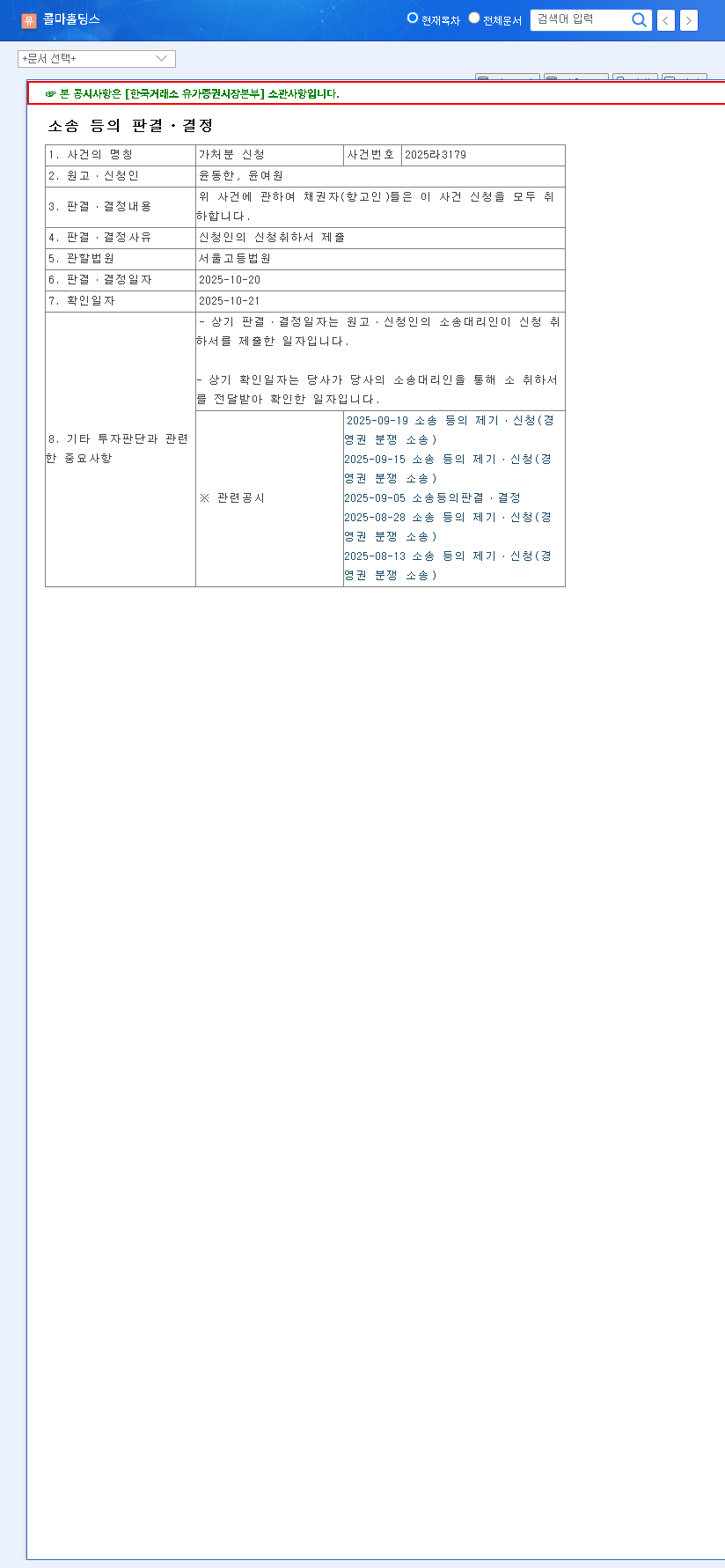

The recent announcement regarding the Sangsangin Co., Ltd. (038540) share disposal has sent ripples through the market. The company has confirmed its decision to sell a significant portion of its shares in the subsidiary, Sangsangin Savings Bank, amounting to ₩110.7 billion. This strategic move is not just a line item on a balance sheet; it represents a critical juncture for the company, poised between achieving much-needed financial stability and navigating persistent underlying risks. This comprehensive analysis will break down the event, its motivations, and the potential consequences for investors.

The Core Event: A ₩110.7 Billion Share Disposal

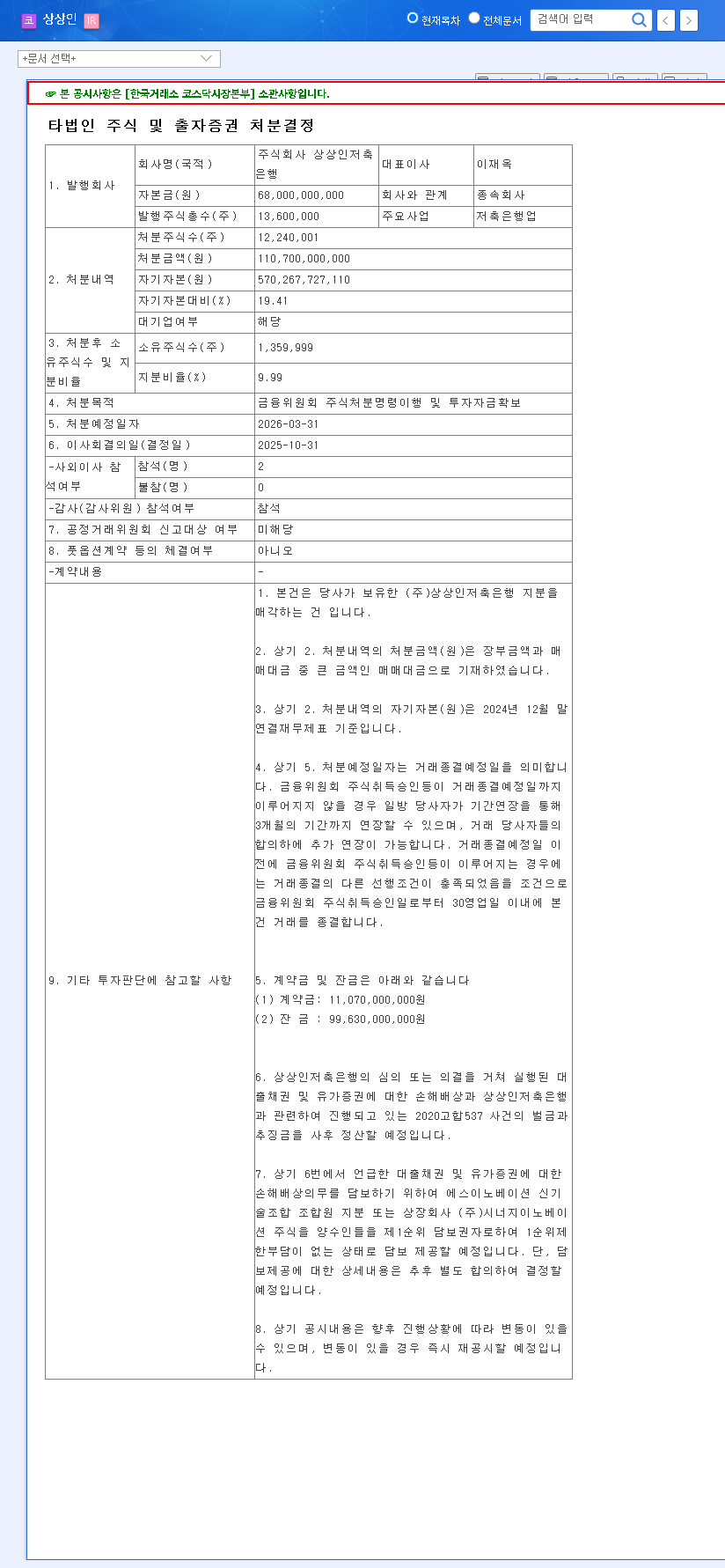

On October 31, 2025, Sangsangin Co., Ltd. formally announced its ‘Decision on Disposal of Shares and Equity Securities in Other Corporations.’ This decision directly involves its highly valuable subsidiary, Sangsangin Savings Bank. For complete transparency, you can view the Official Disclosure on the DART system.

Let’s look at the key details of this transaction:

- •Disposal Target: Shares held in subsidiary Sangsangin Savings Bank.

- •Disposal Value: ₩110.7 billion KRW (approximately 19.41% of capital).

- •Post-Disposal Ownership: Reduced to 9.99%.

- •Stated Purpose: Compliance with a Financial Services Commission (FSC) order and securing investment capital.

Why Now? The Dual Pressures of Finance and Regulation

This decision wasn’t made in a vacuum. Two primary forces are driving the Sangsangin share disposal strategy. Firstly, the company is grappling with a high consolidated debt ratio of 867.94%, a significant vulnerability. The infusion of ₩110.7 billion is a direct attempt to deleverage and fortify its financial foundation. Secondly, Sangsangin is acting under a mandate from the Financial Services Commission. Complying with this share disposal order is a necessary step to address and mitigate ongoing legal and regulatory risks, which have created uncertainty around the company’s management.

This share disposal is a calculated move to tackle two of Sangsangin’s biggest challenges simultaneously: shoring up a weak balance sheet and demonstrating compliance to regulators.

Analyzing the Ripple Effects for Sangsangin Co., Ltd.

The consequences of this sale will be felt across the company’s operations, market perception, and long-term strategy. It’s a classic case of short-term relief versus potential long-term strategic shifts.

The Bull Case: A Leaner, More Focused Future

Optimists will point to the immediate financial benefits. The capital injection provides breathing room to manage debt and reinvest in promising areas, such as its new shipbuilding business. This segment could benefit from the global recovery in shipping, a trend noted by industry experts at authoritative sources like Bloomberg. By addressing the FSC’s order, the company removes a significant regulatory overhang, potentially improving investor sentiment and clarifying its path forward.

The Bear Case: Weakened Control and Lingering Doubts

Conversely, critics will argue that reducing ownership in a key subsidiary like Sangsangin Savings Bank weakens the company’s control over a historically important business segment. This could impact the overall financial portfolio and long-term earnings potential. Furthermore, while the disposal addresses one regulatory issue, it does not erase the underlying legal risks, including a first-instance guilty verdict against management. These issues will continue to weigh on the stock until a final resolution is reached.

Investor Takeaway: A Prudent and Cautious Outlook

For investors, the Sangsangin Co., Ltd. share disposal creates a complex picture. The move is a net positive for financial health in the short term, but it introduces questions about long-term strategy and does not fully resolve the legal uncertainties.

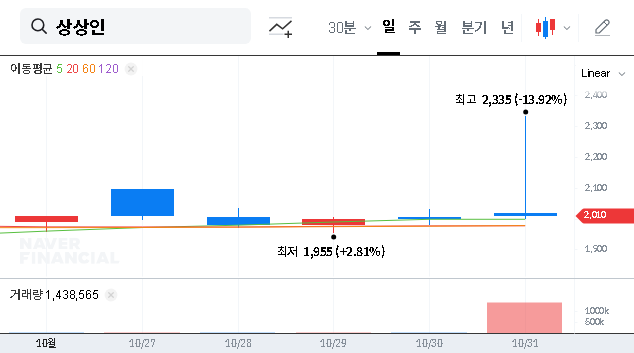

- •Short-Term (1-3 months): Expect continued volatility. Positive news about debt reduction may be offset by negative sentiment from the underlying legal risks.

- •Long-Term (6+ months): The company’s value will depend on three critical factors: the final outcome of legal proceedings, the performance and recovery of its remaining financial assets, and tangible success from its diversification into the shipbuilding industry. For more on this sector, see our in-depth analysis of the Korean shipbuilding market.

In conclusion, a conservative and watchful approach is recommended. While the disposal is a proactive step towards solving major issues, the path to a full recovery for Sangsangin Co., Ltd. is still fraught with significant variables that require careful monitoring.

Frequently Asked Questions

Q1: What are the main reasons for the Sangsangin share disposal?

A1: The two primary drivers are to comply with a share disposal order from the Financial Services Commission (FSC) and to raise ₩110.7 billion in capital to significantly reduce its high debt ratio and improve its financial structure.

Q2: How does this sale impact Sangsangin’s financial health?

A2: The capital infusion is expected to have a direct positive effect by lowering the company’s consolidated debt ratio from 867.94% and strengthening its overall financial stability.

Q3: What are the key long-term factors for investors to watch?

A3: Long-term success hinges on the complete resolution of its legal challenges, the health and profitability of its remaining financial businesses, and whether its new venture into the shipbuilding industry can generate substantial returns.