The latest MCNEX Q3 2025 earnings report has sent ripples through the investment community. For stakeholders in MCNEX CO.,LTD (KRX: 097520), the preliminary numbers revealed a significant shortfall in profitability, raising critical questions about the company’s trajectory. While revenue held steady, a shocking miss on operating profit has become the central point of concern.

This comprehensive MCNEX stock analysis moves beyond the surface-level data. We will dissect the factors behind the earnings decline, evaluate the company’s foundational strengths that remain intact, and outline a strategic investment thesis for navigating this pivotal moment. This report provides the clarity needed to make informed decisions regarding your MCNEX investment.

Deconstructing the Q3 2025 Earnings Shock

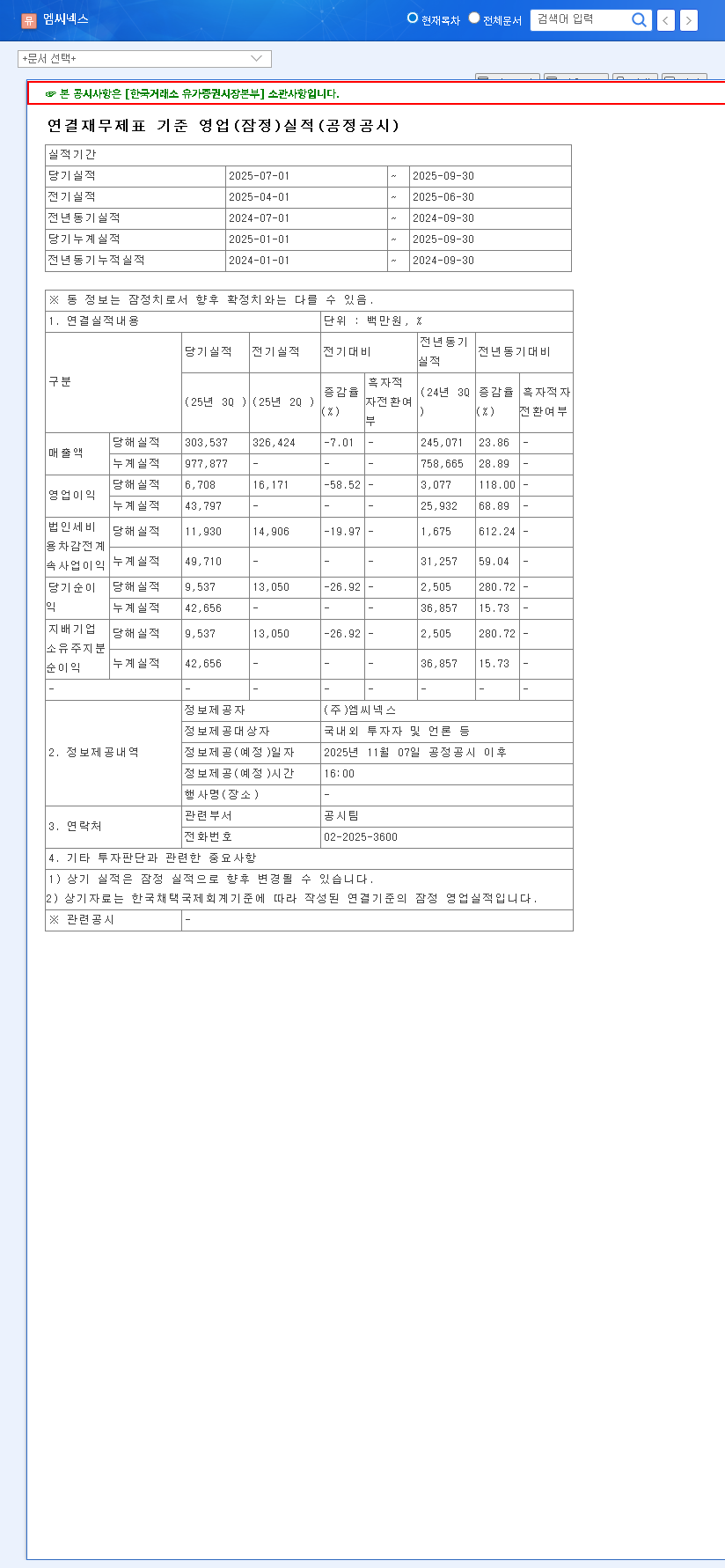

MCNEX’s consolidated preliminary earnings for the third quarter of 2025 presented a mixed but ultimately worrying picture. While revenue met expectations and even grew 23.8% year-on-year—a respectable feat in a sluggish smartphone market—the story on profitability was starkly different. The core issue lies with the MCNEX operating profit.

The most significant takeaway from the 097520 earnings report is the operating profit of 6.7 billion KRW, which missed the market consensus of 12.5 billion KRW by a staggering 46%. This massive deviation has understandably amplified concerns about deteriorating profitability.

This isn’t just a minor miss; it signals a sharp reversal of the positive profitability trend observed up to the second quarter. The primary culprits appear to be a combination of rising costs, pricing pressures, and potential inefficiencies that squeezed margins far more than analysts anticipated.

Why Did Profitability Decline So Sharply?

Several headwinds converged in Q3 to impact MCNEX’s bottom line. Understanding these factors is key to assessing whether this is a temporary setback or a more systemic issue.

- •Intense Smartphone Market Competition: The global smartphone market continues to face sluggish demand. This environment breeds intense competition, forcing component suppliers like MCNEX to accept lower average selling prices (ASPs) to secure orders from major manufacturers.

- •Rising Cost Burden: As highlighted in previous reports, volatility in raw material prices for camera modules likely intensified in Q3. Without the ability to pass these costs onto customers, margins were directly compressed.

- •Adverse Exchange Rate Fluctuations: While a strong Korean Won can benefit importers, for an exporter like MCNEX, it can be a double-edged sword. It can increase the cost of imported raw materials while also making final products more expensive in foreign currency terms, potentially impacting competitiveness.

Long-Term Growth Drivers Remain Intact

Despite the concerning MCNEX Q3 2025 earnings, it’s crucial for investors to look beyond a single quarter. The company’s long-term fundamentals and strategic positioning offer a compelling counternarrative.

Exceptional Financial Stability

As of H1 2025, MCNEX maintained an exceptionally healthy balance sheet. With a debt-to-equity ratio of just 50.99% and a net debt-to-equity ratio near zero (1.48%), the company has a formidable financial cushion. This stability allows it to weather short-term storms, continue funding critical R&D, and pursue strategic growth without relying on costly external financing.

Leadership in the Automotive Camera Market

The most exciting part of the MCNEX story is its growing dominance in the automotive sector. As the industry shifts towards autonomous driving and advanced driver-assistance systems (ADAS), the demand for high-performance automotive cameras is exploding. According to market research from firms like Gartner, this market is projected to grow exponentially. MCNEX’s established technology and expanding list of automotive clients position it perfectly to capture a significant share of this high-margin business, which will be a key driver of future profitability.

Investment Outlook: A Neutral Stance with a Watchful Eye

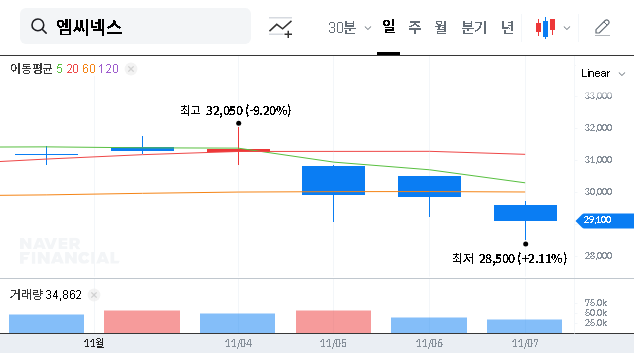

Given the severity of the operating profit miss, we anticipate near-term downward pressure on MCNEX’s stock price. The market will need time to digest this information and seek clarity from management. Therefore, we are adopting a “Neutral” investment opinion at this time. This is not a signal to sell, but rather a call for caution and diligent monitoring.

Investors should closely watch for the following developments, which will be critical in shaping the future MCNEX investment thesis:

- •Management’s Q4 Guidance: The company’s official outlook and explanation for the Q3 results will be paramount. Look for a clear, credible plan to address the margin compression.

- •Automotive Business Momentum: Track announcements related to new automotive contracts and the actual revenue contribution from this segment. Strong growth here could offset weakness in mobile.

- •Profitability Restoration Strategy: Investors need to see concrete steps, such as cost optimization, a focus on high-value products, or renegotiated contracts. Our Guide to Analyzing Tech Company Margins provides more context on this.

For a detailed breakdown of the preliminary figures, investors can review the Official Disclosure on DART.

Conclusion: A Warning Signal, Not a Fundamental Collapse

In summary, the MCNEX Q3 2025 earnings report is a clear warning sign that investors cannot ignore. However, it does not invalidate the company’s strong financial health or the massive growth potential of its automotive business. The coming months will be crucial. A strategic and effective response from management could present a valuable long-term entry point for patient investors, while a failure to address these profitability issues could signal deeper problems. Vigilance is key.