Recent developments concerning Hyosung Heavy Industries (KRX: 298040) have presented a complex picture for investors. On one hand, an amended business report signals a welcome move towards greater corporate transparency. On the other, a notable share reduction by the National Pension Service (NPS) has raised questions. How should investors interpret these conflicting signals? This comprehensive analysis will explore the core issues, their impact on the company’s value, and provide a strategic roadmap for navigating the path ahead.

Decoding the Two Key Events

To understand the current investment climate for Hyosung Heavy Industries stock, we must first dissect the two pivotal events that have captured the market’s attention.

1. Amended Business Report: A Commitment to Transparency

Hyosung Heavy Industries recently filed an amendment to its business report, significantly expanding the details provided in its ‘Status of Single Sales/Supply Contract Execution’ section. This is more than just a procedural update; it’s a strong positive signal. The amendment now includes granular information such as contract names, counterparties, timelines, key terms, and specific financial figures. You can view the Official Disclosure on the DART system. This move directly addresses investor demand for clarity, enhancing trust and allowing for a more accurate assessment of the company’s revenue streams and operational health. For investors, learning how to analyze supply contracts is a crucial skill this report now supports.

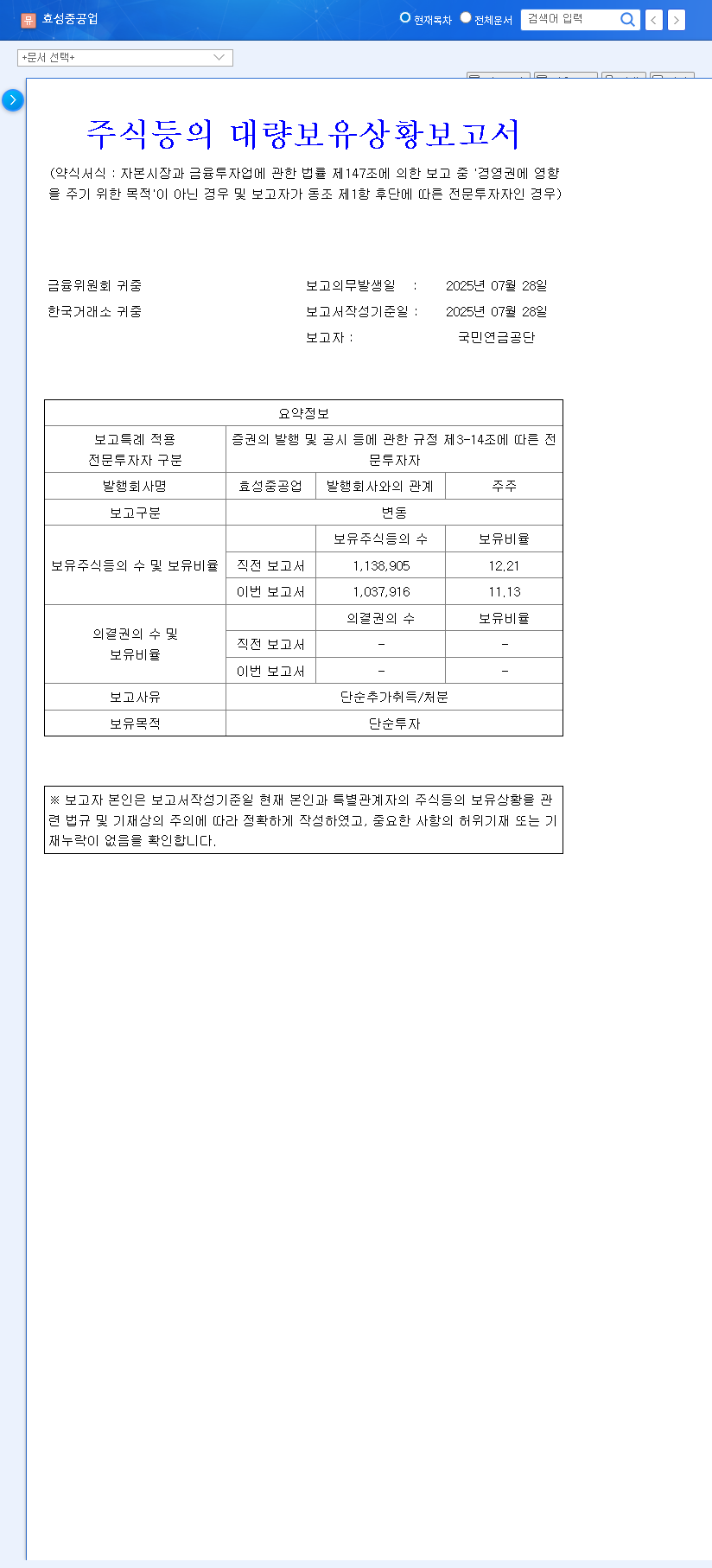

2. National Pension Service (NPS) Stake Reduction

Conversely, the National Pension Service (NPS) reported a decrease in its stake in Hyosung Heavy Industries, from 12.21% down to 11.13%. The stated purpose for the holding is ‘simple investment,’ and the change was due to ‘simple additional acquisition/disposal.’ While a share sale by a major institutional investor can create short-term selling pressure, the context is critical. This NPS divestment is likely part of a broader portfolio rebalancing strategy rather than a negative judgment on the company’s specific fundamentals. Large funds like the NPS regularly adjust their holdings across various sectors to manage risk and align with macroeconomic outlooks, a common practice in institutional investment strategy.

While increased transparency builds long-term trust, the NPS share reduction introduces short-term market uncertainty. Understanding the nuances of both is key for any investor in Hyosung Heavy Industries.

Impact on Fundamentals and Stock Outlook

The enhanced reporting is an unambiguous positive for the company’s fundamentals. It increases the visibility of future revenue, clarifies business risks, and boosts management credibility. In contrast, the NPS stake reduction primarily affects short-term market sentiment and supply-demand dynamics. While it could lead to temporary price volatility, its long-term impact on the intrinsic value of Hyosung Heavy Industries is expected to be limited, provided the company’s core business remains strong.

Macroeconomic Tailwinds for the Heavy Industries Segment

The broader market environment offers significant opportunities for Hyosung Heavy Industries’ core business. The global push for carbon neutrality and the explosive growth of AI and data centers are fueling unprecedented demand for electricity. This directly translates to a need for robust power infrastructure, including the transformers, circuit breakers, and power generation facilities that are central to the company’s portfolio. The expansion of global power grids represents a powerful, long-term growth driver that aligns perfectly with the company’s expertise.

A Strategic Investor’s Action Plan

Given these factors, a prudent investor should adopt a long-term perspective. The fundamental growth story in the heavy industries segment appears intact, while the move toward transparency strengthens the investment case. The NPS divestment should be viewed as short-term market noise rather than a fundamental red flag. Consider the following actions:

- •Focus on Core Business Health: Prioritize analysis of the heavy industries segment’s order book and profitability over short-term stock fluctuations.

- •Monitor Macro Trends: Keep a close eye on global energy investments, data center construction trends, and commodity prices, as these are key performance indicators for the company.

- •Assess Financial Soundness: Use the newly transparent data to evaluate the company’s cash flow, debt levels, and risk management in its more volatile construction segment.

- •Adopt a Long-Term Perspective: Base investment decisions on the company’s intrinsic value and long-term growth potential rather than reacting to headlines about institutional ownership changes.

Frequently Asked Questions (FAQ)

Q1: Why is the amended business report so important for Hyosung Heavy Industries investors?

The report provides unprecedented detail on specific contracts, allowing investors to more accurately forecast revenue, assess risk, and verify cash flow. This transparency reduces uncertainty and increases confidence in the company’s financial health and management.

Q2: Should I be concerned about the NPS reducing its stake?

While it can cause short-term price pressure, the fact that the NPS cited ‘simple investment’ purposes suggests it’s a portfolio management move, not a verdict on the company’s future. Its long-term impact on the value of Hyosung Heavy Industries stock is likely to be minimal.

Q3: What are the biggest growth drivers for Hyosung Heavy Industries?

The primary growth drivers are in the heavy industries segment. This includes rising global demand for power equipment (transformers, circuit breakers) driven by the renewable energy transition, grid modernization, and the power requirements of the rapidly growing AI and data center industries.