The upcoming SAMSUNG ELECTRO-MECHANICS Q3 2025 Earnings announcement, scheduled for October 29, 2025, is a pivotal event for investors. With a market capitalization exceeding KRW 14.9 trillion, the company’s financial results are a bellwether for the broader electronics component market. While robust revenue growth characterized the first half of 2025, a shadow of slowing profitability has created uncertainty. This comprehensive Samsung Electro-Mechanics analysis will unpack the key metrics, division-specific performance, and strategic outlook that will determine the trajectory of SAMSUNG ELECTRO-MECHANICS stock post-announcement.

The Main Event: Q3 2025 Investor Relations Conference

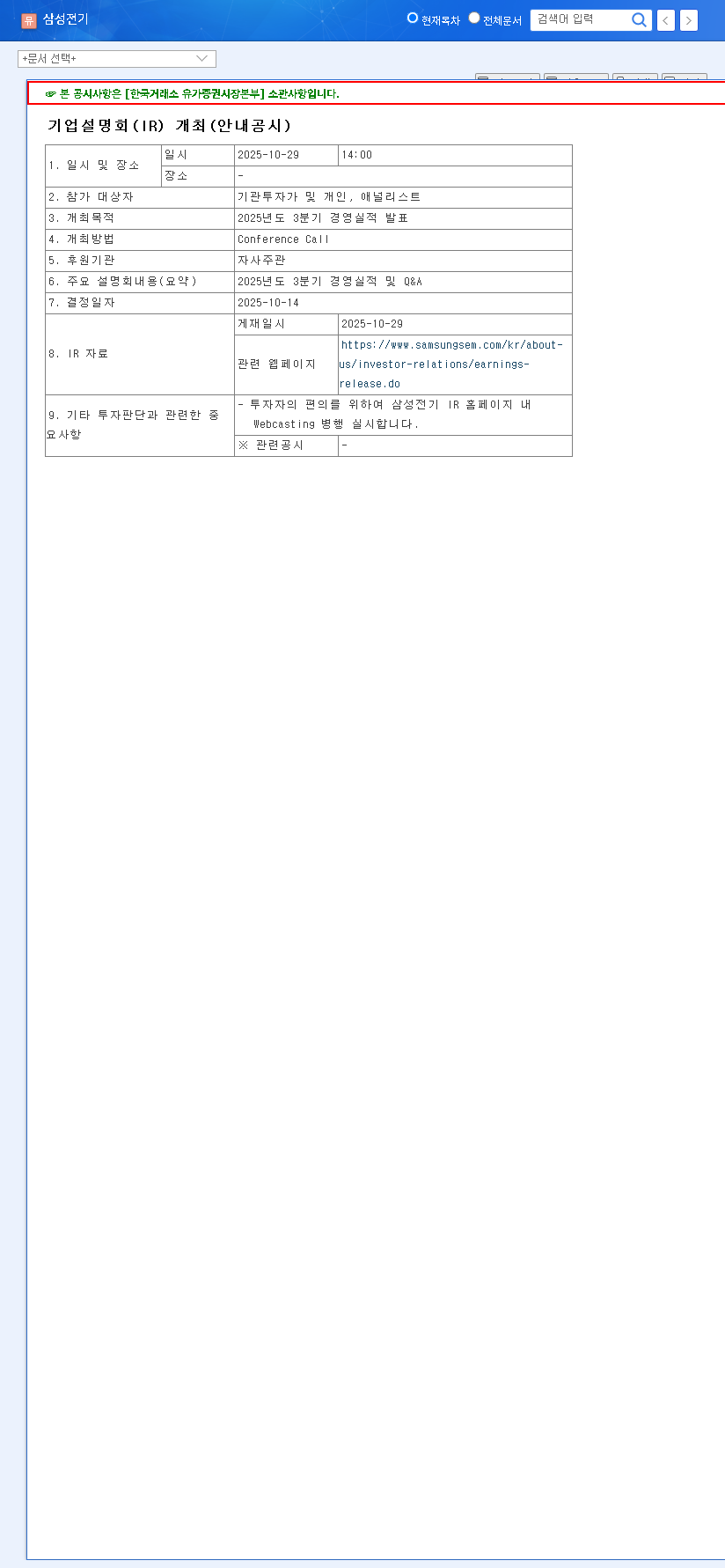

SAMSUNG ELECTRO-MECHANICS CO.,LTD will host its investor relations (IR) conference on October 29, 2025, at 2:00 PM KST to present its Q3 2025 financial results. This event is a critical opportunity for the market to gain clarity on the company’s performance and for management to address pressing questions about future strategy. The official filing can be viewed here: (Source: Official DART Disclosure).

Fundamental Analysis: The Core Business Drivers

Samsung Electro-Mechanics is built on three powerful pillars. Understanding their individual performance is key to a complete analysis of the upcoming financial results.

Positive Catalysts Driving Growth

- •Sustained Revenue Growth: Sales in H1 2025 grew a solid 6.5% year-over-year to KRW 5.5233 trillion, largely thanks to strong average selling prices for high-end MLCCs and camera modules.

- •Strategic Tech Investments: The company is doubling down on future growth markets. Increased R&D spending is targeted at high-value products like automotive-grade MLCCs for EVs and advanced package substrates for the booming AI and server markets.

- •Robust Financial Health: A remarkably low debt-to-equity ratio of 7.88% provides a stable foundation for weathering economic volatility and funding future capital expenditures.

Headwinds and Potential Risk Factors

- •The Profitability Puzzle: Despite higher sales, H1 2025 operating profit declined year-over-year. Rising raw material costs and lower utilization rates in the Package and Optical Solutions divisions are the primary culprits.

- •Macroeconomic Volatility: With significant global exposure, the company is sensitive to currency fluctuations. A volatile KRW/USD exchange rate and rising global interest rates pose tangible risks to margins and borrowing costs.

- •Intense Market Competition: Every business segment faces fierce competition, requiring relentless innovation in technology and cost management to maintain market share.

Key Watch Points for the Q3 Earnings Call

Investors should listen closely for management’s commentary on these critical areas during the investor relations call. The answers will directly influence market sentiment and the future of SAMSUNG ELECTRO-MECHANICS stock.

The central question is whether the company can translate its top-line revenue growth into bottom-line profitability. Commentary on operating profit margin improvement will be the most scrutinized detail of the entire announcement.

Performance Metrics for the SAMSUNG ELECTRO-MECHANICS Q3 2025 Earnings

- •Component Solutions: Look for updates on MLCC demand, particularly from the automotive sector, and pricing power. Is the IT demand cycle recovering as expected in H2?

- •Package Solutions: Focus on factory utilization rates. Has the demand for high-value server/AI substrates like FCBGA translated into improved profitability? For more on this, read our deep dive into the global semiconductor supply chain.

- •Optical Solutions: How is the premium smartphone market affecting camera module sales? Any new design wins or technological advancements in high-magnification optics?

- •Forward-Looking Guidance: What is the outlook for Q4 2025 and early 2026? Concrete strategies and order book updates for the AI and automotive segments will be crucial.

Investor Action Plan and Outlook

The Q3 earnings report will likely trigger short-term stock price volatility. A positive surprise in operating margin could lead to a significant rally, while a miss could see the stock test lower support levels. For long-term investors, the focus should be on whether management can present a credible path to sustainable, profitable growth. Confirmation of market share gains in high-value sectors and effective risk management against macroeconomic trends, as discussed by leading analysts on platforms like Bloomberg, will be vital for building long-term investor confidence.

In conclusion, the SAMSUNG ELECTRO-MECHANICS Q3 2025 Earnings release is more than a simple financial update; it’s a strategic referendum. While revenue growth is encouraging, the company must demonstrate its ability to control costs and improve profitability. A clear, confident vision for its role in the AI and automotive revolutions could unlock significant long-term value for shareholders.