In a significant development for the semiconductor industry, FADU INC., a key player in the data center SSD controller market, has announced a landmark FADU INC. SSD supply contract. This colossal deal, valued at KRW 21.6 billion, represents a staggering 49.60% of the company’s projected 2025 revenue. This news has understandably sent ripples through the investment community, raising critical questions: What does this mean for FADU’s future trajectory? And how should potential investors strategically approach FADU stock now? This comprehensive analysis will break down the contract details, explore the company’s fundamentals, and provide a clear outlook on the investment implications.

Deconstructing the Landmark KRW 21.6 Billion Deal

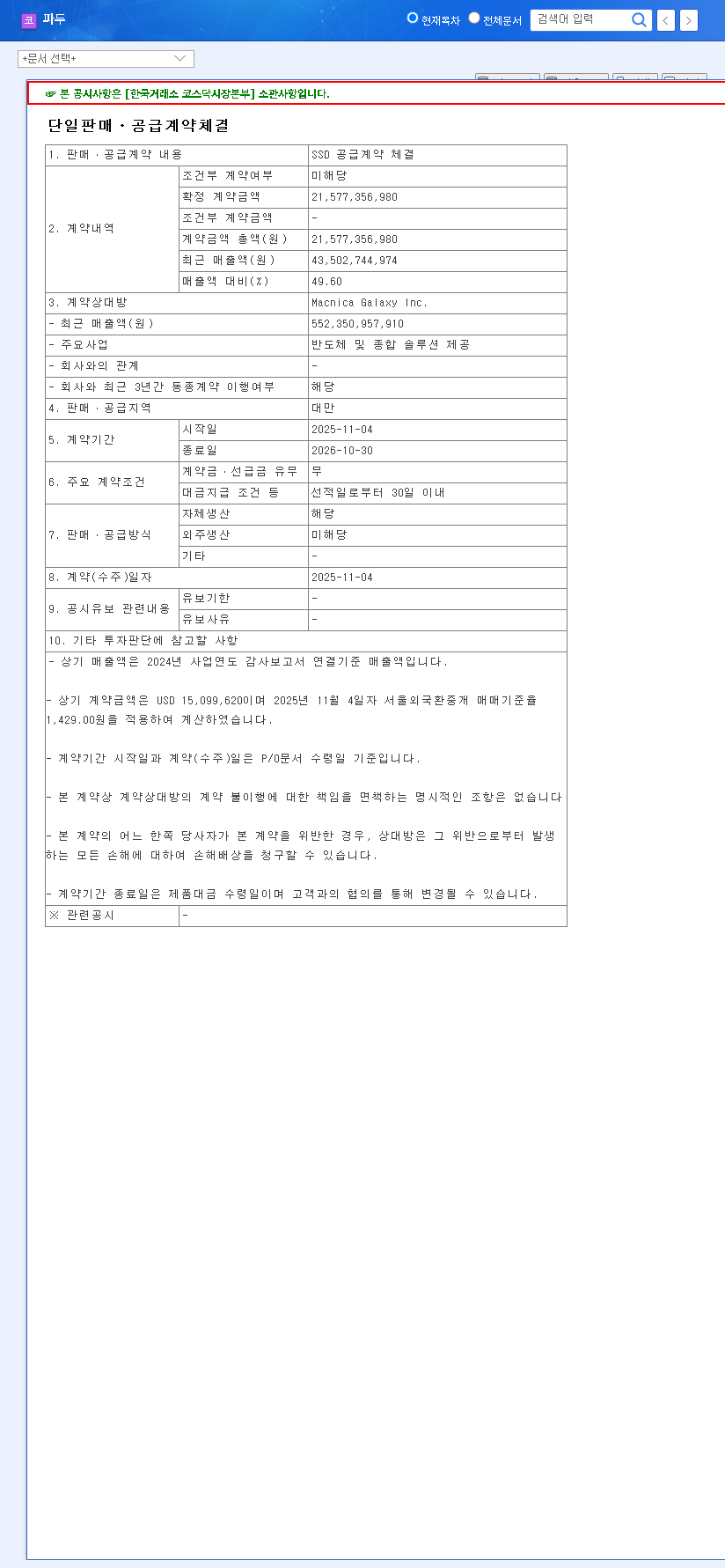

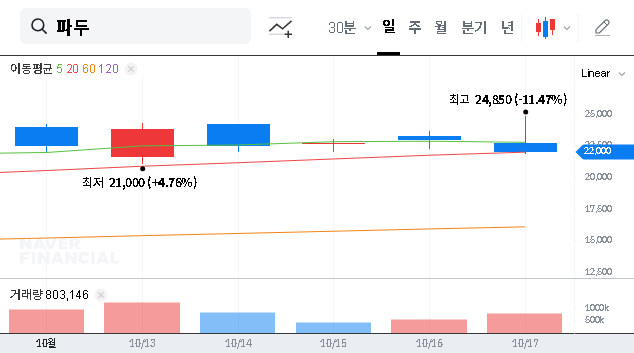

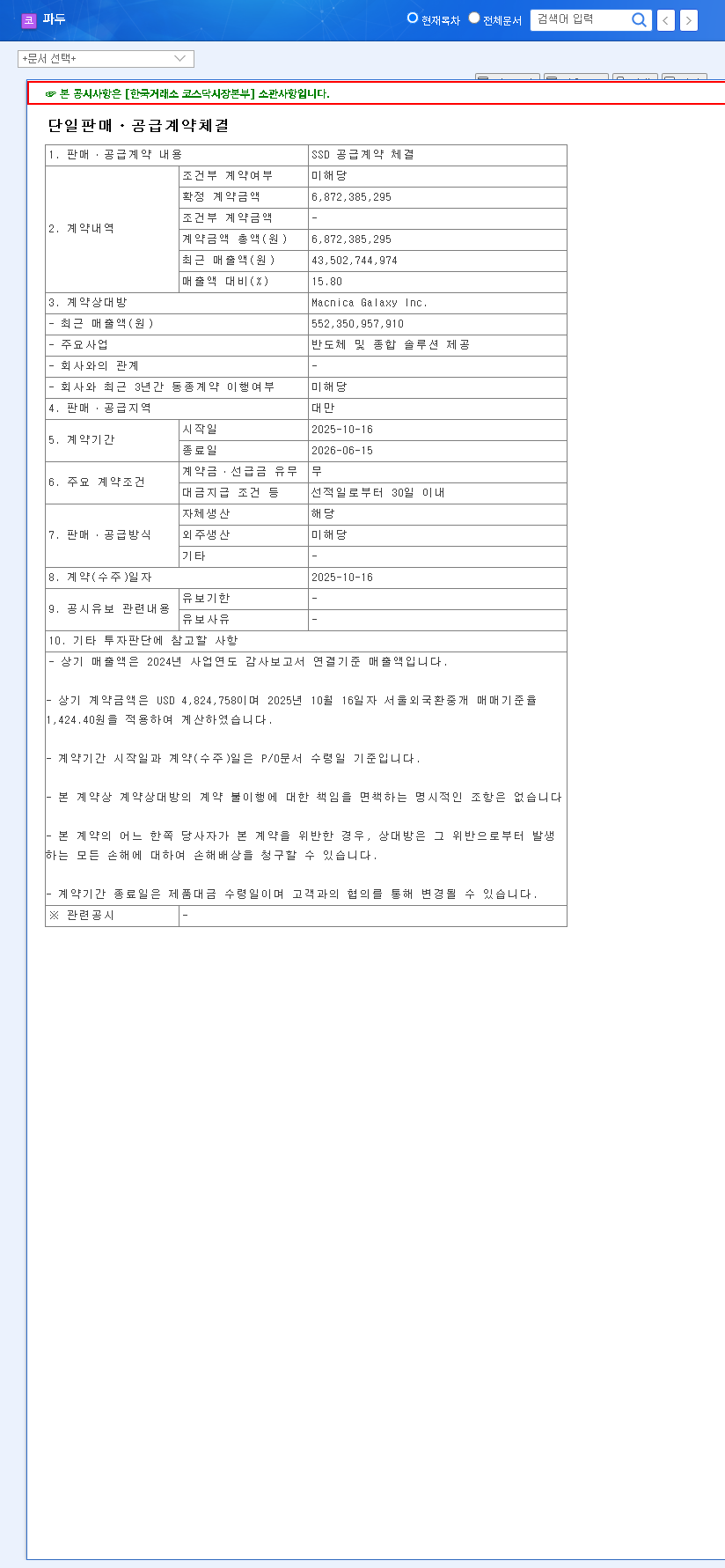

On November 5, 2025, FADU officially disclosed the signing of a major SSD supply agreement with Macnica Galaxy Inc., a prominent technology distributor. This isn’t just another contract; it’s a foundational piece of FADU’s revenue strategy for the upcoming fiscal year. The agreement, which can be viewed in the Official Disclosure on DART, outlines a 12-month supply period to Taiwan, running from November 2025 to October 2026. At approximately USD 16.6 million, the deal provides exceptional revenue visibility and significantly de-risks the company’s short-term sales forecasts.

This contract single-handedly accounts for nearly half of FADU’s estimated 2025 revenue, making its successful execution the most critical factor for the company’s performance over the next year.

FADU’s Corporate Health: A Fundamental Analysis

To understand the true weight of this FADU INC. SSD supply contract, we must look at the company’s current operational and financial landscape. While the deal is a massive win, it exists within a complex context of challenges and opportunities.

Financial Performance and Profitability Hurdles

While FADU has demonstrated positive revenue growth, a key concern for investors has been its negative net profit margins. This indicates that despite growing sales, the company is not yet profitable, a common challenge for tech firms in a high-growth, high-spend phase. Factors like inventory valuation losses have previously impacted the bottom line. Therefore, a primary question surrounding this new contract is whether the profit margins are sufficient to help FADU pivot towards sustained profitability.

Core Technology and Long-Term Growth Engines

FADU’s core strength lies in its competitive position within the high-demand data center SSD controller market. The company is not resting on its laurels; it is actively investing in next-generation technologies like PCIe Gen5 and CXL (Compute Express Link). These advancements are crucial for handling the massive data loads of AI and cloud computing, positioning FADU at the forefront of the industry. For more information on market trends, you can explore reports from authoritative sources like Gartner’s semiconductor analysis. However, this commitment to R&D comes with significant costs, which can temporarily suppress short-term profits.

Impact Analysis: Opportunities and Risks

The deal’s impact is twofold, presenting both clear benefits and potential risks that warrant careful consideration.

The Bull Case: Positive Catalysts

- •Secured Revenue Pipeline: The contract provides a rock-solid revenue foundation for the next 12 months, drastically improving financial predictability.

- •Global Market Validation: Securing a major deal in Taiwan with a partner like Macnica Galaxy Inc. reinforces FADU’s global competitiveness and expands its footprint in the critical Asian tech market.

- •Path to Profitability: If managed efficiently, this surge in revenue could provide the scale needed to overcome fixed costs and finally achieve positive net profit margins.

The Bear Case: Risks to Monitor

- •Customer Concentration Risk: With one contract representing nearly 50% of revenue, FADU’s performance is now heavily dependent on a single client relationship. Any disruption to this contract would be highly impactful.

- •Margin Uncertainty: The announcement focuses on top-line revenue. The actual profitability of the deal remains unknown and is a critical variable for long-term FADU stock analysis.

- •Macroeconomic Headwinds: The global semiconductor market is notoriously cyclical and sensitive to interest rates, currency fluctuations, and geopolitical tensions, all of which remain as external risks.

Investor Action Plan & Strategic Outlook

Given the evidence, how should investors view FADU? The new supply contract is undeniably a major positive catalyst. It provides a clear growth narrative for the short term.

The primary focus for any FADU investment thesis must shift to monitoring execution and profitability. Investors should closely watch quarterly earnings reports for commentary on the contract’s progress and, most importantly, its contribution to the bottom line. Furthermore, securing additional large-scale contracts will be key to proving this is a sustainable growth model and not a one-off event. For those interested in diversifying within this space, learning about investing in other semiconductor stocks could provide valuable context.

Final Assessment

In conclusion, the FADU INC. SSD supply contract is a transformative event that solidifies the company’s revenue base and validates its market position. It shifts the narrative from potential to proven demand. However, the journey towards sustainable profitability is still in progress. Cautious optimism is warranted. The contract provides a powerful tailwind, but investors must remain diligent in monitoring profitability metrics and the company’s efforts to diversify its customer base over the long term.