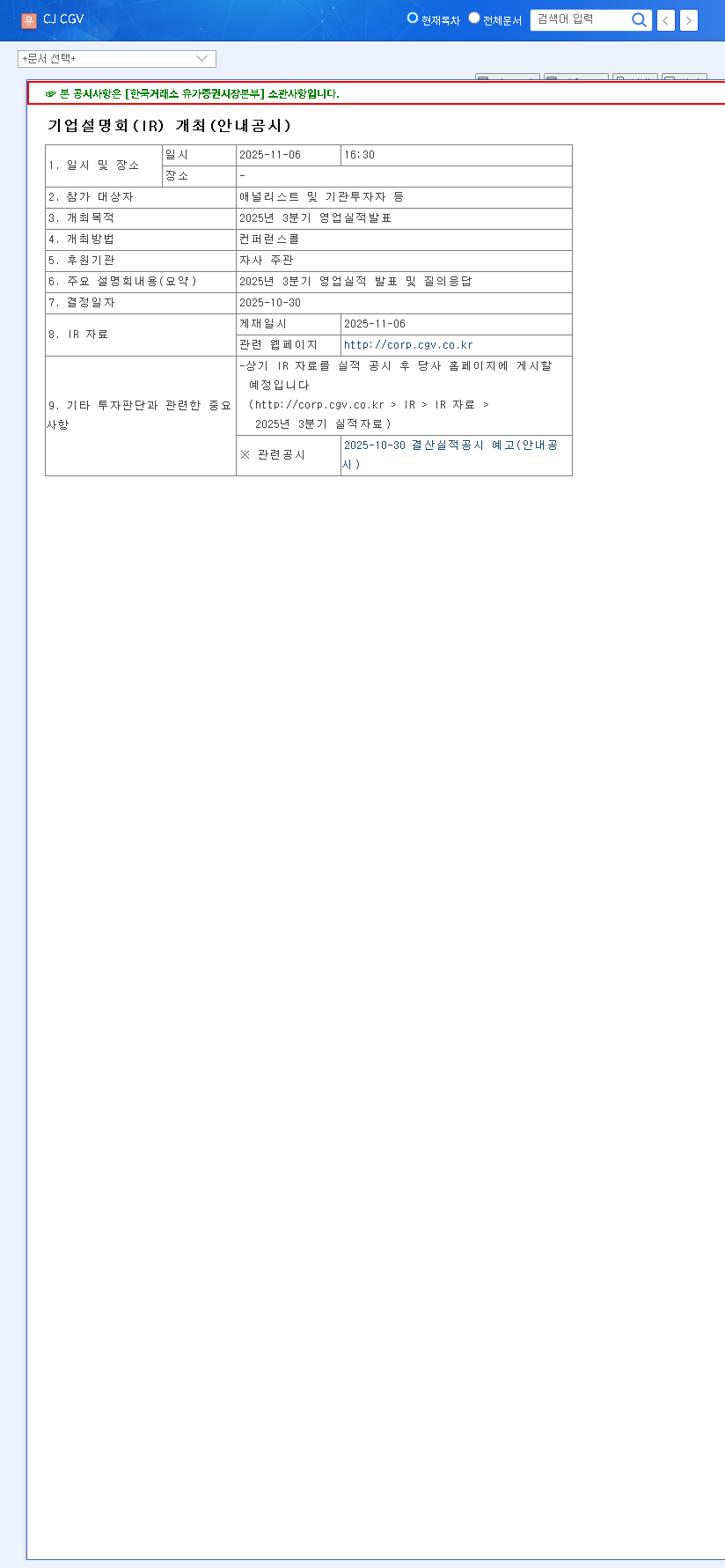

The upcoming CJ CGV Q3 Earnings conference call for 2025 is more than just a financial update; it’s a pivotal moment that could define the company’s trajectory. For investors, it’s like the third act of a tense blockbuster film, where the protagonist faces their greatest challenges. With a backdrop of high debt and a struggling core business, the market is anxiously waiting to see if CJ CGV can unveil a strategy for a triumphant comeback or if the credits will roll on its recent stock stability.

This comprehensive report offers a detailed CJ CGV stock analysis, dissecting the company’s fundamentals, the macroeconomic pressures, and the potential outcomes of the investor relations (IR) event. We will illuminate the key performance indicators to watch and provide a clear roadmap for navigating this critical investment juncture.

Unpacking the CJ CGV Q3 Earnings Report: What Investors Need to Know

The Q3 2025 IR event is a platform for CJ CGV to address its current financial predicament and present a compelling vision for the future. The stakes are incredibly high, as the company grapples with internal weaknesses and external market volatility.

A Look at the Financials (H1 2025 Data)

CJ CGV’s recent financial health paints a concerning picture. While the consolidation of its IT division (CJ OliveNetworks) boosted consolidated revenue to KRW 1.025 trillion, a 24.6% year-over-year increase, the bottom line tells a different story. For more detailed data, see the official disclosure (Source: DART report).

- •Plummeting Profitability: Operating profit fell a staggering 81.8% to just KRW 4.918 billion, dragged down by a KRW 16.871 billion operating loss in the core multiplex segment.

- •Net Loss: The company reported a significant net loss of KRW 76.304 billion, a sharp reversal into deficit.

- •Precarious Debt: The consolidated debt-to-equity ratio stands at an alarmingly high 622%, with short-term borrowings and convertible bonds adding immense financial pressure.

The central question for every investor is: Can CJ CGV’s strategic initiatives, like its special format theaters and IT services, generate enough cash flow to service its massive debt and offset the persistent weakness in its traditional cinema operations? The Q3 earnings call must provide a convincing answer.

Segment Performance: Bright Spots and Shadows

The company’s performance is a tale of two businesses. The multiplex operations, the historical core of CJ CGV, are facing significant multiplex industry challenges. A drought of domestic and international blockbuster films has led to declining attendance, a trend seen across the global cinema market. However, there are potential growth engines:

- •Growth Drivers: Differentiated formats like 4DX and SCREEN X remain competitive advantages. The company is also wisely diversifying into global IP content distribution and alternative programming (like concert screenings), which could open new revenue streams.

- •Persistent Risks: The IT services segment, while growing the top line, cannot single-handedly rescue profitability. High interest rates, fierce competition, and currency volatility remain major threats to any recovery.

Scenarios for the Stock: A Post-IR Analysis

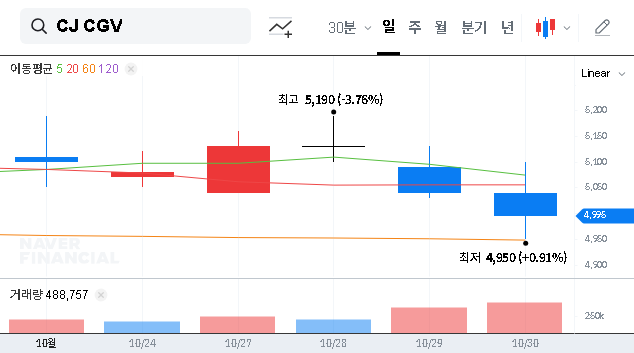

The outcome of the Q3 earnings call will likely trigger a decisive move in CJ CGV’s stock price, which has been hovering in the KRW 5,500-6,000 range. Here are two potential scenarios based on the information revealed.

The Bull Case (Positive Impact)

A positive market reaction could be fueled by announcements of a clear earnings beat, especially a marked improvement in multiplex attendance and sales. If management presents a concrete, credible plan for debt reduction and showcases strong forward momentum in its high-margin special format theaters, the stock could break above the KRW 6,000 resistance level. As leading market analysts at Bloomberg often note, a clear deleveraging strategy is paramount for investor confidence.

The Bear Case (Negative Impact)

Conversely, if the Q3 results miss expectations or if the multiplex segment continues its decline, investor sentiment will sour. Vague answers on financial restructuring or a lack of a clear growth strategy during the Q&A session could be disastrous, potentially sending the stock price below the KRW 5,500 support level. Any sign of further financial strain could trigger a significant sell-off.

Investor Checklist: Key Questions for the Call

For any serious CJ CGV investment, listening to the Q3 earnings call is essential. Pay close attention to management’s commentary on these four critical areas:

- •Multiplex Turnaround: Are attendance, Average Ticket Price (ATP), and concession sales showing signs of life?

- •Financial Health Plan: What are the specific, actionable steps to manage the 622% debt-to-equity ratio?

- •Growth Engine Performance: How is the IT segment’s profitability? What is the expansion strategy for 4DX and SCREEN X?

- •Content Strategy: What is the outlook for the film pipeline and the global IP business?

Ultimately, the CJ CGV Q3 Earnings call will be a moment of truth. Investors should listen carefully, analyze the data beyond the headlines, and prepare to act based on the credibility and substance of the company’s strategic vision.