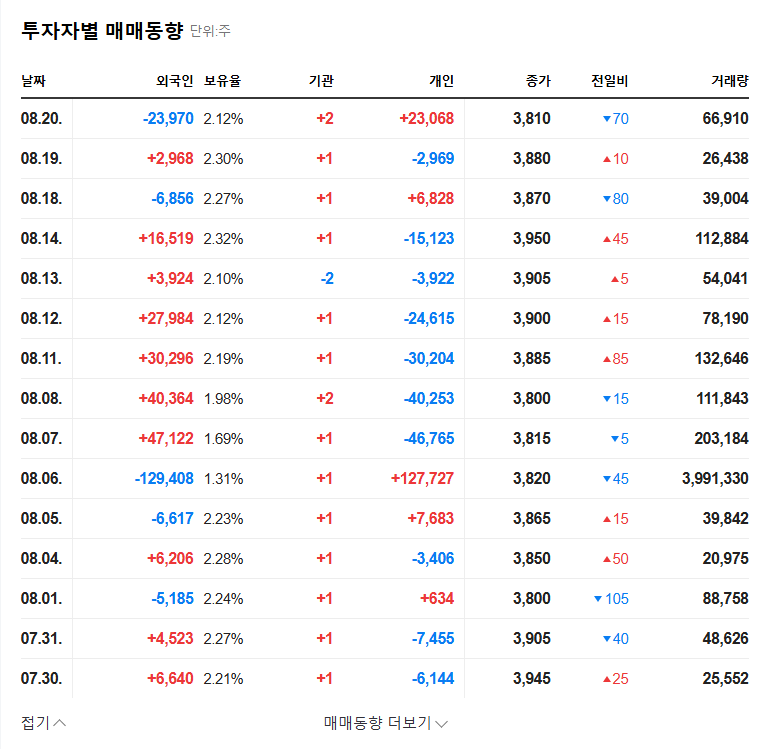

EcoBio Holdings Co., Ltd. stands at a critical crossroads. The company recently unveiled a significant EcoBio Holdings hydrogen investment, committing a substantial 6.5 billion KRW to expand its footprint in the green energy sector. This bold strategic pivot aims to capture a share of the burgeoning hydrogen economy, promising a new era of growth. However, this ambitious move comes as the company grapples with deteriorating financial health, creating a classic high-risk, high-reward scenario for investors. Is this a visionary leap into the future or a financial gamble that could strain the company to its breaking point? This in-depth analysis will dissect the investment, evaluate the underlying financials, and provide a clear roadmap for stakeholders.

The Landmark Investment: What is the KRW 6.5 Billion For?

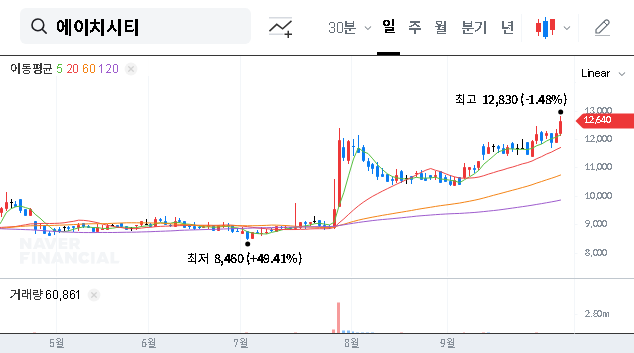

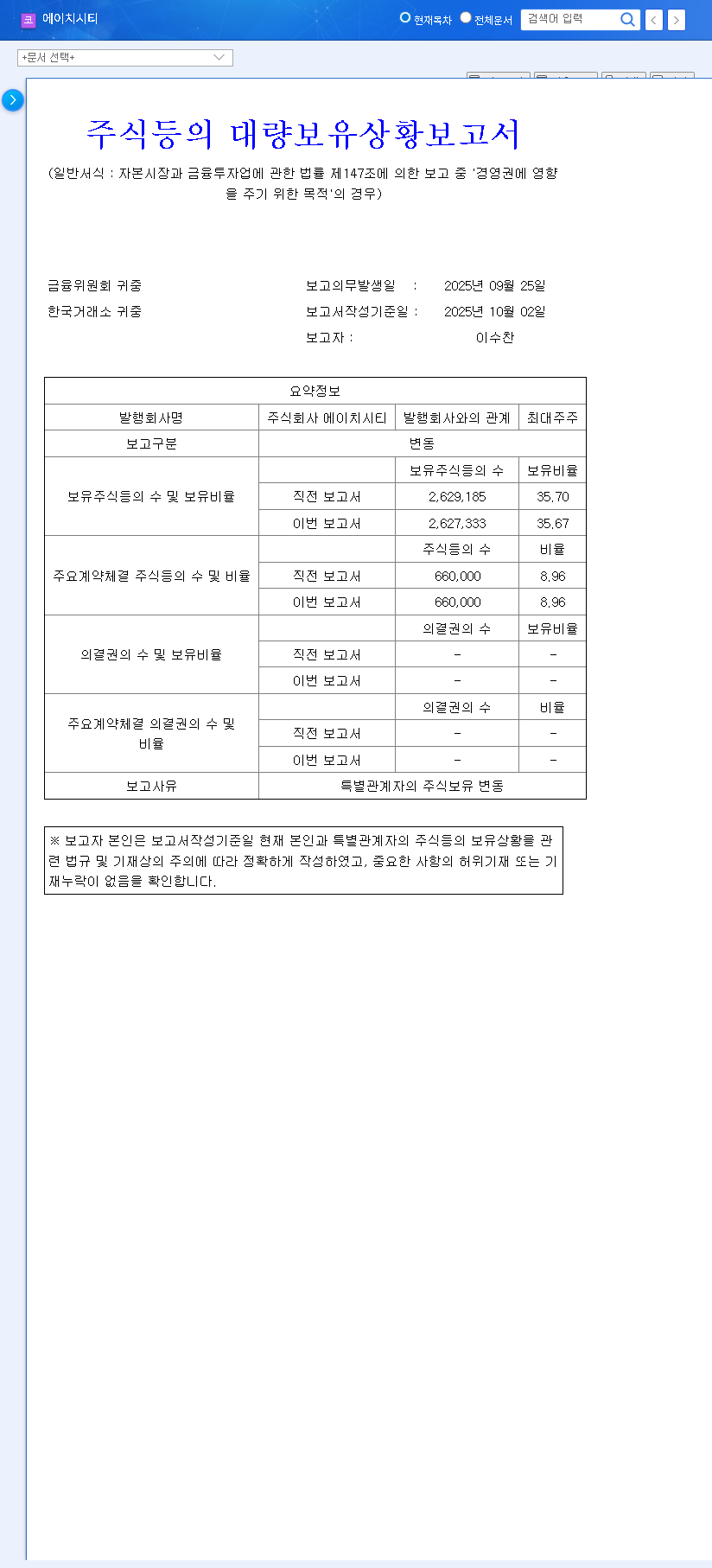

On November 11, 2025, EcoBio Holdings formally announced its plan to inject 6.5 billion KRW into new hydrogen business facilities. This figure, representing over 8% of the company’s total equity, is a clear signal of intent. The investment, detailed in the company’s Official Disclosure on DART, is scheduled over approximately 1.1 years. The capital is expected to fund the development of advanced hydrogen production and storage infrastructure, positioning the company to meet future demand. While the specifics of the technology are proprietary, the goal is to establish a competitive advantage in a market that is rapidly gaining global momentum.

A Company Under Pressure: The Financial Reality

The timing of this major capital expenditure is what raises significant concerns. A close look at the EcoBio financial health reveals a company facing considerable headwinds. The decision to invest heavily now, while potentially strategic, adds a layer of risk that cannot be ignored.

Alarming Liquidity and Debt Metrics

The company’s ability to meet its short-term obligations is under scrutiny. Key indicators paint a worrying picture:

- •Plummeting Current Ratio: A dramatic fall from a healthy 153.78% in 2023 to a precarious 35.64% in 2024 suggests a severe weakening of short-term liquidity. This means the company has far fewer current assets to cover its current liabilities.

- •Rising Debt-to-Equity: This ratio climbed from 27.24% to 46.00% over the last year. While the longer-term trend shows a slight decrease, the current level remains high, indicating a reliance on debt financing that this new investment will only exacerbate.

Plummeting Profitability and Asset Quality

It’s not just the balance sheet that’s flashing warning signs. Profitability has also been on a steady decline. The operating profit margin shrank from 16.21% in 2022 to just 4.87% in 2024, while Return on Equity (ROE) collapsed from 16.03% to 3.37% in the same period. Compounding these issues, both consolidated and separate financial statements reported a net loss in 2024, eroding total equity. An increase in the allowance for doubtful accounts also hints at potential issues with asset quality and loan collections.

For EcoBio Holdings, this hydrogen investment is the ultimate double-edged sword: it represents a potential lifeline to future relevance and profitability, but its immediate financial burden could sink the ship before it reaches the promised land.

The Two Sides of the Coin: Pros vs. Cons

The Bull Case: Future Growth and Diversification

Despite the financial risks, the strategic rationale for the hydrogen business investment is compelling. Globally, governments are promoting hydrogen as a key component of decarbonization, creating powerful tailwinds. According to reports from institutions like the International Energy Agency, the hydrogen market is poised for exponential growth. By investing now, EcoBio could secure a crucial first-mover advantage. This move also serves to diversify its business portfolio, reducing dependence on its currently struggling core operations and creating new, potentially more stable revenue streams for the long term.

The Bear Case: Financial Burden and Execution Risk

The primary risk is clear: the company is making a large, speculative bet from a position of financial weakness. The KRW 6.5 billion investment will place immense pressure on short-term cash flow and further strain the balance sheet. Furthermore, the hydrogen industry is capital-intensive and fraught with technological hurdles and intense competition. There is no guarantee of success, and a return on investment could be many years away. If the core business continues to underperform, it may lack the financial stability to see this ambitious project through to completion. Investors should also review our guide to analyzing high-risk growth stocks for more context.

Investor’s Strategic Checklist

For those conducting an EcoBio Holdings stock analysis, a cautious and vigilant approach is paramount. The long-term stock price will hinge on the successful execution of this hydrogen strategy. Key areas to monitor include:

- •Funding Transparency: How will the 6.5 billion KRW be financed? Will it be through debt, equity, or a mix? Analyze the impact of the chosen method on financial health.

- •Project Milestones: Track the progress of the hydrogen facility construction and operations. Are they hitting their targets on time and on budget?

- •Core Business Performance: Look for signs of a turnaround in the existing business. A stabilization here would provide a much-needed financial cushion for the new venture.

- •Industry & Policy Landscape: Keep an eye on government policies, subsidies for the hydrogen sector, and the competitive environment.

In conclusion, the EcoBio Holdings hydrogen investment is a defining moment for the company. While the short-term market reaction may be negative due to the clear financial risks, the long-term potential could be transformative if management executes flawlessly. Prudent financial risk management must be the top priority to ensure this growth engine doesn’t become a financial anchor.