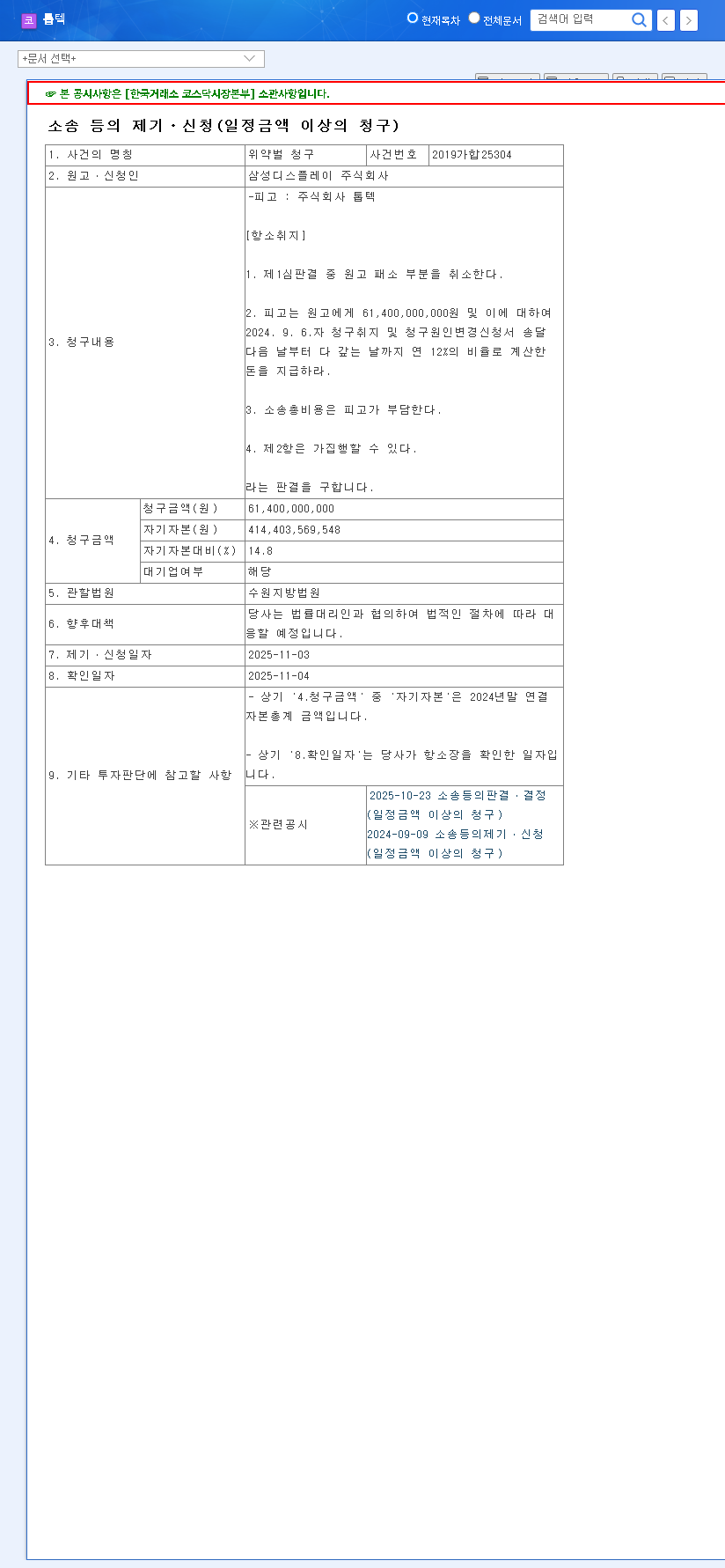

On November 4, 2025, a significant legal challenge emerged for TOPTEC COMPANY,LIMITED, sending ripples through the investor community. The core of this challenge is the TOPTEC lawsuit filed by industry giant Samsung Display Co., Ltd., which involves a staggering KRW 61.4 billion penalty claim. This figure is not trivial; it represents a substantial 14.8% of TOPTEC’s entire asset base, raising critical questions about the company’s financial stability, its stock performance, and its long-term strategic direction. This analysis will delve deep into the specifics of the lawsuit, evaluate TOPTEC’s current fundamentals, and provide a strategic guide for investors navigating this period of heightened uncertainty.

The Heart of the Matter: Samsung Display’s KRW 61.4 Billion Claim

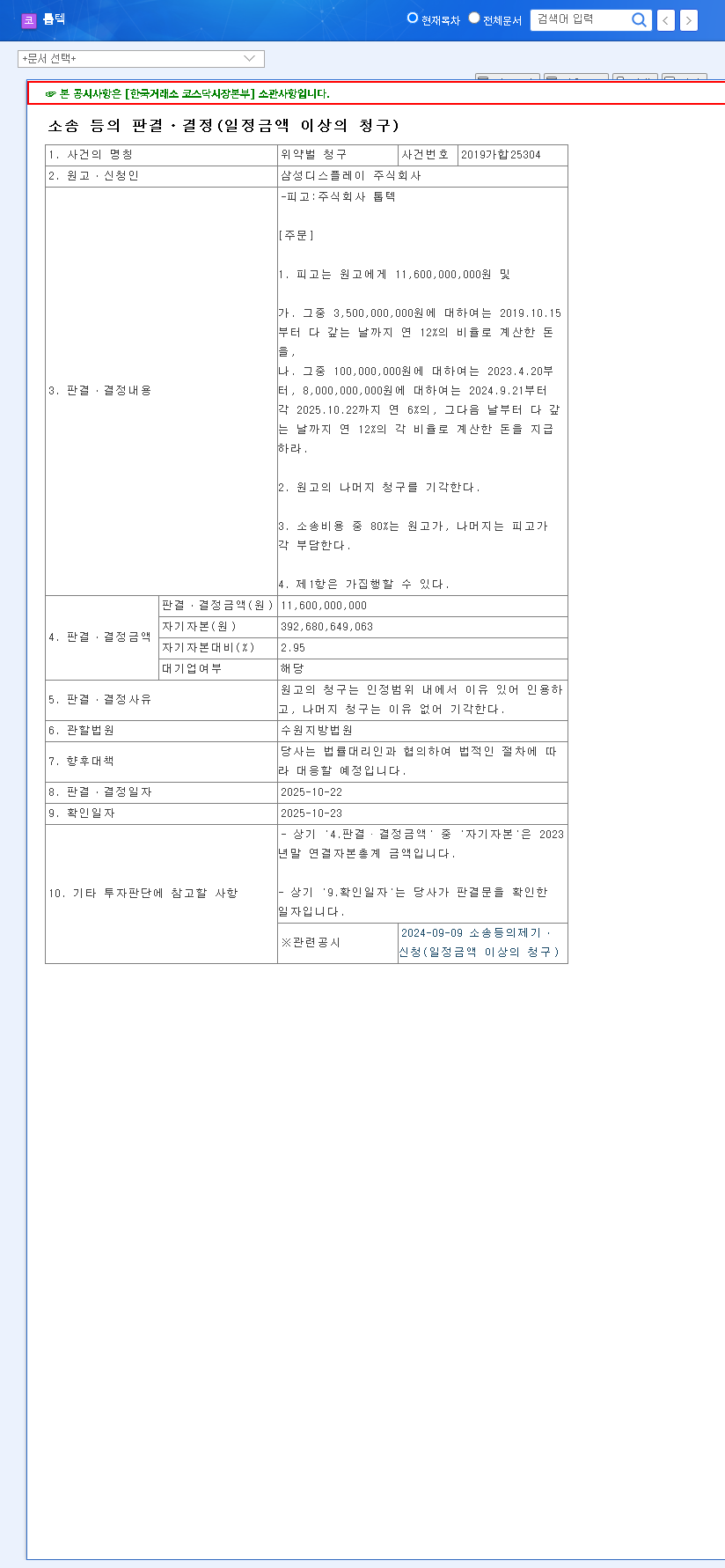

The legal action, officially titled a ‘Claim for Penalty’, was filed by Samsung Display with the Suwon District Court. The claim seeks to overturn a portion of a first-instance judgment and enforce the massive KRW 61.4 billion penalty, plus an annual interest rate of 12%. The details of this legal action were made public through an Official Disclosure on the DART system. TOPTEC has publicly stated its intention to mount a robust legal defense in consultation with its legal representatives. Understanding the gravity of this TOPTEC lawsuit is the first step for any stakeholder.

This legal battle pits TOPTEC against a key client, Samsung Display, creating a perfect storm of financial risk, operational uncertainty, and damaged investor confidence that could define the company’s trajectory for years to come.

Analyzing TOPTEC’s Fundamentals Amidst Crisis

To understand the potential fallout, we must look at TOPTEC’s fundamentals. The company presents a mixed but compelling picture of strengths and weaknesses that this lawsuit brings into sharp focus.

Struggles in the Core FA Division

The Factory Automation (FA) division, historically a cornerstone of TOPTEC’s business, has faced significant headwinds. In the first half of 2025, its sales plunged by nearly 80% year-on-year. This dramatic decline is a result of a global economic slowdown, reduced capital expenditure in the secondary battery and display sectors, and geopolitical tensions. A shrinking order backlog suggests this trend may continue, making the legal dispute with a major display client like Samsung Display even more perilous.

Bright Spots: Product Sales and New Ventures

Conversely, TOPTEC is demonstrating resilience and foresight in other areas. The development of PFAS-Free products using advanced nanofiber membranes and the expansion of its ‘AirQueen’ women’s hygiene brand are gaining traction. Furthermore, new business ventures into specialized construction and logistics automation signal a strategic pivot to diversify revenue and mitigate risks from the volatile FA sector. These initiatives are crucial for the company’s long-term health, especially now.

Potential Impact on TOPTEC Stock and Corporate Value

The consequences of this TOPTEC lawsuit could be severe and multi-faceted, directly affecting financials, stock performance, and business operations.

- •Crippling Financial Damage: If TOPTEC loses, the KRW 61.4 billion penalty far exceeds its projected 2025 net profit of KRW 32.6 billion. This would cause a massive non-operating loss, destroying profitability metrics for the year and potentially straining its otherwise sound financial structure.

- •Intense Pressure on TOPTEC Stock: News of a lawsuit this size is a major blow to investor sentiment. The market’s reaction is likely to be a sharp, short-term drop in TOPTEC stock price. The ongoing uncertainty will fuel volatility until a clear resolution is reached.

- •Long-Term Business and Reputational Risk: Beyond the financial hit, the lawsuit could erode trust with other key clients. The financial burden might also constrain crucial R&D and investment in growth areas, hindering the company’s ability to compete and innovate long-term.

Investor Action Plan: A Strategic Guide

For current and prospective investors, a cautious and informed approach is paramount. The situation demands careful monitoring of several key areas before making any decisions regarding TOPTEC stock.

- •Monitor Lawsuit Developments: Follow all official disclosures and news regarding the legal proceedings. The outcome will be the single largest catalyst for the stock’s future movement. For more context, investors can learn more about corporate litigation trends from authoritative legal journals.

- •Scrutinize Financial Reports: Pay close attention to quarterly earnings reports for any provisions set aside for the lawsuit, changes in cash flow, and updates on the company’s debt levels.

- •Evaluate Diversification Success: Track the revenue and profit growth from the product sales and new business divisions. Strong performance here could signal that TOPTEC can successfully pivot and absorb the potential impact of the lawsuit.

- •Follow Company Communications: Monitor TOPTEC’s investor relations (IR) activities. Transparent communication about their legal strategy and future vision is critical for rebuilding trust. Compare their strategy to our analysis of other tech manufacturing stocks facing challenges.

In conclusion, the TOPTEC lawsuit with Samsung Display is a watershed moment for the company. While its sound financial base provides a cushion, the sheer size of the KRW 61.4 billion penalty claim presents an undeniable threat. The outcome will heavily influence TOPTEC’s future, making diligent monitoring and a cautious investment strategy essential.