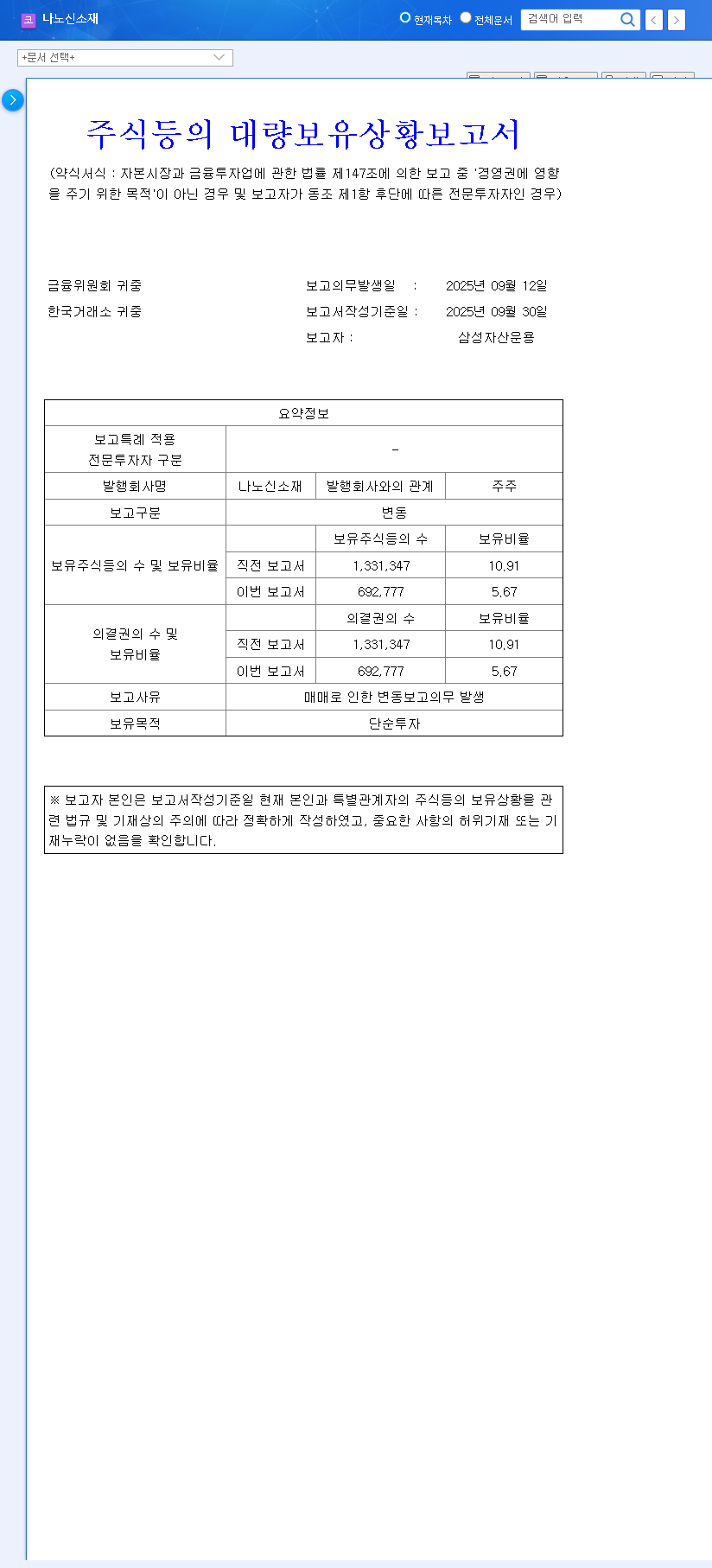

The recent performance of NanoSintech stock (Ticker: 121955680256) has sent ripples of concern through the investment community. A significant event has triggered this uncertainty: the news that Samsung Asset Management, one of Korea’s premier institutional investors, has drastically cut its holdings in the company. With their stake falling from 10.91% to 5.67%, investors are left grappling with critical questions about the future of their NanoSintech investment.

Is this a strategic pivot by an asset manager, or does it point to underlying weaknesses within NanoSintech? This comprehensive analysis will explore the implications of this sale, dissect the company’s latest financial reports, and consider the broader market forces at play to provide a clear outlook on NanoSintech stock.

The Catalyst: Samsung Asset Management’s Share Sale

On October 2, 2025, a significant filing revealed that Samsung Asset Management had reduced its stake in NanoSintech by 5.24 percentage points, a move that liquidated shares worth approximately 31.6 billion KRW. The specifics of this transaction, available in the Official Disclosure, confirm the scale of the sale. Such a large-scale divestment by a major institution is often a bearish signal, typically leading to increased selling pressure and a contraction in investor sentiment.

The key takeaway for investors is that a large institutional exit, regardless of the reason, can create significant short-term volatility. The market often reacts first and asks questions later.

While Samsung Asset Management cited ‘Simple Investment’ as its purpose for holding the shares, suggesting the sale could be for portfolio rebalancing or profit-taking, the timing warrants a deeper look into NanoSintech’s underlying health.

Fundamentals Under the Microscope: A Look Inside NanoSintech

To understand if this sale is a red flag, we must analyze NanoSintech’s recent performance. The 2025 semi-annual report paints a picture of a company facing significant headwinds, even as it positions itself for future growth.

Evaluating the Concerning NanoSintech Stock Financials

- •Revenue Decline: While headline figures showed an 18.7% year-on-year increase due to accounting changes, the actual half-year revenue (Jan-Jun) plummeted by a startling 41.1% compared to the previous year.

- •Profitability Issues: The company reported an operating profit of just 2.139 billion KRW (a 9.8% decrease) and swung to a net loss of -1.193 billion KRW, primarily due to rising administrative expenses.

- •Broad-Based Weakness: Revenue fell across all major business segments: Secondary Batteries (-24.7%), Displays (-52.4%), Semiconductors (-50.1%), and Solar Cells (-56.2%).

This widespread downturn suggests that the company’s challenges are not isolated to one division but are systemic, likely stemming from increased competition and shifting market dynamics. For a deeper understanding of market trends, investors can consult authoritative sources like Bloomberg’s industry analysis.

Balancing Risk and Reward: Future Outlook

Despite the grim short-term picture, NanoSintech is not without a long-term strategy. The company is making moves to shore up its finances and pivot towards high-growth areas. The critical question for any NanoSintech stock analysis is whether these future prospects can outweigh the current struggles.

Mid-to-Long Term Growth Drivers

- •Global Expansion: New subsidiaries and production facilities in the US and Poland are poised to tap into the growing EV and renewable energy markets in North America and Europe.

- •Strategic Fundraising: The issuance of 95 billion KRW in convertible bonds and 100 billion KRW in bonds with warrants is a clear effort to secure capital for these growth initiatives and improve financial stability.

- •High-Tech Potential: NanoSintech retains technological expertise in advanced materials for semiconductors and solar cells, two sectors with strong long-term tailwinds.

Investor Action Plan: Navigating the Uncertainty

Given the conflicting signals, a prudent investment strategy is essential. The Samsung sale has undoubtedly increased the risk profile for NanoSintech stock in the short term. Investors should consider the following steps:

- •Exercise Short-Term Caution: The overhang from the institutional sale could keep the stock price suppressed or volatile for the next few quarters. A wait-and-see approach may be wise.

- •Monitor Fundamental Recovery: Pay close attention to the next two quarterly earnings reports. Look for signs of a turnaround in the core secondary battery segment and stabilization in other divisions.

- •Track Growth Milestones: Watch for announcements related to the US and Poland facilities becoming operational and securing new contracts. Concrete progress is needed to validate the growth story. For more on evaluating growth stocks, you can read our guide on analyzing tech company fundamentals.

- •Assess Macro Environment: Keep an eye on factors like interest rates and raw material costs, which can significantly impact NanoSintech’s profitability and investment sentiment.

In conclusion, while Samsung Asset Management’s sale is a significant negative signal that reflects NanoSintech’s current operational struggles, it may not be a definitive judgment on its long-term corporate value. The coming months will be critical in determining whether the company can execute its turnaround strategy and transform its growth potential into tangible results.