The latest SM Entertainment earnings report for Q3 2025 sent a significant tremor through the market, as the K-Pop powerhouse posted results that fell dramatically short of analyst expectations. For investors holding SM Entertainment stock (041510), this news raises critical questions about the company’s current trajectory, its integration with Kakao, and its future growth prospects. This comprehensive analysis will unpack the Q3 results, explore the underlying causes of the underperformance, and provide a clear action plan for investors navigating this period of uncertainty.

The Q3 2025 Earnings Shock: A Numbers Breakdown

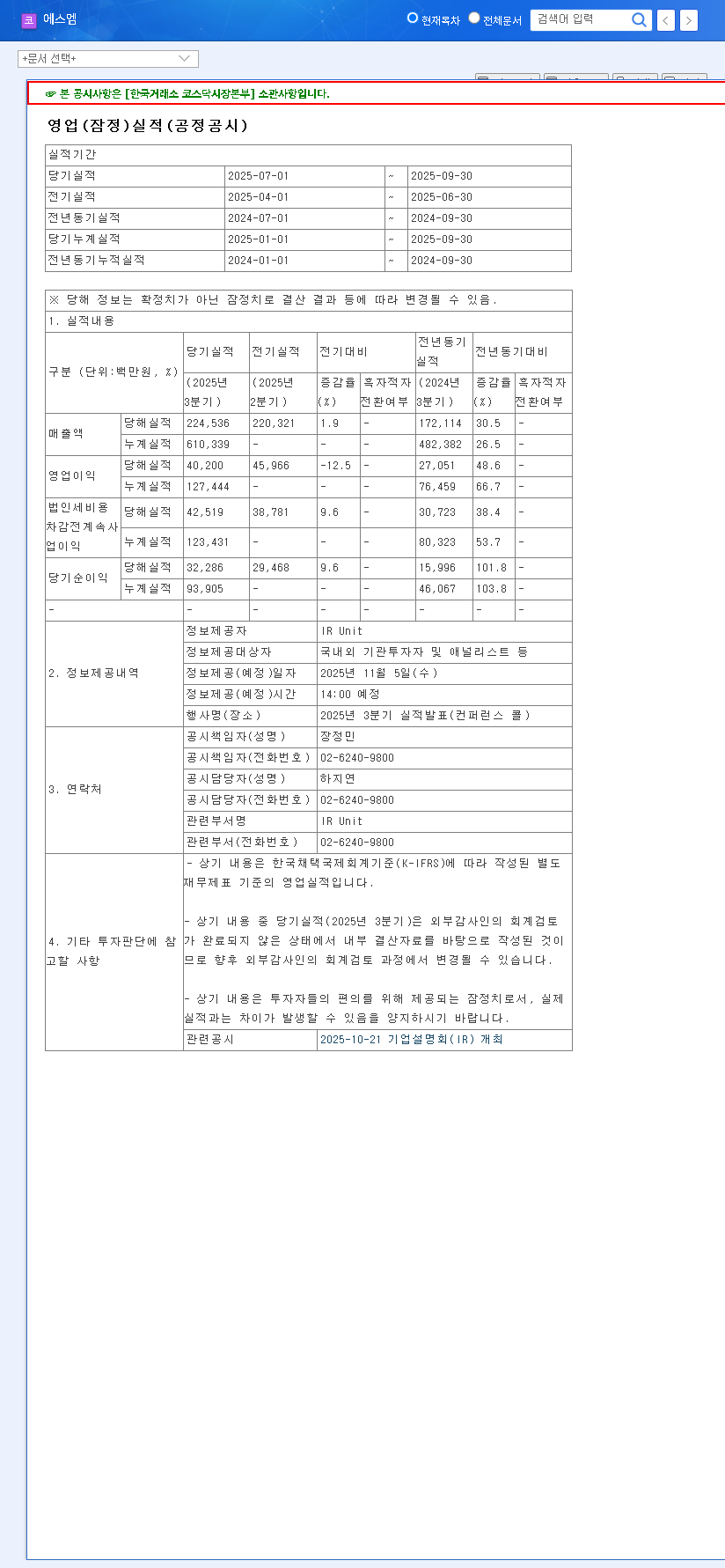

On November 5, SM Entertainment released its preliminary Q3 2025 operating results, which immediately soured investor sentiment. The figures revealed a significant disconnect between market forecasts and actual performance across all key metrics. These figures are based on the company’s public filing, which can be reviewed via the Official Disclosure on DART.

Key Financials vs. Market Consensus

- •Revenue: KRW 224.5 billion, a staggering 31% decrease from the expected KRW 327.7 billion.

- •Operating Profit: KRW 40.2 billion, a 15% decrease from the anticipated KRW 47.4 billion.

- •Net Profit: KRW 32.3 billion, a 13% decrease from the forecast of KRW 37.2 billion.

This pronounced underperformance signals that the revenue challenges identified in the first half of the year have not only persisted but have intensified, raising fundamental concerns about the company’s core operations and strategic investments.

Root Causes: What Drove the Decline?

The poor SM Entertainment earnings are not the result of a single issue but rather a combination of structural problems, delayed synergies, and struggling business segments.

Weakness in Core Entertainment and Advertising

The revenue shortfall was most apparent in two key areas. The core entertainment business, including album/digital sales and artist management, saw significant drops. This could be due to a lighter comeback schedule for top-tier artists or lower-than-expected sales from new intellectual property (IP). Simultaneously, the advertising business collapsed, with revenue falling from KRW 71.4 billion to KRW 21.2 billion. This indicates a severe difficulty in monetizing K-Pop IP in a competitive advertising landscape and a failure to create compelling synergies that attract major brands.

Aggressive Investments Yet to Bear Fruit

SM Entertainment has been on an investment spree, with intangible assets growing 239% year-on-year to KRW 589.5 billion by H1 2025. This includes major M&A activity and acquisitions like additional shares in DEAR U. While aimed at securing future growth, these aggressive moves have increased the short-term financial burden (evidenced by falling cash reserves and rising liabilities) without yet delivering tangible returns. This is part of a broader trend in the K-Pop entertainment industry, where companies are diversifying heavily.

The market is now questioning whether these long-term bets will pay off, especially as the promised synergy with majority shareholder Kakao remains largely theoretical. The slow integration and lack of visible collaborative projects are a key source of investor concern.

Outlook for SM Entertainment Stock and Investors

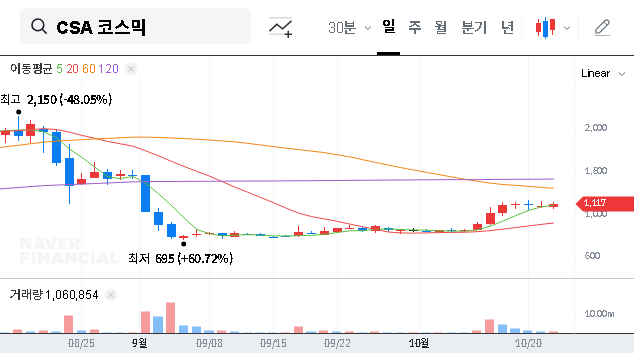

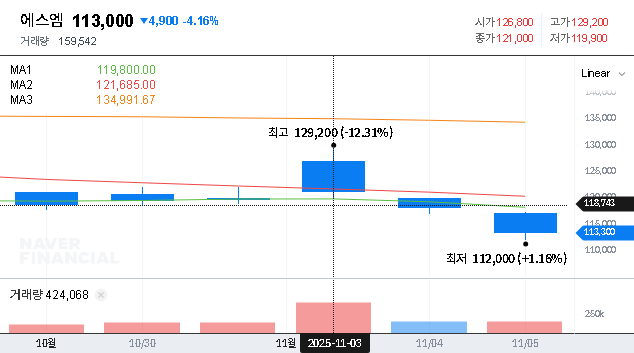

In the wake of this earnings report, investors should brace for short-term volatility. A significant miss on SM Entertainment earnings will almost certainly trigger a re-evaluation of the company’s valuation by analysts, as noted by sources like Bloomberg. This could lead to downward price pressure as the market digests the news.

However, it’s not all doom and gloom. SM Entertainment’s foundational strength lies in its powerful artist IP and dedicated global fandoms. This provides a degree of downside resilience. The long-term thesis still hinges on whether the company can successfully leverage this IP, execute its investment strategy, and finally unlock the synergy potential with Kakao’s vast tech and content ecosystem.

Investor Action Plan: Key Watchpoints

For those invested in or considering SM Entertainment stock, a cautious and watchful approach is paramount. Focus on these critical indicators in the coming months:

- •Q4 Guidance & Rebound Potential: The company’s forecast for the next quarter will be crucial. Look for a clear, credible strategy for revenue recovery and cost management.

- •Artist Pipeline & New IP Performance: Monitor upcoming comeback schedules for major artists (e.g., NCT, aespa) and the commercial success of any new group debuts. This is the lifeblood of revenue.

- •Tangible Kakao Synergy: Move beyond promises. Watch for concrete joint ventures, content collaborations on Kakao’s platforms, or integrated global marketing efforts that generate actual revenue.

- •Profitability and Cost Control: While operating profit fell less than revenue, the company must demonstrate structural improvements in cost efficiency to protect margins during this period of revenue weakness.

In conclusion, the Q3 2025 SM Entertainment earnings were a clear setback. While the company retains immense potential, it is at a critical juncture where it must prove it can execute its ambitious strategy and translate its assets into sustainable financial growth. Investors are advised to proceed with caution and diligence.