The latest HD Korea Shipbuilding earnings report for Q3 2025 has sent ripples through the market, showcasing a remarkable operating profit that sailed past analyst expectations. For investors tracking HD KOREA SHIPBUILDING & OFFSHORE ENGINEERING CO., LTD. (HD KSOE), this performance confirms the company’s strong market position but also raises important questions about its net profitability and future headwinds. This comprehensive analysis will dissect the financial results, explore the core drivers behind the success, and provide a forward-looking perspective on the HD KSOE stock analysis and the broader shipbuilding industry trends.

Q3 2025 Earnings Report: The Official Numbers

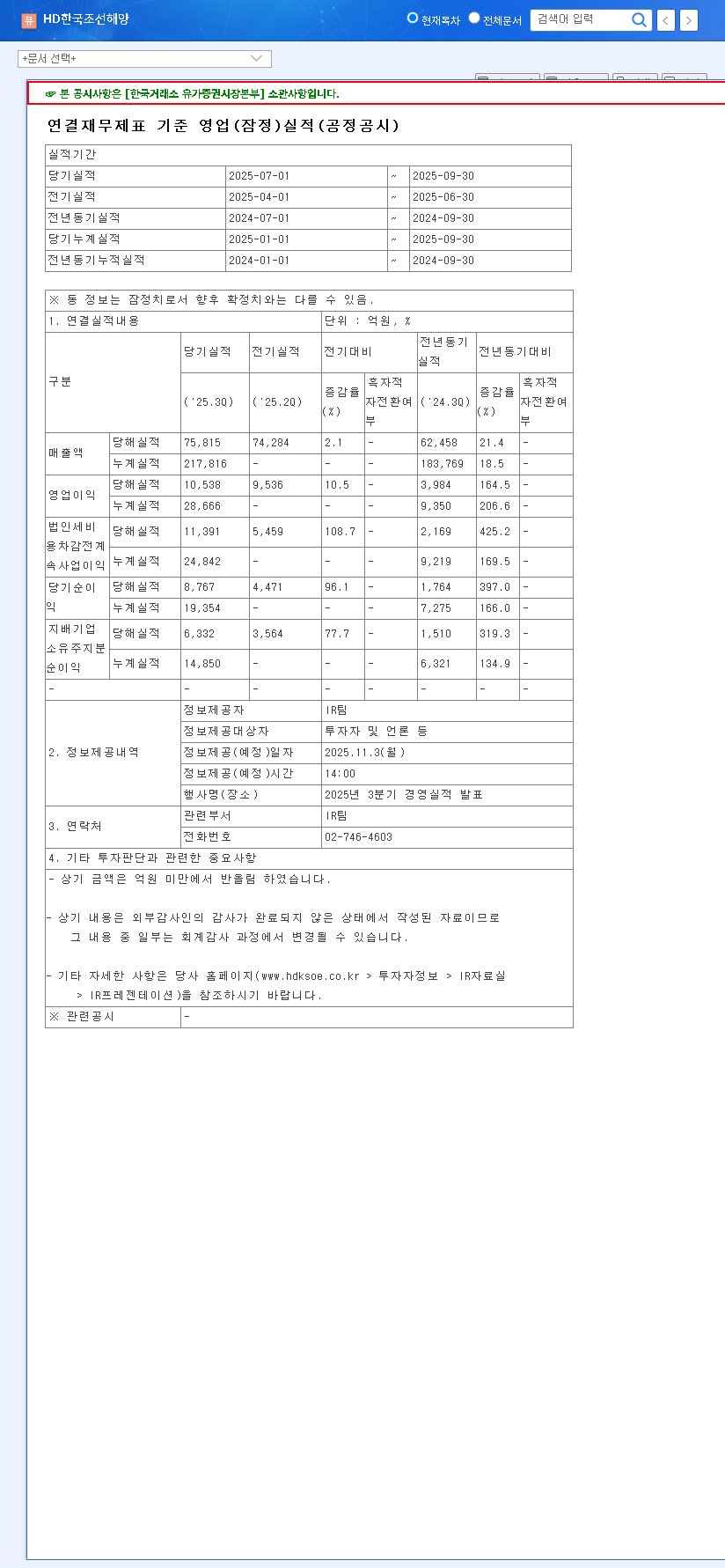

On November 3, 2025, HD KSOE released its preliminary consolidated financial statements, revealing a performance that largely outpaced market consensus. The figures highlight a company firing on all cylinders in its core operations, even as other factors weighed on the bottom line. The full details can be verified in the company’s Official Disclosure (DART).

- •Revenue: KRW 7.5815 trillion, a solid 6% above the market expectation of KRW 7.1198 trillion.

- •Operating Profit: KRW 1.0538 trillion, a massive 13% beat on the KRW 932.6 billion forecast, marking a significant earnings surprise.

- •Net Profit: KRW 633.2 billion, which fell 9% short of the KRW 693 billion consensus.

This mixed-signal report—stellar operational performance contrasted with a net profit miss—requires a deeper look into the underlying factors shaping the company’s financial health.

Behind the Surge: Why Operating Profit Excelled

The impressive operating profit wasn’t an accident; it was the result of strategic positioning and favorable market dynamics. The key drivers cementing HD KSOE’s leadership include:

Dominance in High-Value, Eco-Friendly Vessels

A significant portion of the success comes from the company’s focus on high-margin, technologically advanced ships. With global shipping regulations tightening under frameworks like the International Maritime Organization (IMO), the demand for vessels powered by LNG, methanol, and other dual-fuel technologies has skyrocketed. HD KSOE’s strong order backlog for these eco-friendly ships (over 50% of orders) not only boosts revenue but also enhances profit margins compared to standard vessels.

Operational Efficiency and Cost Management

Improved construction processes and stabilized prices for key raw materials, like steel plates, have helped control costs. This operational discipline allows the company to convert its strong revenue growth directly into higher operating profit, demonstrating a robust and efficient production pipeline.

The Q3 report paints a clear picture: HD KSOE’s core shipbuilding operation is a well-oiled machine, capitalizing on the green shipping revolution. However, the net profit figure reminds investors that external financial variables can still create turbulence.

Analyzing the Net Profit Shortfall

While the operating performance was a clear win, the net profit miss warrants careful consideration. This discrepancy was primarily driven by non-operating factors that don’t reflect the health of the core business but impact the final bottom line. These included:

- •Increased Corporate Tax Expenses: Higher profits naturally lead to a larger tax burden.

- •Foreign Exchange Volatility: As a global exporter, fluctuations in the KRW/USD and KRW/EUR exchange rates can create gains or losses on foreign currency holdings and transactions.

- •Non-Operating Costs: Other miscellaneous costs outside of the primary shipbuilding activities also played a role.

Investor Outlook: HD KSOE Stock Analysis

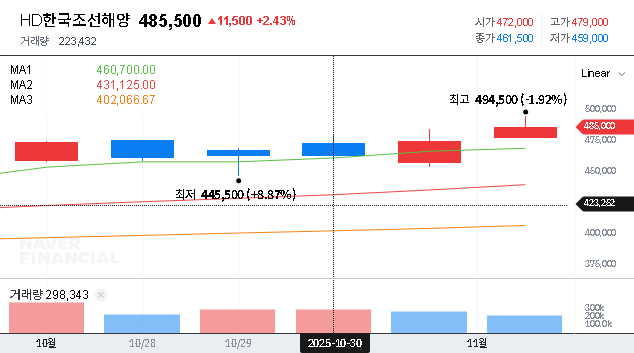

For those evaluating an investment in HD KSOE, it’s crucial to balance the short-term market reaction with the long-term fundamentals. The positive HD Korea Shipbuilding earnings surprise is likely to provide immediate upward momentum for the stock price.

Medium-to-Long-Term Growth Drivers

The company’s future looks promising, underpinned by a global shipbuilding market recovery and its technological edge. Continuing innovation in areas like SMR-powered container ships and hydrogen carriers positions HD KSOE as a key player in the next generation of maritime technology. This aligns perfectly with long-term shipbuilding industry trends. For more on this sector, see our guide to investing in the global shipbuilding industry.

Potential Risks to Monitor

However, investors must remain vigilant. Macroeconomic uncertainties could temporarily slow new ship orders. Furthermore, intensified competition from Chinese shipbuilders and the impact of geopolitical risks on global trade and energy prices are persistent threats. The company’s ability to manage currency and raw material price volatility through hedging and other financial instruments will be key to sustaining profitability.

Conclusion: A Resilient Leader with Manageable Risks

HD KOREA SHIPBUILDING & OFFSHORE ENGINEERING CO., LTD. has demonstrated exceptional operational strength in Q3 2025. The earnings surprise reaffirms its market leadership and its successful pivot towards high-value, eco-friendly vessels. While the net profit miss highlights the impact of external financial factors, the company’s fundamental health appears robust. Investors should weigh the strong growth prospects against macroeconomic risks to make an informed decision, recognizing that HD KSOE is well-positioned to navigate the future of global shipbuilding.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made at the investor’s sole discretion after consulting with a financial professional.