LS Eco Energy Ltd. (KRX: 229640) has sent ripples through the investment community with its preliminary Q3 2025 earnings report. While top-line revenue remained largely stable, a significant and unexpected miss on operating and net profit has raised critical questions about the company’s short-term health and trajectory. For investors tracking LS Eco Energy stock, this moment demands a deeper, more nuanced understanding than the headlines suggest.

This comprehensive LS Eco Energy analysis will dissect the Q3 performance, explore the underlying factors contributing to the shortfall, and provide a clear, actionable investment strategy for both short-term traders and long-term believers in the company’s vision.

The Q3 2025 Earnings Shock: By the Numbers

On October 28, 2025, LS Eco Energy released its preliminary consolidated operating results. According to the Official Disclosure, the key figures fell short of market consensus:

- •Revenue: KRW 232.8 billion (vs. KRW 236.2 billion estimate, a -1.4% miss)

- •Operating Profit: KRW 14.8 billion (vs. KRW 15.8 billion estimate, a -6.3% miss)

- •Net Profit: KRW 9.8 billion (vs. KRW 13.6 billion estimate, a staggering -28.0% miss)

The 28% shortfall in net profit is the most alarming figure. It signals that underlying issues beyond simple revenue fluctuations—such as soaring costs, operational inefficiencies, or one-time charges—have severely eroded the company’s bottom line this quarter.

What Went Wrong? An In-depth LS Eco Energy Analysis

To understand the Q3 shock, we must look at the preceding performance and external pressures. The deviation from the positive trend established in the first half of 2025 is stark and warrants a closer examination.

A Reversal from a Strong First Half

Prior to this report, the narrative around LS Eco Energy was overwhelmingly positive. The first half of 2025 saw robust year-on-year growth, primarily driven by its powerhouse Vietnamese subsidiaries, LS-VINA Cable & System and LS Cable & System Vietnam. Demand for power cables in the region was booming. Concurrently, the company was making strategic pivots into high-growth sectors like submarine cables—a critical component of the offshore wind industry—and rare earth materials, positioning itself for future success. This strong fundamental story makes the Q3 results even more jarring.

Dissecting the Profitability Plunge

The Q3 performance represents a significant downturn compared to the immediately preceding quarter (Q2 2025), where the company posted an operating profit of KRW 23.6 billion and a net profit of KRW 18.2 billion. The Q3 figures show a roughly 37% drop in operating profit and a 46% collapse in net profit quarter-over-quarter. This isn’t a minor dip; it’s a cliff. Potential culprits include:

- •Raw Material Costs: Volatility in the prices of electrolytic copper and aluminum, key inputs for cables, may have spiked unexpectedly, squeezing margins.

- •Currency Headwinds: While a strong USD can help exporters, unfavorable hedges or volatility in other currencies like the EUR could have negatively impacted financials.

- •One-Off Expenses: There could be undisclosed one-time costs related to new business investments, asset write-downs, or legal settlements that decimated net profit.

Investment Strategy for LS Eco Energy Stock (229640)

Given the conflicting signals—a strong long-term strategy versus a deeply concerning quarterly report—investors need a clear framework for their next steps.

Short-Term Caution is Advised

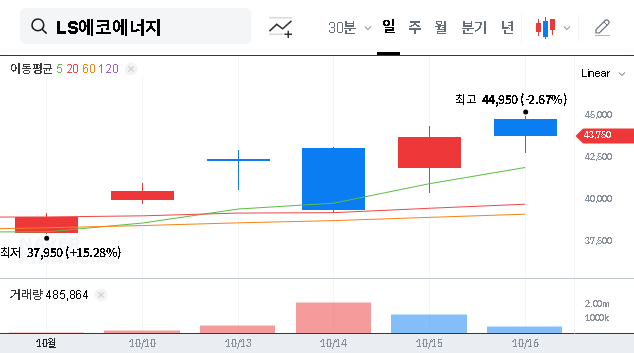

In the immediate term, the market is likely to punish the 229640 stock price. The uncertainty created by the massive net profit miss will weigh heavily on investor sentiment. A conservative, wait-and-see approach is prudent until the company provides a detailed explanation in its full Q3 report. Any new investment should be considered high-risk until there is clarity on whether these issues are temporary or systemic.

Mid-to-Long-Term Potential Remains Intact

The long-term investment thesis for LS Eco Energy has not been invalidated by one bad quarter. The company’s strategic initiatives in high-demand areas are still highly relevant. For a broader view on market trends, high-authority sources like Bloomberg’s analysis of the global energy transition confirm the massive demand for cable infrastructure. Furthermore, as we detail in our deep dive into the submarine cable market, this sector is poised for exponential growth. Investors with a longer time horizon may see any significant price drop as a buying opportunity, provided the following points are monitored closely.

4 Key Factors to Monitor Before Investing

- 1.Clarity on the Q3 Shortfall: The company’s official, detailed Q3 report is paramount. Look for a transparent explanation of the profit miss. Was it a one-time event or a structural problem?

- 2.Margin Recovery in Q4: Watch the company’s forward-looking guidance. Are they implementing strategies to manage costs and foreign exchange risk more effectively? Evidence of margin stabilization in the next quarter will be crucial.

- 3.New Business Milestones: Track tangible progress in their new ventures. This includes securing major contracts for submarine cables, advancing rare earth processing capabilities, and progress on IDC centers.

- 4.Geopolitical Risk Management: Keep an eye on updates regarding their Myanmar operations. Any signs of stabilization or successful risk mitigation in this politically volatile region would be a positive signal.

Conclusion: A Balanced Outlook

In summary, the LS Eco Energy earnings for Q3 2025 present a classic case of short-term pain versus long-term potential. While the immediate market reaction will likely be negative due to the severe profit miss, the company’s foundational strengths and strategic direction remain compelling. Prudent investors should demand clarity on the recent performance before making new commitments, while long-term holders should focus on the key monitoring points to ensure the company gets back on track.