Investors examining SillaTextile stock are currently navigating a complex landscape. A recent ‘Report on Major Shareholdings’ has settled a period of management uncertainty, yet this positive development is cast against a backdrop of significant fundamental challenges. While the ownership structure has stabilized, deep-seated issues within the company’s core operations and financial health demand a cautious and thorough evaluation.

This comprehensive analysis provides a detailed look into the recent shareholding event, dissects SillaTextile’s business segments, and scrutinizes its deteriorating financial metrics. We aim to deliver an expert-level SillaTextile investment strategy to help you understand the company’s future value and make well-informed decisions about your portfolio.

The Shareholding Change: A Step Towards Stability?

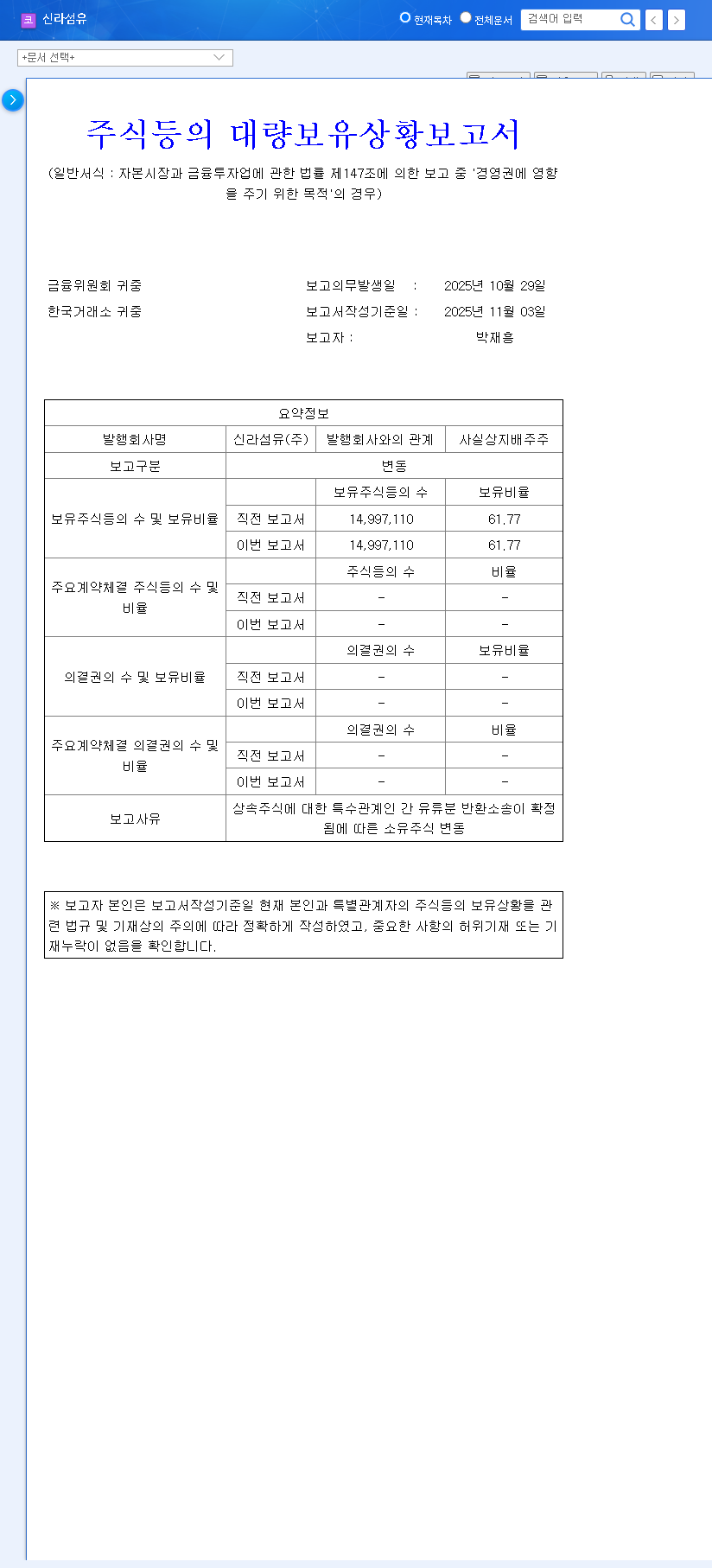

The primary catalyst for recent attention on SillaTextile stock was a mandatory disclosure filed by its largest shareholder, Park Jae-heung. This report detailed changes in share ownership among related parties following the conclusion of a clawback lawsuit related to inherited shares. You can view the Official Disclosure on DART for the complete filing.

Key Takeaways from the Report

While the internal share distribution shifted slightly, the most critical fact is that Park Jae-heung’s controlling stake remains firmly intact at 61.77%. The resolution of the family legal dispute eliminates a significant source of uncertainty. This allows the executive team to redirect their focus from internal legal battles to core business strategy, which is a net positive for management stability. However, this event has a limited direct impact on the SillaTextile stock price in the short term, as it does not alter the company’s underlying operational performance.

A Deep Dive into SillaTextile Stock Fundamentals

Beyond the boardroom, the company’s fundamentals present a tale of two vastly different businesses. Understanding this dichotomy is essential for any potential SillaTextile investment strategy.

The Ailing Mobile Division

The mobile phone sales division, a significant part of SillaTextile’s identity, is in a state of persistent decline. Performance in the first half of 2025 revealed a decrease in sales and a concerning shift to an operating loss. This isn’t a temporary dip; it’s a symptom of broader market forces, including intense competition, market saturation, and weakened consumer spending due to macroeconomic headwinds. A sharp increase in inventory levels further suggests that sales are sluggish and management is struggling to adapt to the changing market dynamics.

The Real Estate Leasing Lifeline

In stark contrast, the real estate leasing segment is the company’s bedrock of stability. This division now accounts for nearly 60% of total revenue and grew by an impressive 14.4% year-on-year. It functions as a reliable cash cow, providing predictable income that helps offset the losses from the mobile business. This stability is a crucial factor preventing a more severe downturn for the company.

The core challenge for SillaTextile stock is whether its stable, profitable real estate arm can indefinitely support a struggling mobile division and a strained balance sheet.

Financial Health Under Scrutiny

A comprehensive look at the company’s financial health reports reveals several red flags. Accumulated deficits have eroded total equity, while the debt ratio has climbed, increasing financial risk. Key profitability metrics like operating profit margin and Return on Equity (ROE) are disappointingly low. Furthermore, the market valuation appears stretched. With a Price-to-Earnings (P/E) ratio of 64.67x, the SillaTextile stock price seems significantly overvalued relative to its weak earnings power, a concern echoed by analysts at major outlets like Bloomberg.

Expert Investment Strategy: Underperform

Considering the struggling mobile segment, deteriorating financial health, and high valuation, our expert opinion on SillaTextile stock is ‘Underperform.’ We expect its performance to lag behind the broader market. The stability in management and real estate is not enough to warrant a bullish outlook at this time.

Recommendation for Investors

We recommend a cautious wait-and-see approach. New investments are not advised at the current price level. Existing shareholders should monitor the situation closely for signs of a fundamental turnaround. The investment appeal of SillaTextile stock hinges on tangible improvements, not just management stability.

Key Monitoring Points for the Future

- •Mobile Division Turnaround: Any concrete strategy to improve profitability or competitiveness.

- •Financial Structure Improvement: Actionable plans for debt reduction or capital increases.

- •New Growth Engines: Announcements of business diversification beyond the two current segments.

- •Real Estate Performance: Continued stability and growth in this crucial leasing business.

Investment decisions should always be made based on your own judgment and risk tolerance. This report serves as an analytical guide and is not a direct solicitation to buy or sell securities.