The recent Vieworks Q3 2025 earnings report sent a significant shockwave through the investment community. Vieworks Co., Ltd., a recognized leader in high-performance digital X-ray detectors and industrial imaging solutions, announced preliminary results that fell dramatically short of market consensus. This unexpected downturn has left many investors questioning the company’s immediate trajectory and long-term health.

This in-depth Vieworks earnings analysis unpacks the critical numbers, diagnoses the underlying causes of the performance slump, and provides a strategic outlook for investors. We will explore whether this is a temporary setback or a sign of deeper structural issues, helping you formulate an informed strategy for your Vieworks stock position.

The Q3 2025 Earnings Shock by the Numbers

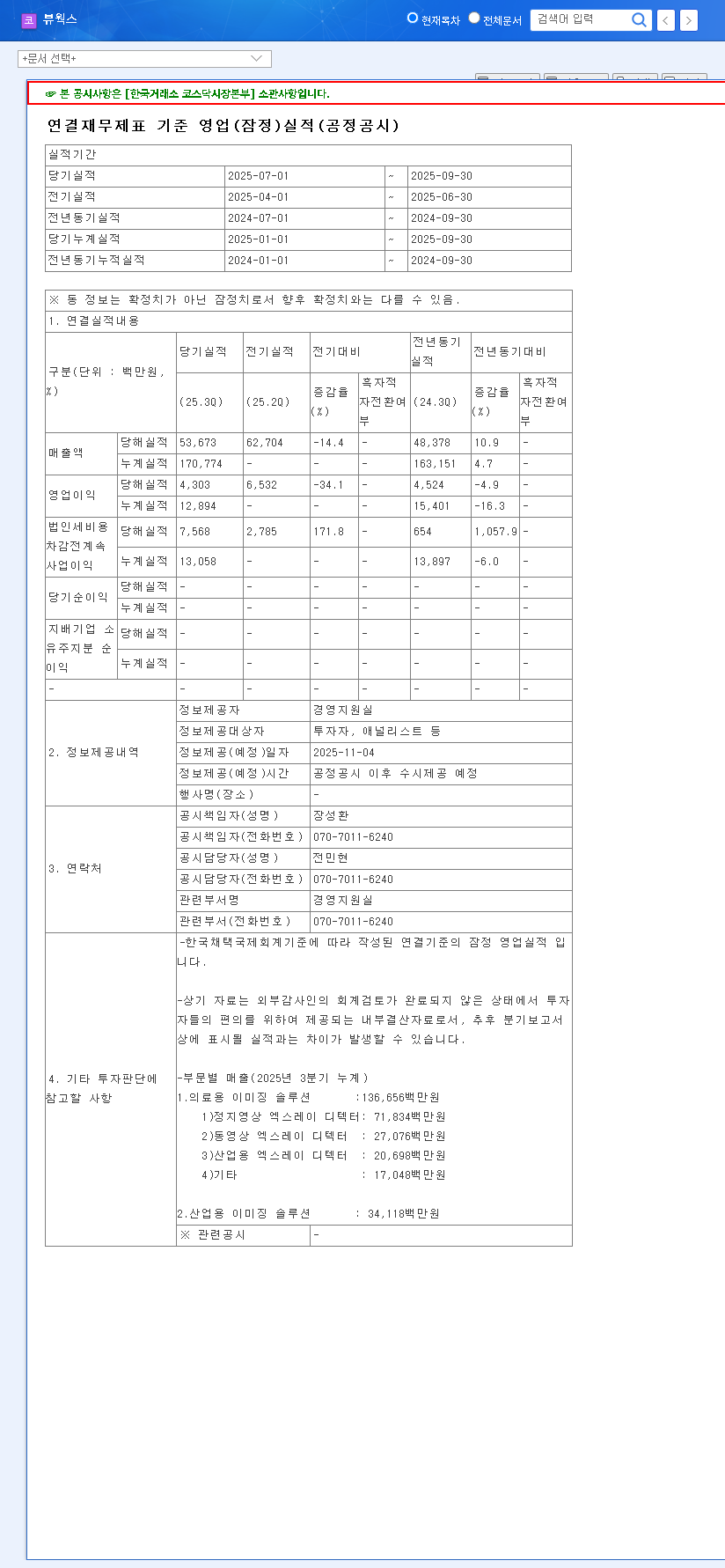

The preliminary Q3 results revealed a significant disconnect between expectations and reality. According to the Official Disclosure on DART, the key performance indicators were deeply concerning:

- •Revenue: KRW 53.7 billion, missing the forecast of KRW 55.9 billion by 4%.

- •Operating Profit: KRW 4.3 billion, a staggering 31% below the forecast of KRW 6.2 billion.

- •Net Profit: Significantly underperformed against the projected KRW 5.3 billion (final figure undisclosed).

The 31% miss on operating profit is the most alarming figure. It signals a severe deterioration in profitability that cannot be ignored and has understandably eroded short-term investor confidence.

Fundamental Diagnosis: What Went Wrong at Vieworks?

To understand the future, we must first diagnose the past. Our analysis, combining the semi-annual report with these Q3 results, points to a combination of internal and external pressures impacting the company.

1. Core Business Slowdown & Intensifying Competition

The engine of Vieworks’ revenue, its medical imaging segment, is sputtering. In the first half of 2025, sales of static imaging digital X-ray detectors fell by 8%, while dental dynamic detectors dropped by over 15%. This slowdown suggests a combination of market saturation and fierce competition from rivals. While the company’s foray into the high-potential digital pathology market is a promising long-term play, it’s not yet mature enough to offset the decline in its core business. For more on this emerging field, you can read about the latest trends in digital pathology.

2. Declining Financial Health

The Q3 earnings miss was foreshadowed by a weakening financial position in H1 2025. The company’s debt ratio climbed from 36.36% to 47.33%, and its net debt ratio more than doubled to 23.13%. This increased financial leverage makes the company more vulnerable to profit slumps and rising interest rates. On a positive note, Vieworks is not cutting back on innovation. The company invested a substantial KRW 13 billion in R&D (11.1% of revenue), a necessary gamble to secure future growth engines and maintain its technological edge in industrial imaging solutions and medical devices.

3. Macroeconomic Pressures and Volatility

As a global exporter, Vieworks is highly exposed to macroeconomic trends. While a strong US Dollar and Euro can lead to foreign exchange gains, it also increases the cost of imported raw materials, creating a double-edged sword for profitability. According to market analysis from high-authority sources like Bloomberg, global supply chain costs and interest rate policies continue to create an uncertain environment. On the bright side, falling oil prices and shipping costs could provide some relief by stabilizing production and logistics expenses in the coming quarters.

Investor Playbook: Navigating the Path Forward

The short-term outlook for Vieworks stock is undoubtedly challenging. The market will be looking for a clear turnaround story. Investors should monitor the following key areas to assess the company’s recovery potential:

- •Q4 Performance Rebound: Is the Q3 slump an anomaly? Watch the Q4 earnings report closely for signs of stabilization or recovery, particularly in the industrial imaging solutions segment, which has shown recent growth.

- •New Business Traction: Look for concrete evidence of market adoption and revenue generation from new ventures, especially the digital pathology system. Tangible results are needed to shift the growth narrative.

- •R&D Monetization: The heavy investment in R&D must translate into profitable new products. Monitor announcements for technological breakthroughs and product launches that can create new revenue streams.

- •Management’s Strategy: Pay close attention to the company’s official communications. Vieworks needs to articulate a clear, convincing plan to address profitability, manage costs, and navigate competition.

In conclusion, the Vieworks Q3 2025 earnings miss has rightfully put the company under a microscope. While significant challenges in core markets and financial health exist, its commitment to R&D and diversification into new growth areas provides a potential path to recovery. Cautious and diligent monitoring of the key performance areas outlined above will be essential for any investor looking to navigate this period of uncertainty.