This comprehensive HANLA IMS investment analysis delves into the company’s powerful H1 2025 performance and the game-changing Memorandum of Understanding (MOU) to acquire assets from Daesun Shipbuilding. In a rapidly evolving shipbuilding industry, understanding both a company’s robust fundamentals and its ambitious growth drivers is critical for any savvy investor. We will dissect how this major expansion plan, built on a foundation of solid earnings, could redefine HANLA IMS’s corporate value and shape future investment decisions.

Going beyond a simple earnings report, this article explores the potential synergies, latent risks, and long-term strategic implications of the acquisition. We provide the essential information needed to forecast the future of HANLA IMS stock and its position within the competitive maritime sector.

Stellar H1 2025 Performance: A Foundation for Growth

HANLA IMS delivered a truly impressive financial performance in the first half of 2025, establishing a powerful financial springboard for its strategic expansion plans. These results demonstrate strong operational efficiency and a healthy demand for its core products.

Key Financial Highlights (YoY Growth)

- •Revenue: Reached KRW 62.218 billion, a remarkable 27.8% increase.

- •Operating Profit: Surged to KRW 11.289 billion, a 43.3% increase.

- •Net Income: Climbed to KRW 12.191 billion, an outstanding 54.9% increase.

Analysis of Core Strengths

The engine behind this growth was the company’s core businesses in shipbuilding equipment and industrial plants. Integrated control and monitoring systems were significant contributors, showcasing the company’s technological edge. Furthermore, the company’s financial health has been substantially fortified. Cash and cash equivalents saw a significant rise, and the debt-to-equity ratio improved to a very stable 19.44%. This fiscal discipline provides HANLA IMS with the flexibility and capital to pursue ambitious projects like the Daesun Shipbuilding asset acquisition without over-leveraging.

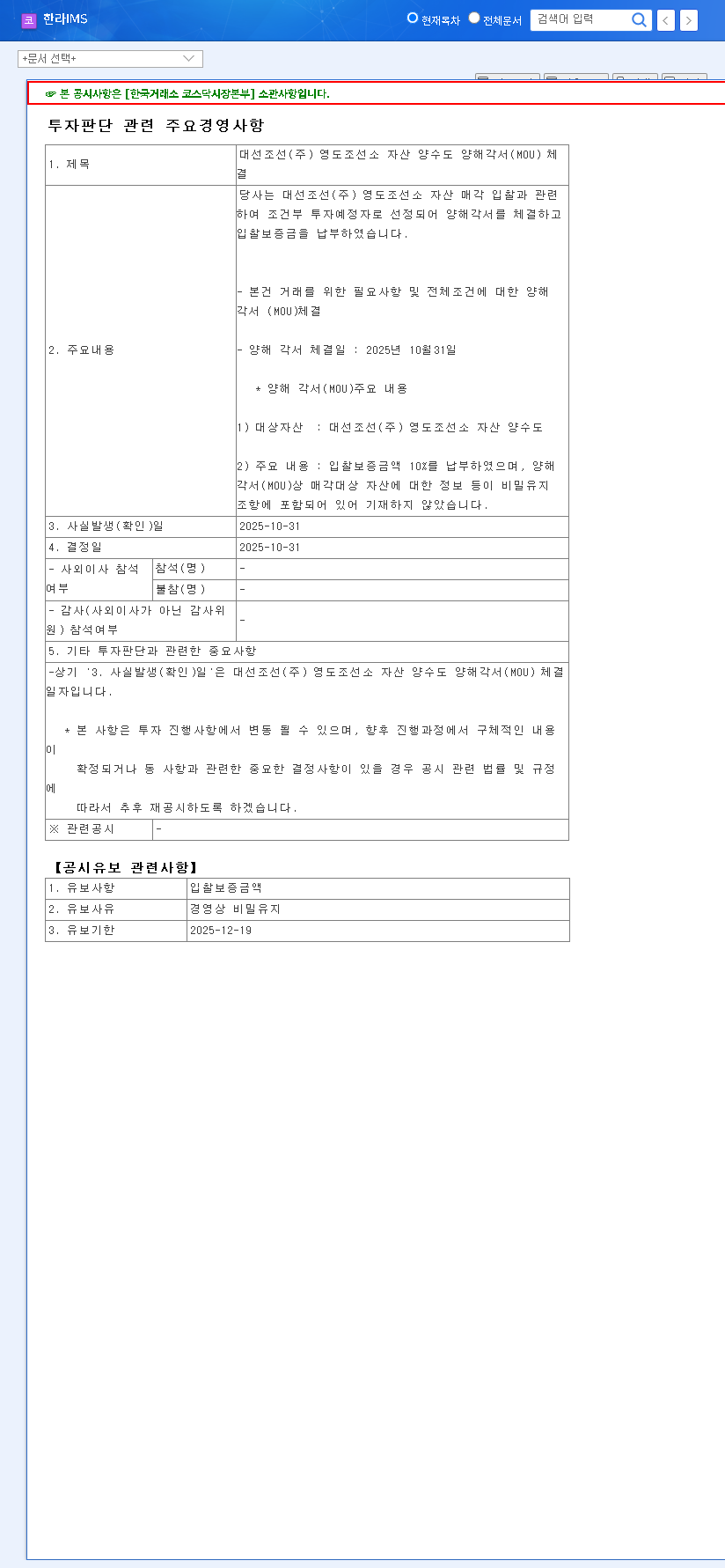

The Daesun Shipbuilding MOU: A New Horizon for HANLA IMS

The landmark MOU for the acquisition of Daesun Shipbuilding’s Yeongdo Shipyard assets represents a pivotal moment for HANLA IMS. On October 31, 2025, the company was selected as the conditional preferred bidder, a move that signals a bold step towards business expansion and portfolio diversification. For more details, see the Official Disclosure on DART.

This isn’t just an acquisition; it’s a strategic transformation. By securing shipyard assets, HANLA IMS is evolving from a leading equipment supplier to a more integrated player in the shipbuilding industry, unlocking significant vertical synergies.

Strategic Benefits and Synergies

- •Expanded Production Capacity: Acquiring the Yeongdo Shipyard grants HANLA IMS the physical infrastructure to dramatically scale its operations and enter new segments like steel shipbuilding and potentially large offshore wind substructures.

- •Portfolio Diversification: This move reduces reliance on the equipment sector, creating a more resilient business model that can better withstand cyclical downturns in specific parts of the shipbuilding industry.

- •Enhanced Competitiveness: The integration of production facilities is expected to streamline supply chains, reduce costs, and improve profitability through powerful synergies in technology, production, and sales networks.

Calculated Risks and Considerations

While the outlook is positive, investors must remain aware of the inherent risks. The MOU is a preliminary step, and the final terms of the contract could change. The large-scale acquisition will require significant capital, and while HANLA IMS’s financial position is robust, the impact on its balance sheet must be monitored. Finally, the post-acquisition integration of Daesun Shipbuilding’s assets and workforce will present managerial challenges that require flawless execution to realize the projected synergies. For more on industry trends, you can read about the global shipbuilding market outlook.

Investment Thesis: A ‘Buy’ Rating with Vigilance

Our overall assessment of the HANLA IMS investment case is highly positive. The company’s strong fundamentals, demonstrated by its H1 2025 results, provide a stable base for the significant long-term growth potential offered by the Daesun Shipbuilding deal. While short-term uncertainties exist, the strategic rationale for the acquisition is compelling and promises to substantially enhance long-term corporate value.

Therefore, we maintain a ‘Buy’ rating for HANLA IMS stock. However, prudent investors should closely monitor the following developments before making a final decision:

- •The successful negotiation and final terms of the asset transfer contract.

- •The specific financing plan for the acquisition and its real-time impact on the company’s financial structure.

- •Early indicators of successful business integration and synergy realization post-acquisition.

By keeping these factors in mind, investors can make well-informed decisions regarding their position in HANLA IMS. For further reading, check our analysis on the broader shipbuilding equipment market.