The latest SUNG KWANG BEND Q3 2025 earnings report has landed, presenting a complex but revealing picture for investors. The company, a key player in the industrial fittings sector, announced strong revenue figures that surpassed market expectations. However, a miss on operating profit has introduced a note of caution, leaving many to wonder about the underlying health and future trajectory of SUNG KWANG BEND stock. These figures are far more than just numbers on a spreadsheet; they are critical signals about the company’s operational efficiency, market position, and resilience in a dynamic economic environment. This comprehensive earnings analysis will dissect the results, explore the challenges and opportunities ahead, and provide a clear roadmap for formulating a prudent investment strategy.

Q3 2025 Preliminary Earnings: The Headline Figures

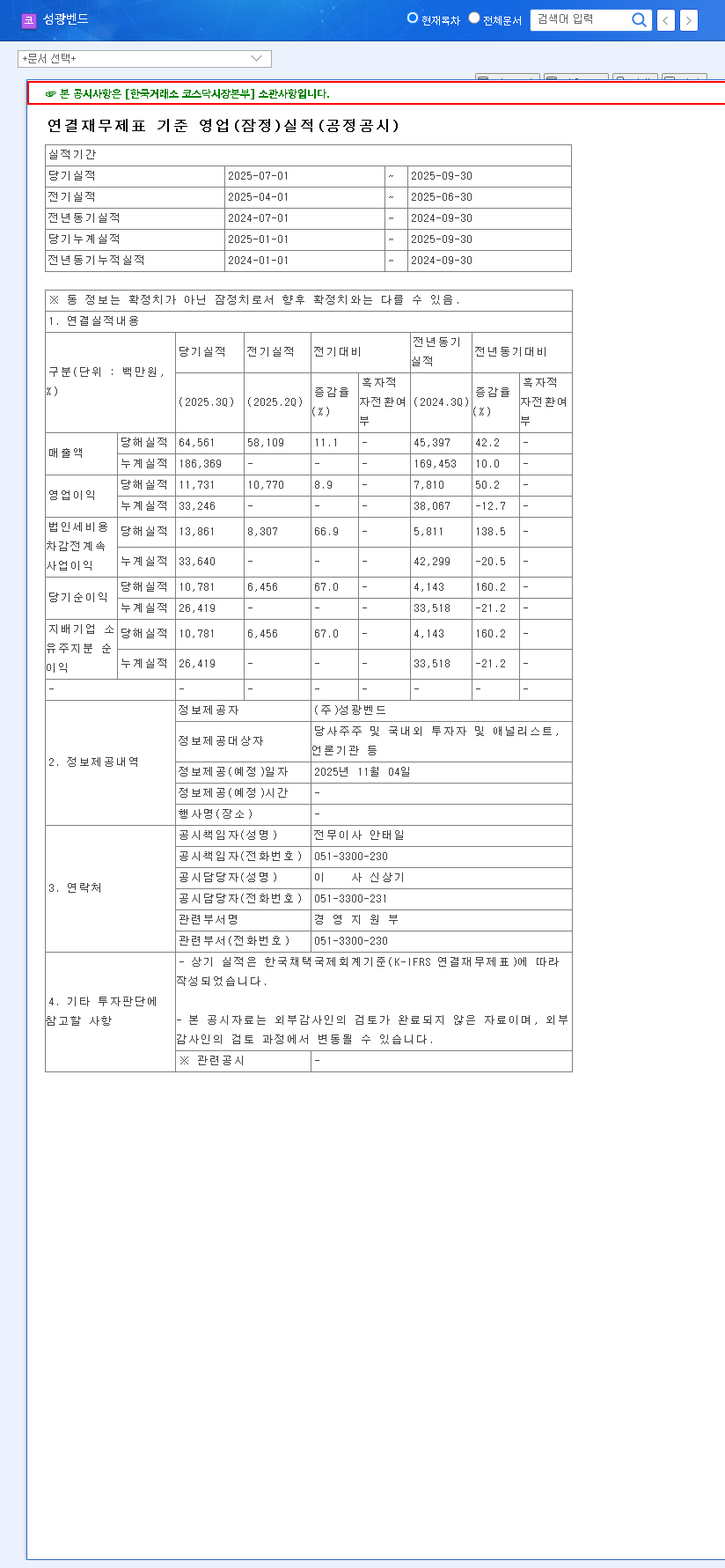

On November 4, 2025, SUNG KWANG BEND released its preliminary operating results, revealing a mixed but intriguing performance. The official numbers, as filed, can be viewed in the Official Disclosure (DART). Here are the key takeaways:

- •Revenue: KRW 64.6 billion, which is approximately 5.4% above market consensus.

- •Operating Profit: KRW 11.7 billion, falling about 3.3% below market forecasts.

- •Net Profit: KRW 10.8 billion, a significant beat of 13.7% above market estimates.

The core story of the SUNG KWANG BEND Q3 2025 earnings is a classic conflict: robust top-line growth overshadowed by margin pressure. While strong sales indicate healthy demand, the dip in operating profit signals underlying cost challenges that investors must carefully evaluate.

In-Depth Analysis: Behind the Numbers

Robust Revenue Driven by Core Industries

The revenue of KRW 64.6 billion is a clear positive, representing a continued growth trajectory from previous quarters. This strength suggests that the company’s fundamentals are solid and that demand from its key downstream industries, such as shipbuilding and LNG plant construction, is recovering. This top-line performance indicates a healthy order book and effective market positioning, which is a crucial pillar for any positive investor outlook.

What Dragged Down Operating Profit?

The slight miss in operating profit is primarily attributed to two key factors: volatile conditions in front-line industries and, more critically, rising raw material costs. As a manufacturer of industrial fittings, SUNG KWANG BEND is heavily reliant on steel and other alloys. Recent global supply chain disruptions and inflationary pressures have likely increased these input costs, squeezing profit margins. This challenge to company profitability highlights the importance of cost management and pricing power in the current economic climate.

The Net Profit Rebound Explained

The impressive 13.7% beat on net profit, despite the operating profit miss, suggests favorable non-operating factors. This could include gains from foreign exchange translations, income from financial assets, or a lower-than-expected corporate tax burden. While positive for the bottom line, investors should view this as a one-off or non-recurring benefit until proven otherwise, keeping the focus on the core operational performance.

Financial Health and Strategic Outlook

The company’s stable financial structure, characterized by a low debt-to-equity ratio, provides a strong foundation. This financial prudence enhances its resilience against market shocks and provides flexibility for future investments. Historically, the company’s performance, as seen in our previous quarterly reviews, has been tied to cyclical industries. However, a strategic investment in solar power signals a forward-thinking approach. This move not only strengthens its ESG credentials but also aims to diversify revenue streams and secure long-term growth momentum, reducing its dependence on traditional sectors.

Investor’s Corner: Stock Impact and Future Path

So, how will the SUNG KWANG BEND Q3 2025 earnings affect the stock? In the short term, the market’s reaction will likely be mixed. The positive revenue and net profit figures may be counterbalanced by concerns over profitability. The stock, which has historically traded in a range, will likely experience some volatility as investors digest these conflicting signals.

Positive and Negative Factors to Consider

- •Positives: The company boasts a stable market position, growing orders from recovering shipbuilding and LNG sectors, and long-term growth potential from its solar venture. A history of shareholder-friendly policies like dividends and buybacks adds to its appeal.

- •Negatives: Key risks include high sensitivity to industry cycles, profitability erosion from raw material and currency volatility, and a relatively high inventory burden that could tie up capital.

Action Plan: A Prudent Investment Thesis

The Q3 2025 results signal a fundamental recovery in demand but also highlight persistent margin challenges. A wise investment approach requires continuous monitoring of key external trends, such as global macroeconomic indicators discussed by sources like Reuters, and internal company efforts. Investors should focus on the company’s ability to manage costs, the pace of recovery in its core industries, and the tangible progress of its solar business. While SUNG KWANG BEND showcases potential, a long-term perspective that weighs both its intrinsic value and growth prospects against the prevailing risks is essential for success.