed but intriguing signal to the market. As a critical material supplier in the booming semiconductor industry, BCnC Co., Ltd. presented a financial puzzle: while revenue and operating profit missed analyst forecasts, net profit skyrocketed, creating what many are calling an ‘earnings surprise.’ This analysis will dissect the official figures, explore the hidden drivers behind this anomaly, and provide a comprehensive outlook for a potential BCnC investment strategy.

Is this a sign of underlying financial strength and clever management, or a one-off event masking deeper issues? Let’s dive into the data to understand BCnC’s true position in a dynamic global market.

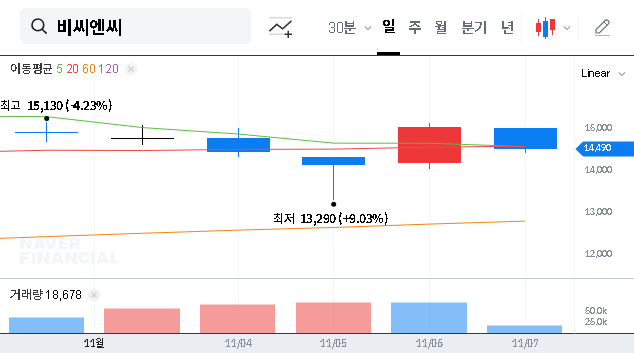

Unpacking the BCnC Q3 2025 Earnings Report

BCnC’s preliminary Q3 2025 results presented a clear deviation from market consensus. Here’s a breakdown of the performance against expectations:

- •Revenue: KRW 22 billion, falling 7% short of the KRW 23.6 billion forecast.

- •Operating Profit: KRW 1.4 billion, a 12.5% miss compared to the KRW 1.6 billion expectation.

- •Net Profit: KRW 1.7 billion, a staggering 183.3% surge above the KRW 0.6 billion forecast.

This discrepancy, particularly the massive outperformance in net profit, is the central theme of the current BCnC earnings analysis and requires a deeper investigation to determine its sustainability and impact on the BCnC stock.

The Core Mystery: Dissecting the Results

Headwinds for Revenue and Operating Profit

The shortfall in top-line revenue and operating profit can be attributed to a mix of industry-wide and company-specific factors. The global semiconductor market, while growing, faces periodic slowdowns in certain segments. Furthermore, BCnC’s H1 2025 report mentioned that its synthetic quartz manufacturing facility utilization was only at 50%. This underutilization can lead to lower production output and reduced economies of scale, putting pressure on operating margins. A slight dip from Q2’s operating profit of KRW 1.6 billion suggests that cost pressures or a shift in product mix may have impacted profitability.

The Source of the ‘Surprise’ Net Profit

The dramatic jump in net profit is almost certainly due to non-operating factors. These are financial events outside the company’s core business activities. Potential sources include:

- •Foreign Exchange Gains: Given BCnC’s 26.6% export ratio and the volatile KRW/USD exchange rate, significant currency fluctuations could have resulted in substantial financial gains.

- •Asset Sales: The one-time sale of property, equipment, or investment stakes can inject a large amount of cash, directly boosting net profit.

- •Tax Adjustments: A corporate tax refund or a significant change in deferred tax liabilities could have had a positive impact.

Investors must identify the precise cause to assess if this is a recurring benefit or a one-time windfall. The most reliable information can be found in the company’s official filing. You can review the Official Disclosure (DART Report) for a complete breakdown of non-operating income and expenses.

Understanding the source of the net profit surprise is the single most critical task for any investor evaluating the BCnC Q3 2025 earnings. A one-off event has very different implications for future value than a sustainable improvement in financial structure.

BCnC Investment Strategy: A Look at Fundamentals

Beyond the quarterly numbers, a sound BCnC investment strategy requires a look at the company’s underlying strengths and weaknesses. The outlook for semiconductor materials is robust, with organizations like SEMI projecting record industry growth. BCnC is positioned to capitalize on this through several key initiatives.

Strengths and Growth Catalysts

- •Technological Edge: Domestic production of synthetic quartz and expanded QD9+ supply give BCnC a competitive advantage.

- •Portfolio Diversification: The development of new materials like CD9 and Si ingots for next-generation chips signals a commitment to innovation.

- •Global Reach: Expansion into overseas markets with major clients diversifies revenue streams away from domestic dependence. For more context, see our guide to investing in the semiconductor sector.

Risks and Investor Concerns

However, investors should remain cautious of several red flags. The high debt-to-equity ratio of 128.48% indicates significant financial leverage, which can be risky in a high-interest-rate environment. Additionally, the issuance of convertible bonds introduces the potential for share dilution, which could negatively impact the BCnC stock price in the future.

Conclusion: A Prudent Path Forward

BCnC’s Q3 2025 earnings report is a classic case of needing to look beyond the headlines. While the net profit figure is impressive, the weakness in core operations requires careful consideration. For long-term investors, the focus should be on the company’s technological roadmap and its ability to improve operational efficiency.

Before making any investment decisions, investors should:

- •Verify the Net Profit Source: Analyze the official disclosures to confirm the reason for the net profit surge.

- •Monitor Q4 Guidance: Pay close attention to the company’s outlook for the next quarter and full-year 2026 to gauge recovery momentum.

- •Track Key Projects: Watch for progress on new material commercialization and improvements in facility utilization rates.

Ultimately, BCnC presents a compelling long-term growth story marred by short-term uncertainty. A cautious, research-driven approach is the most prudent strategy.