Recent corporate filings from Daesung Hi-Tech have sparked conversations among investors about a noteworthy change in its major shareholder’s stake. While the adjustment itself is minor, the implications for management stability and the company’s future direction are significant. This comprehensive analysis dives deep into the official disclosure, evaluating the company’s underlying financial health and technological strengths to provide a clear picture for potential investors.

We will explore what this shareholder activity truly signals and whether it’s enough to bolster confidence in Daesung Hi-Tech stock amidst challenging financial headwinds. Understanding the full context is key to making an informed decision about this high-precision technology firm.

The Disclosure Decoded: A Closer Look at the Filing

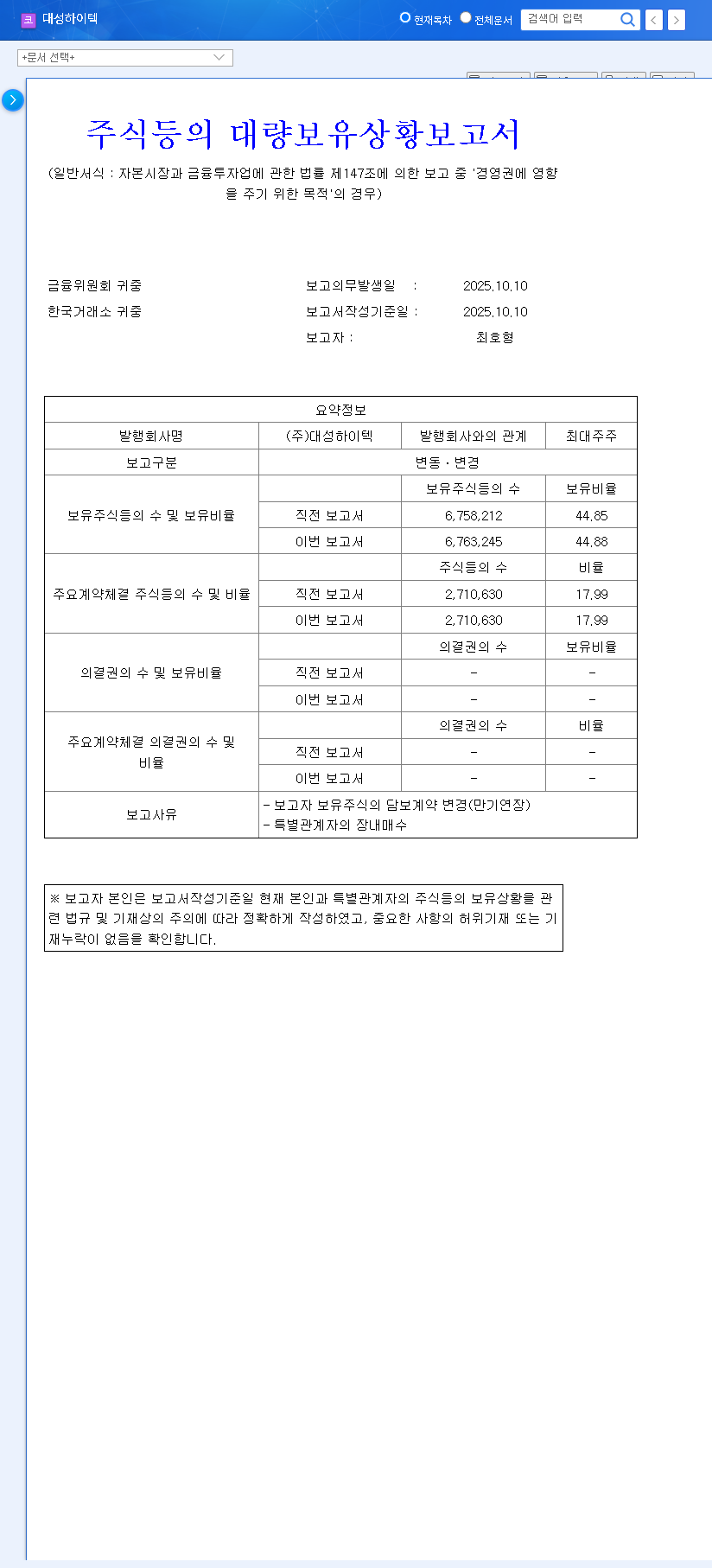

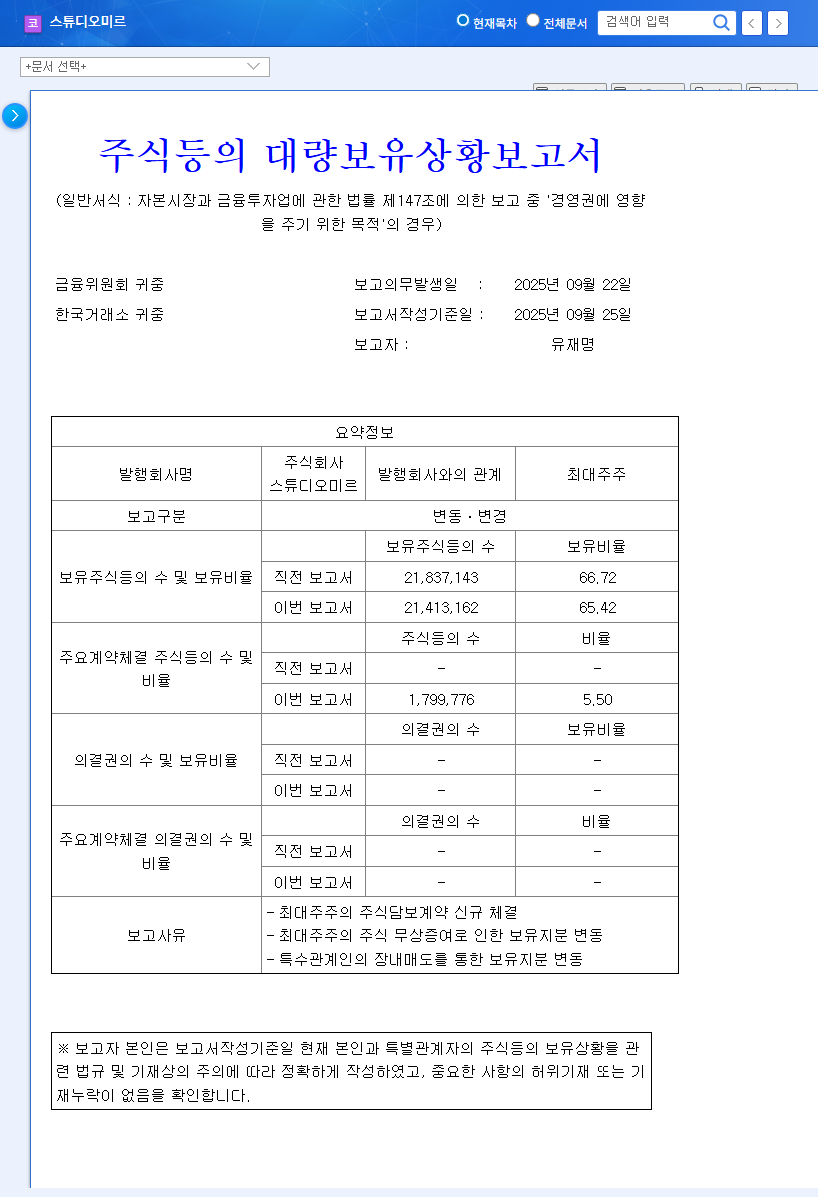

On October 10, 2025, Daesung Hi-Tech submitted a mandatory ‘Report on the Status of Large Shareholding in Stocks, etc.’ to financial regulators. This filing, detailed in an Official Disclosure, outlined several key points:

- •Stake Increase: CEO Choi Ho-hyung and related parties increased their collective stake from 44.85% to 44.88%, a marginal gain of 0.03 percentage points. This was primarily driven by an on-market purchase of 5,033 shares by a related party.

- •Stated Purpose: The declared reason for the holding is to ‘influence management,’ signaling a clear intent to maintain and solidify control over the company’s strategic direction.

- •Collateral Extension: Crucially, the maturity date for existing collateral agreements on the held shares was extended. This move secures the current ownership structure and reduces the risk of forced selling or instability related to loan terms.

Understanding Daesung Hi-Tech: Technology Powerhouse Facing Hurdles

Founded on a bedrock of over two decades of high-precision processing technology, Daesung Hi-Tech boasts a strong competitive position in several niche markets. Its core business revolves around three main pillars: precision parts, Swiss-type automatic lathes, and compact machining centers. The company is a Top 5 global player in the Swiss-type lathe market and is carving out a significant presence in high-growth sectors like electric vehicle (EV) components.

However, this technological prowess is currently overshadowed by significant financial challenges. In the first half of 2025, the company reported troubling figures: a 49.2% year-on-year drop in sales revenue, an operating loss of KRW 1.71 billion, and a net loss of KRW 5.29 billion. This performance has strained its balance sheet, leading to a high debt-to-equity ratio of 240.44% and substantial inventory levels, which can impact cash flow.

The central conflict for investors is weighing Daesung Hi-Tech’s impressive technological capabilities and market position against its pressing short-term financial weaknesses.

Signal vs. Substance: The True Impact on Daesung Hi-Tech Stock

The recent shareholder stake change is best interpreted as a strategic move to reinforce management stability. While the 0.03% increase is numerically insignificant, the act of purchasing shares on the open market sends a message of internal confidence. It suggests that leadership believes the company’s stock is undervalued and is committed to its long-term recovery and growth. Extending the collateral agreements further solidifies this stability, removing a potential source of market uncertainty.

However, this event does not fundamentally alter the company’s financial reality. The positive signal cannot, on its own, resolve issues like declining revenue, negative profitability, or high debt. Therefore, while it might provide a small, short-term positive sentiment boost, a sustained rally in Daesung Hi-Tech stock is unlikely until tangible improvements in financial performance are demonstrated. For context on market sentiment, investors often track trends on platforms like Bloomberg’s market analysis pages.

Investor Action Plan: A Prudent, Long-Term Approach

For those considering an investment in Daesung Hi-Tech, a patient and observant strategy is paramount. The focus should be on fundamental business improvements rather than short-term market noise. Here are the key areas to monitor:

1. Track Performance Turnaround

Scrutinize upcoming quarterly earnings reports for signs of revenue stabilization and a return to profitability. Pay close attention to the performance of new growth drivers, such as contracts in the defense, medical device, and EV sectors. Tangible results here are the most powerful catalyst for the stock.

2. Monitor Financial Health Metrics

Keep an eye on the company’s efforts to manage its high debt-to-equity ratio and improve inventory turnover. Any successful debt restructuring or reduction in inventory would be a strong positive signal. For a deeper dive, consider learning how to analyze a company’s balance sheet.

3. Assess Long-Term Growth Potential

Ultimately, the investment thesis for Daesung Hi-Tech rests on its long-term potential. The strengthened management stability provides a solid foundation, but the execution of its growth strategy is what will create shareholder value. A prudent decision requires balancing the company’s technological edge against its current financial burdens, waiting for clear evidence of a sustainable operational recovery.