The latest HYUNDAI G.F. HOLDINGS Q3 2025 earnings report has sent a complex signal to the market. While top-line figures like revenue and operating profit narrowly missed analyst consensus, the company delivered a stunning 46% ‘earnings surprise’ in net profit attributable to controlling interests. This divergence creates a critical question for investors: Is this a sign of underlying strength and clever financial management, or a one-time event masking core operational challenges? This comprehensive analysis will dissect the Q3 performance, explore the long-term financial trends, and provide a clear framework for your HYUNDAI G.F. HOLDINGS investment strategy.

Breaking Down the Q3 2025 Earnings Report

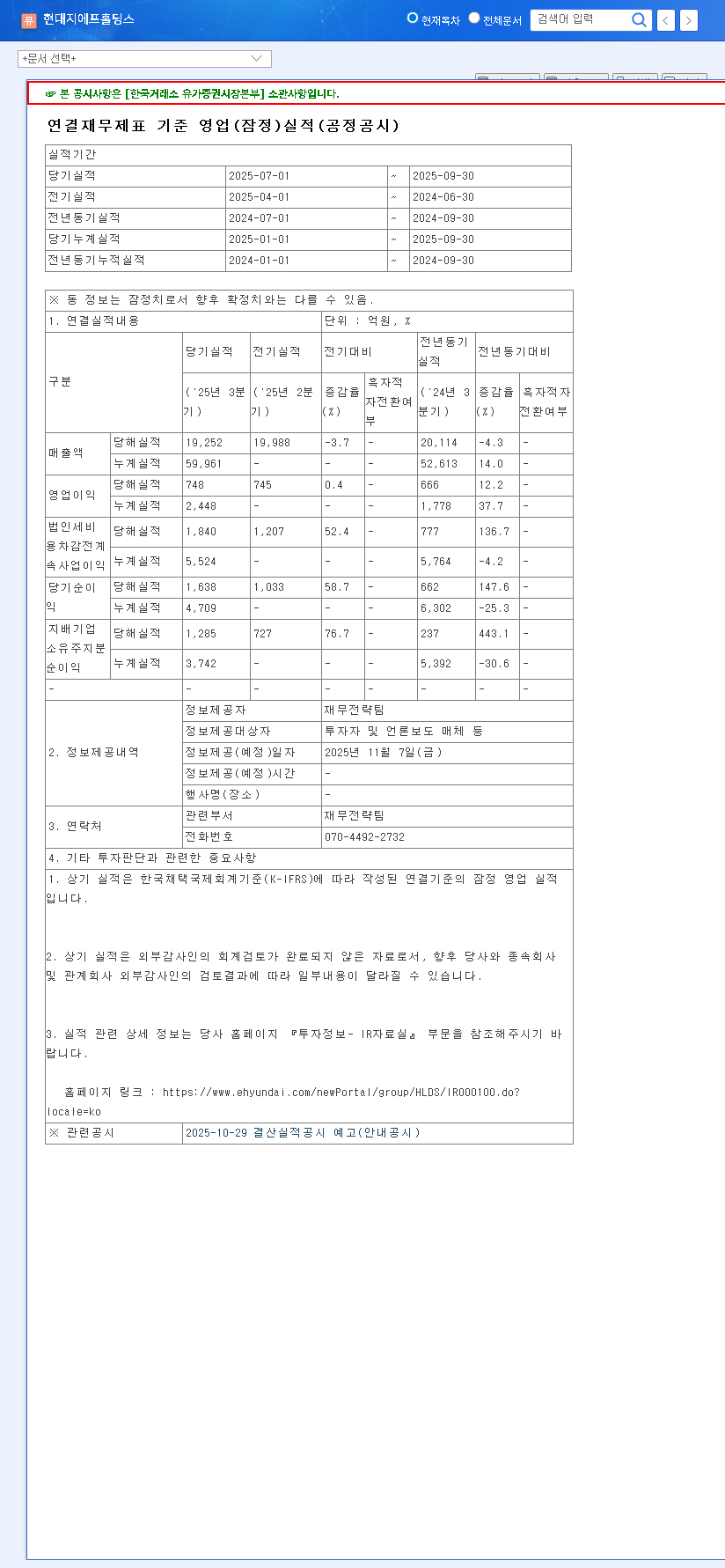

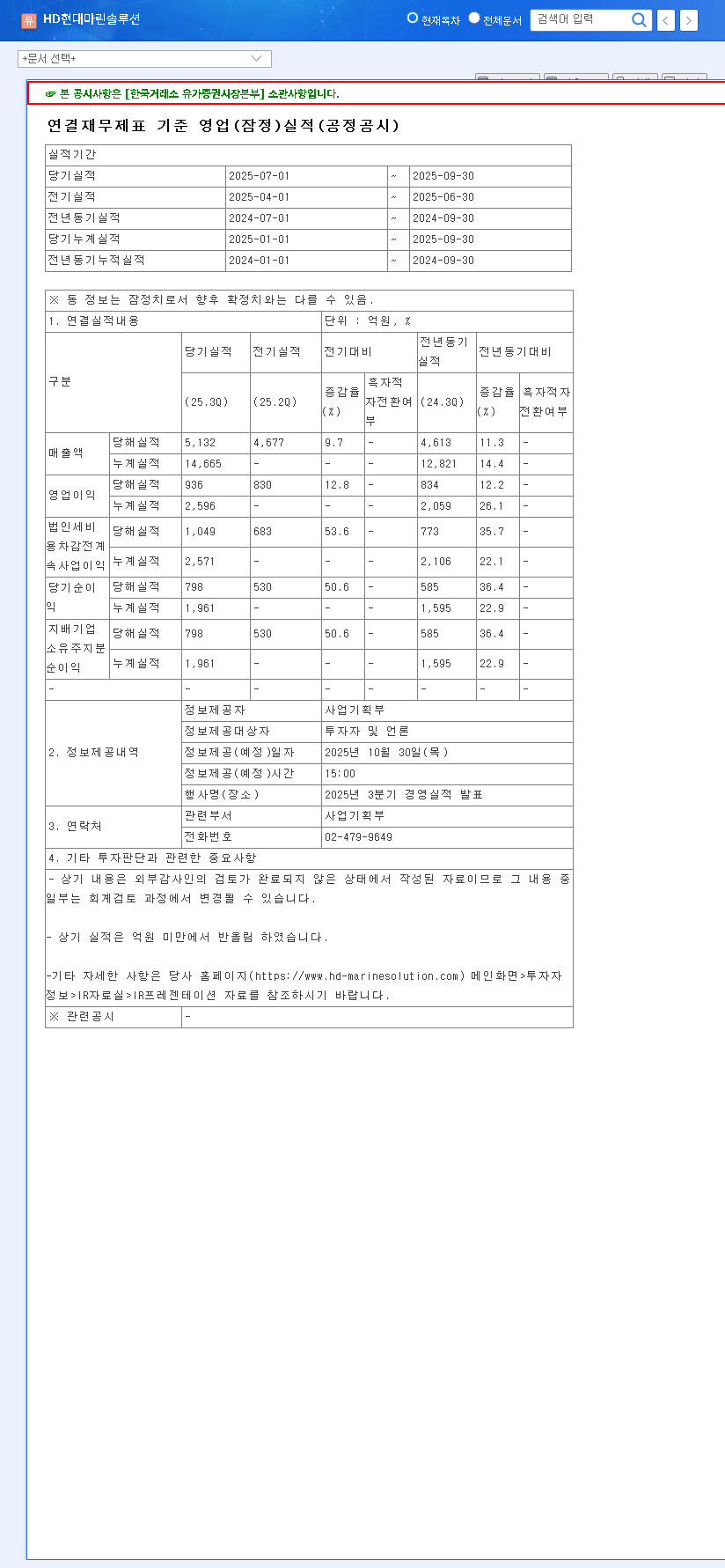

On November 7, 2025, HYUNDAI G.F. HOLDINGS released its provisional consolidated results, revealing a mixed performance against market expectations. The headline numbers present a narrative of slight operational underperformance overshadowed by exceptional bottom-line results.

- •Revenue: KRW 1.9252 trillion, missing the expected KRW 2.0150 trillion by 4%.

- •Operating Profit: KRW 74.8 billion, just 1% below the consensus of KRW 75.4 billion.

- •Net Profit (Controlling Interests): KRW 128.5 billion, a massive 46% above the market’s expectation of KRW 88.1 billion.

These figures are derived from the company’s provisional announcement. For a complete breakdown, investors should consult the Official Disclosure (Source: DART).

The Core Story: Unpacking the Net Profit Surprise

The pivotal element of the HYUNDAI G.F. HOLDINGS Q3 2025 earnings is the significant gap between operating profit and net profit. While operating profit reflects the core business’s profitability, net profit includes all financial activities. The substantial outperformance suggests strong contributions from non-operating areas.

The 46% net profit beat was likely driven by non-operating factors, such as gains from equity method investments in affiliates, favorable currency exchange movements, gains on asset sales, or other one-time financial income. This is a crucial distinction for assessing the sustainability of the company’s earnings power.

Long-Term Financial Performance Trends

Examining the company’s trajectory over the last few years reveals several key trends essential for a complete HYUNDAI G.F. HOLDINGS stock analysis. The annual revenue growth from 2022 to 2024 shows long-term momentum, but the quarterly revenue decline in 2025 is a new headwind that requires monitoring. Meanwhile, profitability metrics like Return on Equity (ROE) have been volatile, declining sharply before showing signs of a potential recovery in 2025 estimates.

- •Profitability Concern: Operating profit has stagnated, and net profit showed losses in 2023 and 2024, highlighting the importance of the recent Q3 rebound.

- •Rising Leverage: The debt-to-equity ratio has climbed from 69.9% in 2022 to 84.85% in 2024, indicating increased financial risk that needs careful management.

- •Valuation Check: The estimated 2025 Price-to-Earnings (PER) ratio of 52.07x, while an improvement, is still high, suggesting the market has already priced in significant future growth. For more on valuation metrics, see this guide from Investopedia.

Market Reaction and Strategic Outlook for Investors

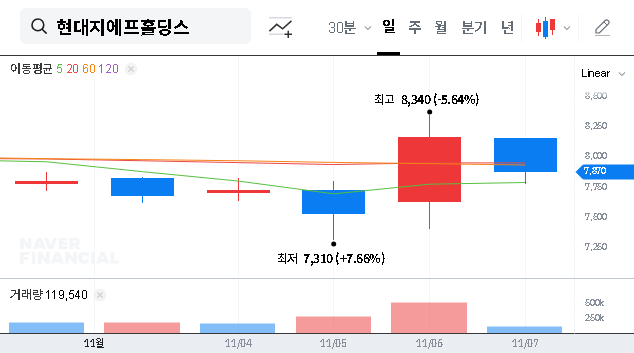

The stock price of HYUNDAI G.F. HOLDINGS has already seen a remarkable surge in 2025, climbing to KRW 8,048 by the earnings release date. This indicates that the market had anticipated a positive turn, likely based on the 2024 performance and the broader economic outlook. Given this context, the Q3 report is expected to have a neutral short-term impact. The positive net profit surprise may balance out the concerns from the softer revenue figures.

Key Strengths (The Bull Case)

- •Bottom-Line Resilience: The ability to generate significant net profit demonstrates financial flexibility and potential value from its holdings.

- •Anticipated 2025 Recovery: Projections for a significantly improved EPS in 2025 suggest a strong turnaround is underway.

- •Long-Term Growth: Historical revenue growth provides a solid foundation if the recent quarterly decline can be reversed.

Potential Risks (The Bear Case)

- •Core Business Slowdown: The three-quarter revenue decline is a major red flag that needs to be addressed in the company’s next strategic update.

- •High Financial Leverage: The rising debt-to-equity ratio could become a burden in a high-interest-rate environment. You can explore our analysis of corporate debt strategies for more context.

- •High Valuation: With the stock price already elevated, there is little room for error. Any failure to meet future growth expectations could lead to a sharp correction.

In conclusion, a successful HYUNDAI G.F. HOLDINGS investment requires a nuanced view. Investors should look past the headline net profit number and demand clarity on the sustainability of earnings, a clear plan to reignite revenue growth, and prudent management of the company’s balance sheet. The upcoming full Q4 report and 2026 outlook will be critical in determining if the current optimism is justified.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.