The latest MERITZ FINANCIAL GROUP INC. Q3 2025 earnings report is out, and it paints a complex picture for investors. While the headline net profit surpassed market expectations, a slight miss on operating profit introduces a note of caution. This mixed signal requires a deeper investigation to understand the company’s true financial health and future trajectory.

In this comprehensive analysis, we will dissect the Q3 2025 performance, exploring the strengths and weaknesses across Meritz’s key business segments. We’ll examine the impact of the current macroeconomic climate and provide a forward-looking investment strategy. Our goal is to equip you with the insights needed to make informed decisions regarding your position in Meritz Financial Group.

MERITZ FINANCIAL GROUP INC. Q3 2025 Earnings at a Glance

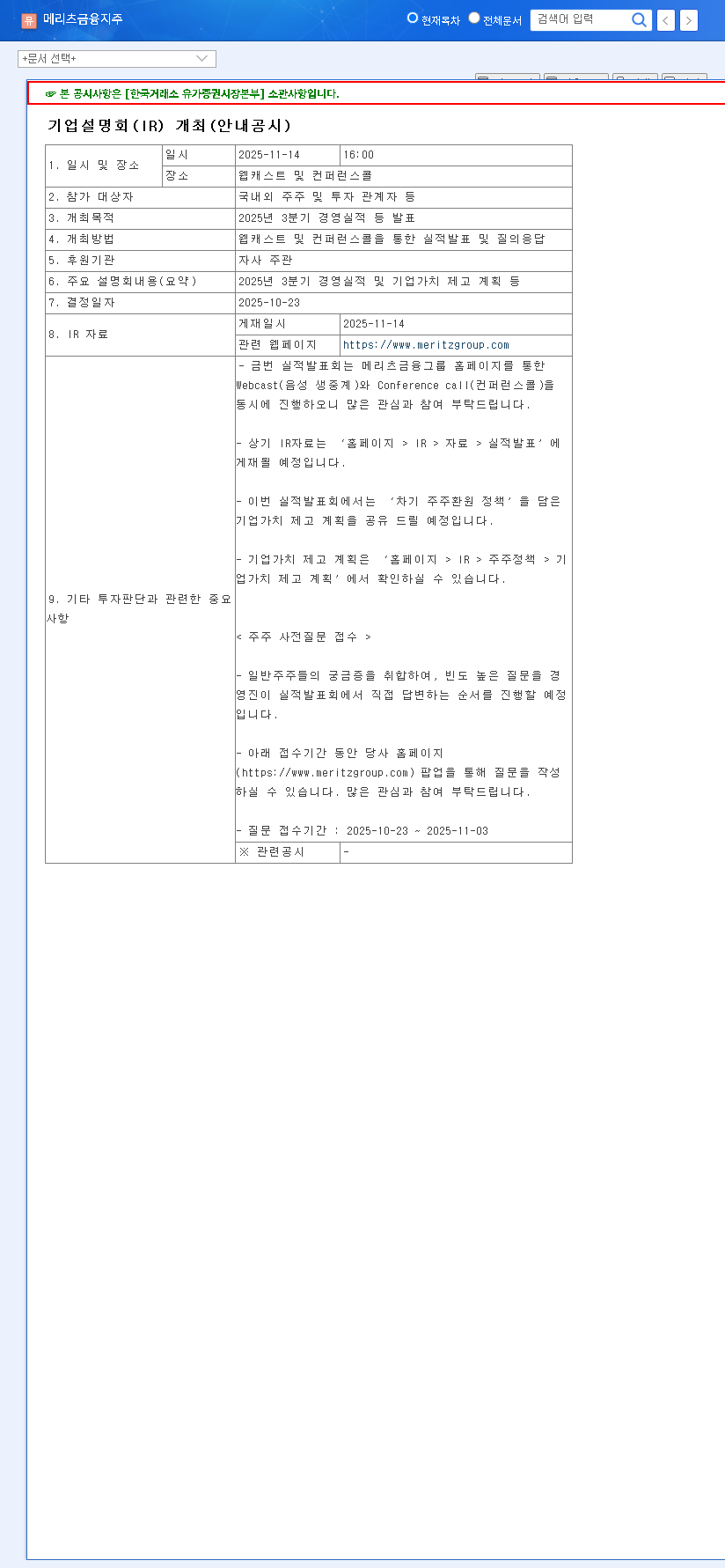

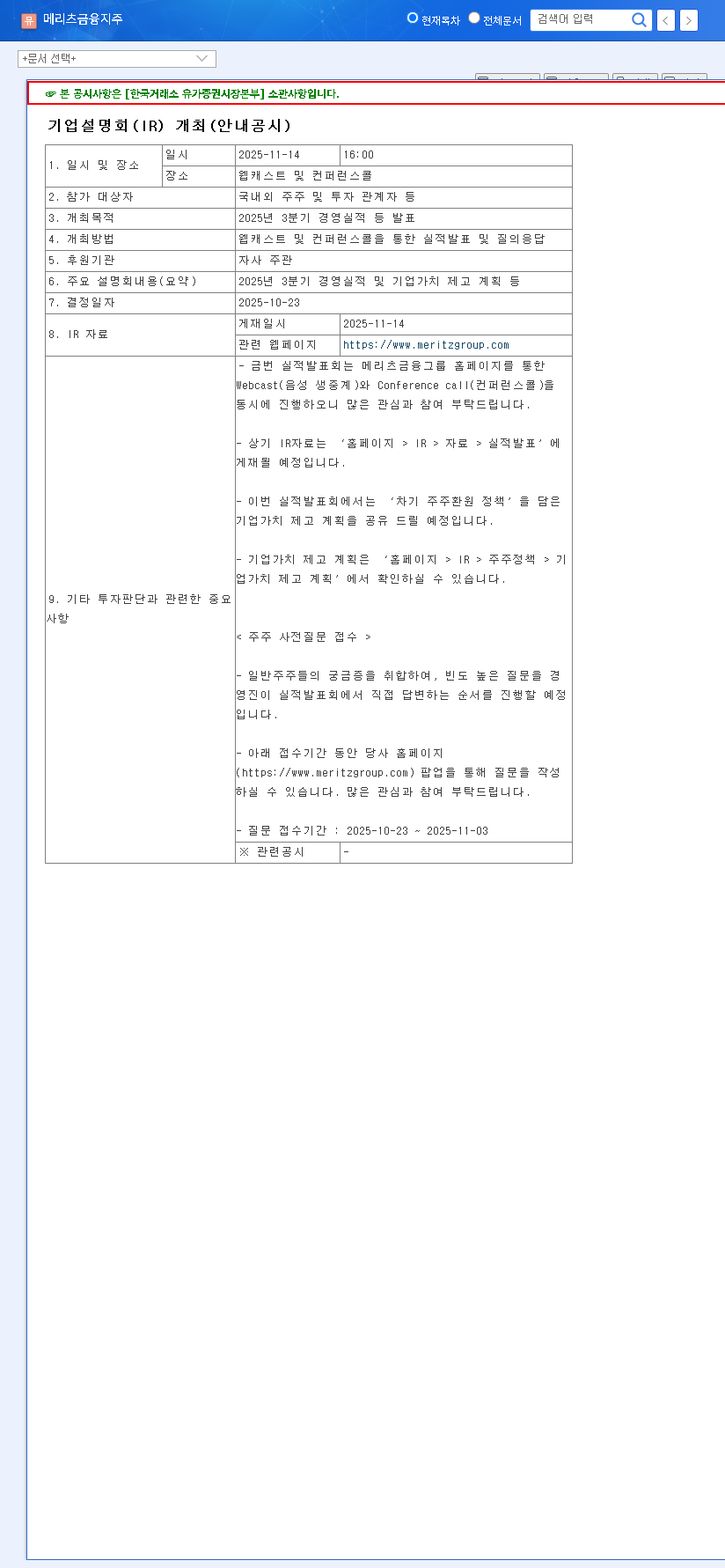

On November 14, 2025, MERITZ FINANCIAL GROUP INC. released its preliminary consolidated financial results. As detailed in the Official Disclosure filed with DART, the key figures reveal a story of resilience and specific challenges:

- •Revenue: KRW 7.3705 trillion

- •Operating Profit: KRW 862.3 billion (a ~1% miss versus consensus)

- •Net Profit: KRW 654.7 billion (a ~1% beat versus consensus)

The core takeaway is one of divergence: while operational efficiency faced minor headwinds, the bottom-line profitability proved stronger than anticipated, showcasing effective management across the group’s diverse portfolio.

Deep Dive: Segment Performance Analysis

To understand the mixed results, we must analyze the performance of each major subsidiary. The group’s diversified structure is a key strength, allowing strong segments to offset weaknesses elsewhere.

1. Meritz Fire & Marine (Non-Life Insurance)

The insurance arm continues to be the bedrock of stability. It demonstrated sustained growth, driven by a 4.0% increase in insurance revenue. This was supported by growth across all major lines, including long-term, auto, and general insurance. Critically, the company maintained a robust solvency ratio of 242.7%, well above regulatory requirements, indicating strong financial health. While net profit saw a minor dip, the segment’s fundamental growth trajectory remains positive.

2. Meritz Securities (Financial Investment)

Meritz Securities presented a tale of two businesses. The Institutional business, particularly Sales & Trading (S&T) and Corporate Finance (IB), performed exceptionally well, with net profits up 10% and 39% respectively. This highlights their strength in a volatile market. However, the Retail segment was a significant drag, with net profit plummeting 76%. This was largely a self-inflicted wound due to an aggressive zero-commission promotion aimed at capturing market share, a strategy that investors should monitor for long-term profitability. For more on this trend, see this analysis of brokerage commission wars.

3. Meritz Capital (Specialized Credit)

Meritz Capital focused on growth, increasing total assets by 15.5% and new loan origination by a substantial 37.3%. However, this growth came at a cost. Net profit declined by 12%, impacted by impairment charges on overseas investment assets and intensified competition in the credit finance industry. This reflects the challenging macroeconomic environment of higher interest rates, which can pressure lending margins and asset quality.

Investment Thesis & Strategic Outlook

Considering the MERITZ FINANCIAL GROUP INC. Q3 2025 earnings, what is the path forward for investors? The results highlight both a resilient core business and areas requiring strategic attention.

The Bull Case (Potential Upside)

- •Solid Fundamentals: The consistent performance of the non-life insurance segment provides a stable earnings base that can weather economic storms.

- •IB & S&T Strength: The securities division has proven its ability to generate significant profits from its institutional-facing businesses, a high-margin area.

- •Financial Soundness: High solvency and net capital ratios suggest the company is well-capitalized to handle market volatility and pursue growth opportunities.

- •Shareholder Returns: Stable earnings often lead to consistent shareholder return policies, such as dividends and buybacks, which are attractive to investors. Explore our guide on evaluating financial stocks for more on this.

The Bear Case (Risks to Monitor)

- •Macroeconomic Headwinds: The company is not immune to global trends. Persistently high interest rates, currency volatility, and geopolitical uncertainty can negatively impact its investment and lending profits.

- •Retail Profitability: The aggressive strategy in the securities retail segment is a drag on earnings. The market will be watching closely to see if the company can convert its new user base into a profitable one.

- •Intense Competition: The financial industry, particularly with the rise of fintech, is highly competitive. Meritz must continue to innovate to protect its market share and margins.

Frequently Asked Questions (FAQ)

Q1: What were the key takeaways from Meritz Financial Group’s Q3 2025 earnings?

The key takeaway is a mixed but resilient performance. Net profit exceeded expectations, driven by strong fundamentals in insurance and institutional securities. However, operating profit slightly missed forecasts due to weakness in the retail securities segment and pressure on the capital lending business.

Q2: Which business segment performed the best?

The Non-Life Insurance segment (Meritz Fire & Marine) was the most stable and robust performer, showing consistent growth in revenue and maintaining excellent financial health. Within Meritz Securities, the Corporate Finance (IB) division also showed outstanding growth.

Q3: What major risks should investors be aware of?

Investors should monitor the impact of global macroeconomic factors like interest rates and currency volatility. Internally, the key challenge is to improve profitability in the retail brokerage segment and manage asset quality within Meritz Capital amid fierce industry competition.

Disclaimer: This report is prepared for informational purposes based on publicly available data. The final responsibility for investment decisions rests solely with the investor.