The recently announced DL E&C 2025 earnings outlook has sent ripples through the investment community. With ambitious projections of KRW 7.5 trillion in revenue and KRW 380 billion in operating profit, DL E&C CO.,LTD. (375500) presents a bold vision for its future. However, this optimism stands in stark contrast to the company’s recent financial performance, creating a critical dilemma for current and potential investors. Is this a sign of a monumental turnaround or an overly ambitious forecast? This comprehensive DL E&C stock analysis will dissect the fundamentals, macroeconomic landscape, and financial realities to provide a clear investment strategy.

Deconstructing the DL E&C 2025 Earnings Outlook

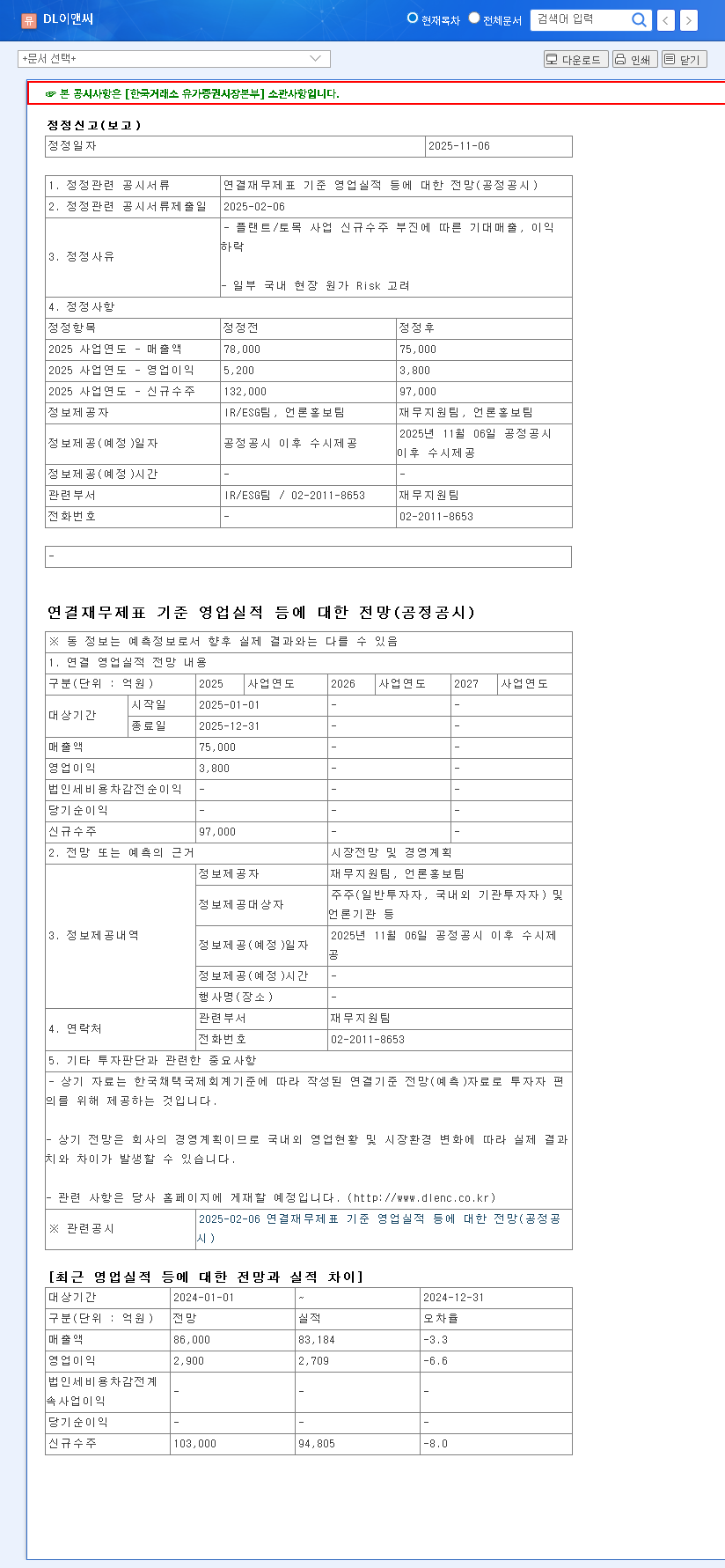

According to its official corporate disclosure, DL E&C has set significant targets for its 2025 fiscal year. The numbers, as detailed in the Official Disclosure (Source: DART), are:

- •Consolidated Revenue: KRW 7,500 billion

- •Operating Profit: KRW 380 billion

These projections are not just numbers; they represent the company’s strategic direction. However, when juxtaposed with a recent trend of declining profitability—including a projected operating loss for the current period—they demand rigorous scrutiny. For investors, understanding the feasibility of this turnaround is paramount.

Current State: A Look at DL E&C’s Financial Health and Fundamentals

To evaluate the 2025 forecast, we must first understand the company’s foundation. A deep dive into the DL E&C financial health reveals both significant challenges and underlying strengths.

Financial Soundness: A Mixed Picture

Recent financial indicators paint a concerning picture. The company has experienced a downward trend in both revenue and operating profit from 2022 to 2024. Key metrics like a negative net profit margin, falling Return on Equity (ROE), and a debt-to-equity ratio surpassing 100% signal financial pressure. Furthermore, a sharp decline in the current ratio raises valid concerns about short-term liquidity. These are critical red flags that any potential DL E&C investment must consider.

Brand Competitiveness and Technological Edge

Despite financial headwinds, DL E&C possesses formidable assets. With over 80 years in the industry, its brand equity is undeniable, anchored by premier residential brands like ‘e편한세상’ and the luxury ‘ACRO’ line. More importantly, the company is actively investing in its future by adopting next-generation construction technologies such as Building Information Modeling (BIM), Advanced Work Packaging (AWP), AI-driven project management, and modular construction. These innovations are crucial for improving efficiency, reducing costs, and securing a competitive advantage in a complex market.

The core challenge for investors is to weigh DL E&C’s deteriorating short-term financials against its long-term brand strength and technological investments. The path to achieving the 2025 outlook will depend on how effectively the latter can overcome the former.

Macroeconomic Factors at Play

No construction company operates in a vacuum. DL E&C’s performance is intrinsically linked to a complex web of external economic forces.

- •Real Estate & Government Policy: With residential projects forming the bulk of its revenue (58.7%), the company is highly sensitive to real estate market cycles and government regulations. Diversification into rental housing is a strategic move to mitigate this risk.

- •Interest Rates & Raw Materials: Globally, anticipated interest rate cuts could ease financing burdens. However, a strong KRW/USD exchange rate can increase the cost of imported materials. Conversely, falling oil prices may provide some cost relief.

- •Overseas Projects: Large-scale international ventures, like the Shaheen Project, offer significant profit potential but also expose the company to currency fluctuation risks that require careful management.

The Investor’s Action Plan: A Prudent Strategy

Given the high degree of uncertainty, a cautious and research-driven approach is essential for anyone considering a DL E&C investment. The gap between the ambitious 2025 forecast and current reality is substantial, suggesting that the stock price may face short-term volatility as the market digests this information. For further context on market trends, investors often consult analysis from high-authority sources like leading financial news outlets.

Investors should meticulously monitor the following key performance indicators before making a decision:

- •New Order Pipeline: Track the announcement of significant new domestic and overseas contracts that can substantiate the revenue forecast.

- •Quarterly Profit Margins: Look for sequential improvement in operating and net profit margins as a leading indicator of a turnaround.

- •Debt and Liquidity Management: Monitor changes in the debt-to-equity and current ratios for signs of improving financial stability.

- •Macroeconomic Shifts: Stay informed on interest rate policies, currency trends, and commodity prices that directly impact profitability. For a deeper understanding, explore our complete guide to analyzing construction stocks.

In conclusion, while the DL E&C 2025 earnings outlook presents a compelling bull case, the path to achieving it is fraught with challenges. A successful outcome hinges on a favorable economic shift, flawless execution of major projects, and the tangible benefits of its technological investments. Until concrete evidence of this turnaround emerges, a prudent, watch-and-wait strategy is advised.