The recent news surrounding the potential DOUZONE BIZON management rights sale has created significant turbulence for investors. Initial media reports, followed by a clarifying disclosure from the company, have left the market in a state of flux. This uncertainty directly impacts the DOUZONE BIZON stock outlook, forcing shareholders to navigate a complex landscape of rumors and official statements. This comprehensive analysis will break down the situation, explore future scenarios, and provide a clear investor strategy for making informed decisions.

We will dissect this pivotal issue by examining what has happened, why it’s critical for the company’s future, the potential short-term and long-term consequences, and what actionable steps investors should consider now.

The Timeline: Unpacking the Sale Rumors

The controversy began with a media report and was quickly followed by an official company response, creating a timeline of events that investors must understand.

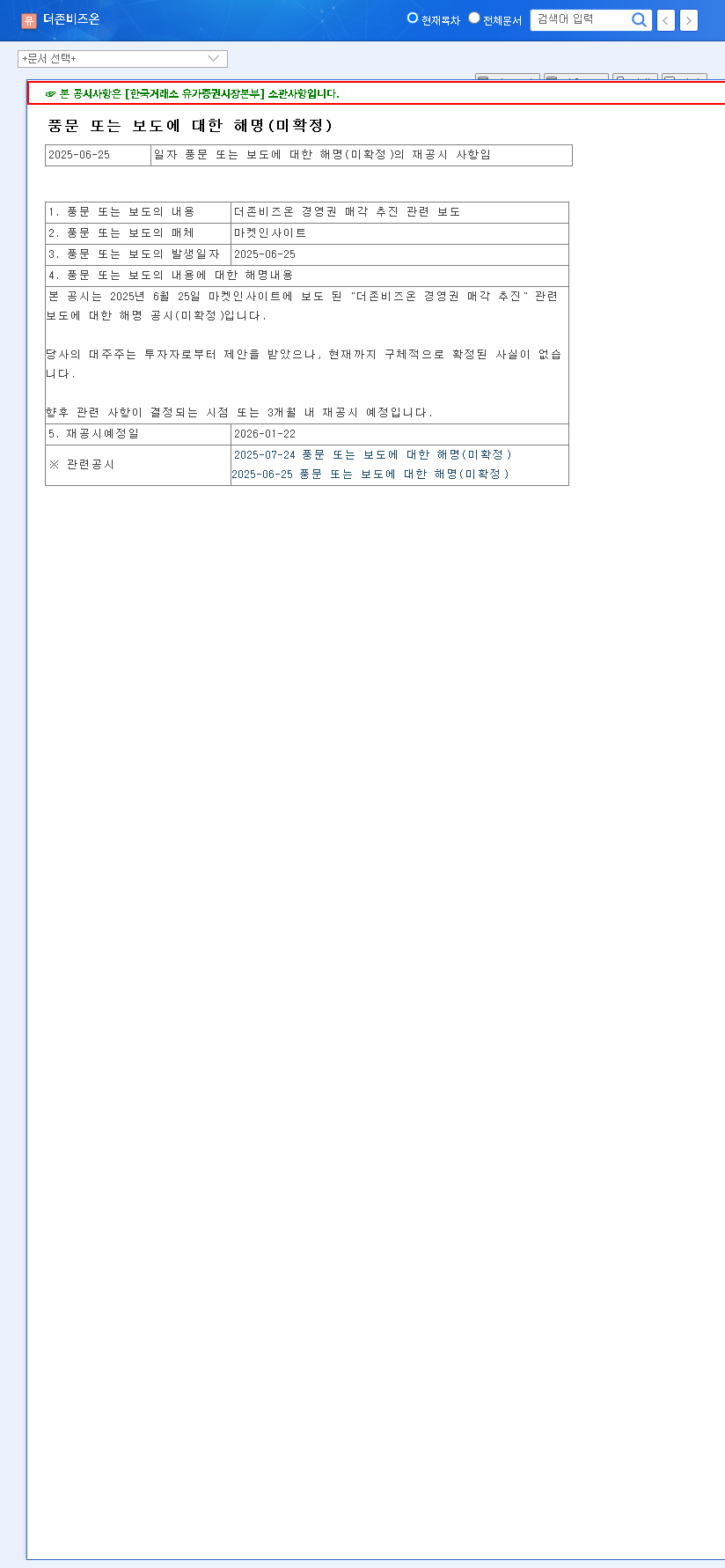

- •Initial Report (June 25, 2025): Market Insight, a financial news outlet, first published a report suggesting that a DOUZONE BIZON management rights sale was being actively pursued.

- •Company Disclosure (October 23, 2025): In response, DOUZONE BIZON issued a formal clarification. They stated that while the major shareholder had received proposals, nothing was confirmed. This ambiguity is the primary source of current market uncertainty. You can view the Official Disclosure on the DART system.

- •Next Milestone (January 22, 2026): The company has committed to a re-disclosure by this date, which is now the most anticipated event for anyone following the DOUZONE BIZON stock.

Why This M&A News is a Game-Changer

A change in management control is one of the most transformative events a public company can experience. The ‘unconfirmed’ status creates an information vacuum, leading to heightened stock price volatility as traders bet on different outcomes. The core of the uncertainty lies in the unknown identity and intentions of the potential acquirer.

For investors, an M&A rumor is a double-edged sword. It can unlock hidden value or introduce paralyzing uncertainty. The key is to separate speculation from the company’s underlying fundamental strength.

Without clear guidance, investors may overreact to market chatter rather than focusing on DOUZONE BIZON’s intrinsic value, such as its market position in the ERP software industry, financial health, and long-term growth prospects. This period demands a steady hand and a focus on facts over fear.

Potential Scenarios and Stock Impact

The outcome of the re-disclosure will likely push the company and its stock into one of three primary scenarios. Understanding these possibilities is crucial for a sound investor strategy.

Positive Scenario: A Successful, Strategic Sale

If the sale is confirmed with a strategic buyer at a premium valuation, the market could react very favorably. A new major shareholder could inject fresh capital, accelerate technological innovation, or provide access to new international markets. This could lead to a re-evaluation of the company’s long-term worth and a significant appreciation in the DOUZONE BIZON stock price.

Negative Scenario: Sale Fails or Uncertainty Drags On

Conversely, if the re-disclosure announces that the deal has fallen through or is indefinitely delayed, the market could be hit with a wave of disappointment selling. The stock price may fall as speculative investors exit their positions. Prolonged uncertainty can also harm the business itself, distracting management from core operations and delaying critical investments.

Neutral Scenario: A Return to Fundamentals

It’s also possible that a sale proceeds but with a less dramatic immediate impact. For example, a financial buyer like a private equity firm might maintain the current strategy while focusing on operational efficiencies. In this case, the stock price would likely revert to trading based on the company’s fundamental performance—revenue growth, profitability, and market share.

Investor Action Plan: How to Navigate the Uncertainty

Given the high stakes, a cautious and well-researched approach is essential. Here is a recommended action plan for navigating the ongoing situation.

- •Focus on the Re-disclosure: The January 22, 2026, re-disclosure is the single most important catalyst. Mark this date and be prepared to analyze the details, such as the identity of the buyer, the sale price, and any stated strategic rationale.

- •Analyze Company Fundamentals: Look past the M&A noise. Is DOUZONE BIZON’s core business strong? Examine their recent financial reports, competitive standing, and product pipeline. A strong underlying business provides a margin of safety regardless of the sale outcome. For more on this, check out our guide on how to analyze a company during M&A rumors.

- •Implement Risk Management: The high volatility warrants caution. Avoid making oversized bets on a single outcome. Consider portfolio diversification and a disciplined approach to buying or selling shares. Understanding M&A arbitrage strategies can also provide context, as explained by authoritative sources like Investopedia.

- •Monitor Market Sentiment: After the disclosure, watch how institutional investors and analysts react. Their interpretations can often set the tone for the stock’s direction in the following weeks.

In conclusion, the DOUZONE BIZON management rights sale saga presents both risks and opportunities. While the future remains uncertain until the next official announcement, investors who remain informed, patient, and focused on fundamental value will be best positioned to navigate the path ahead.