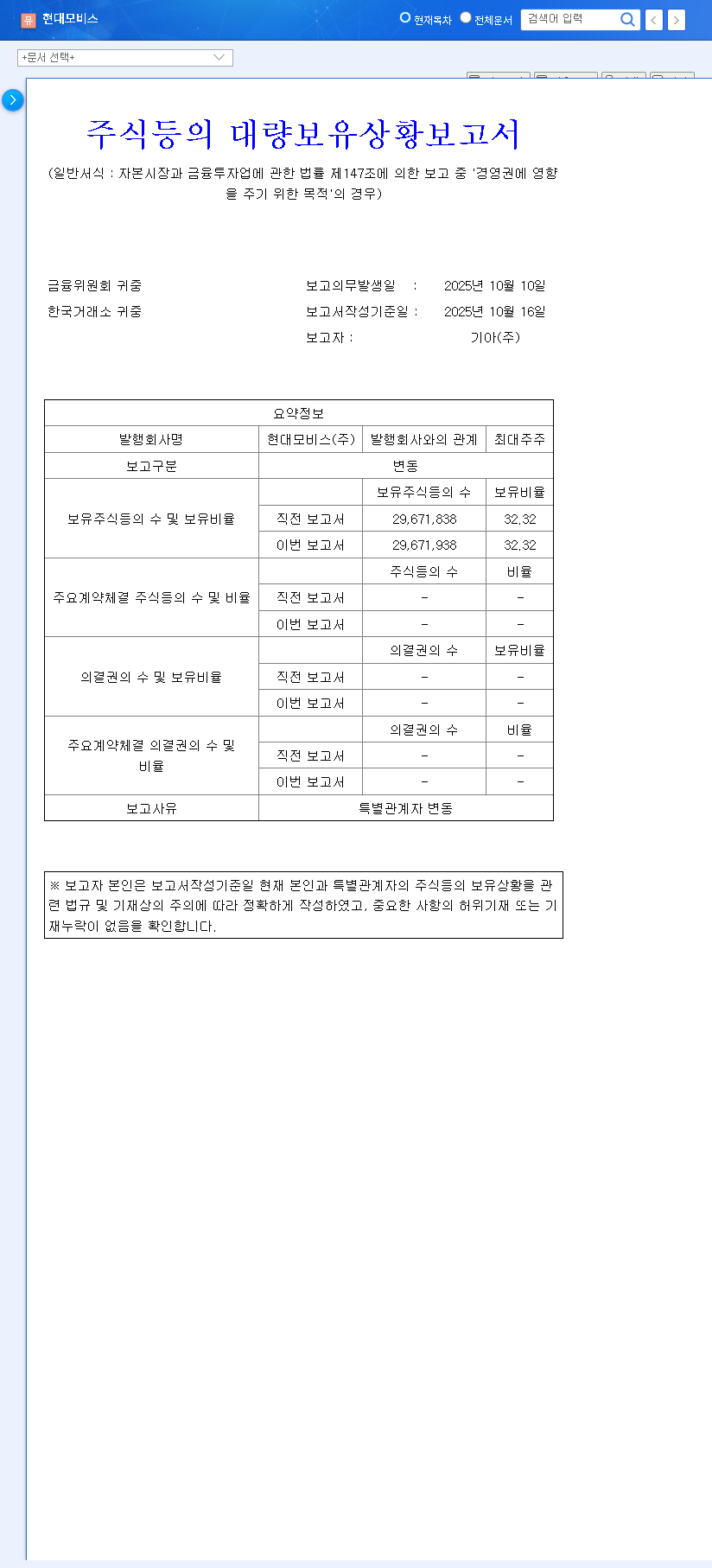

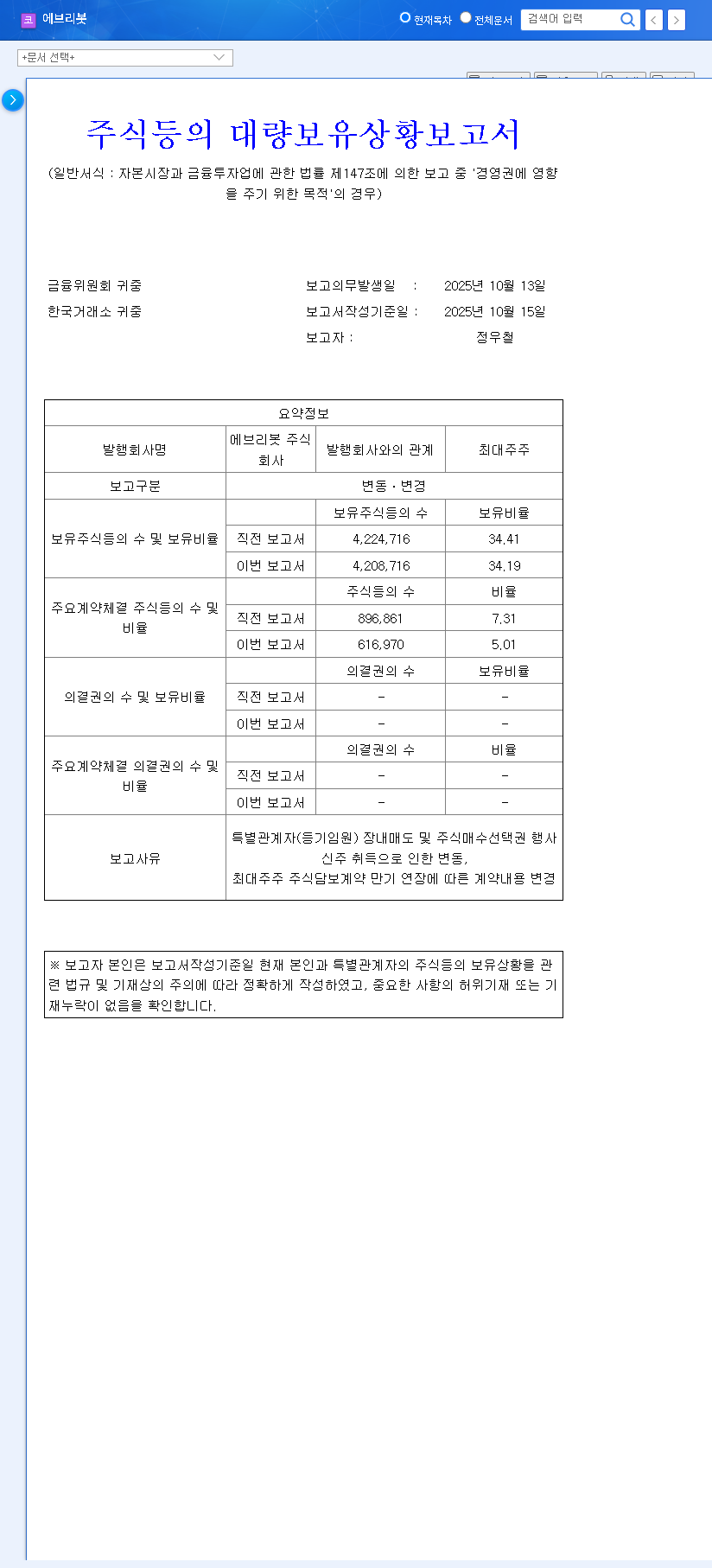

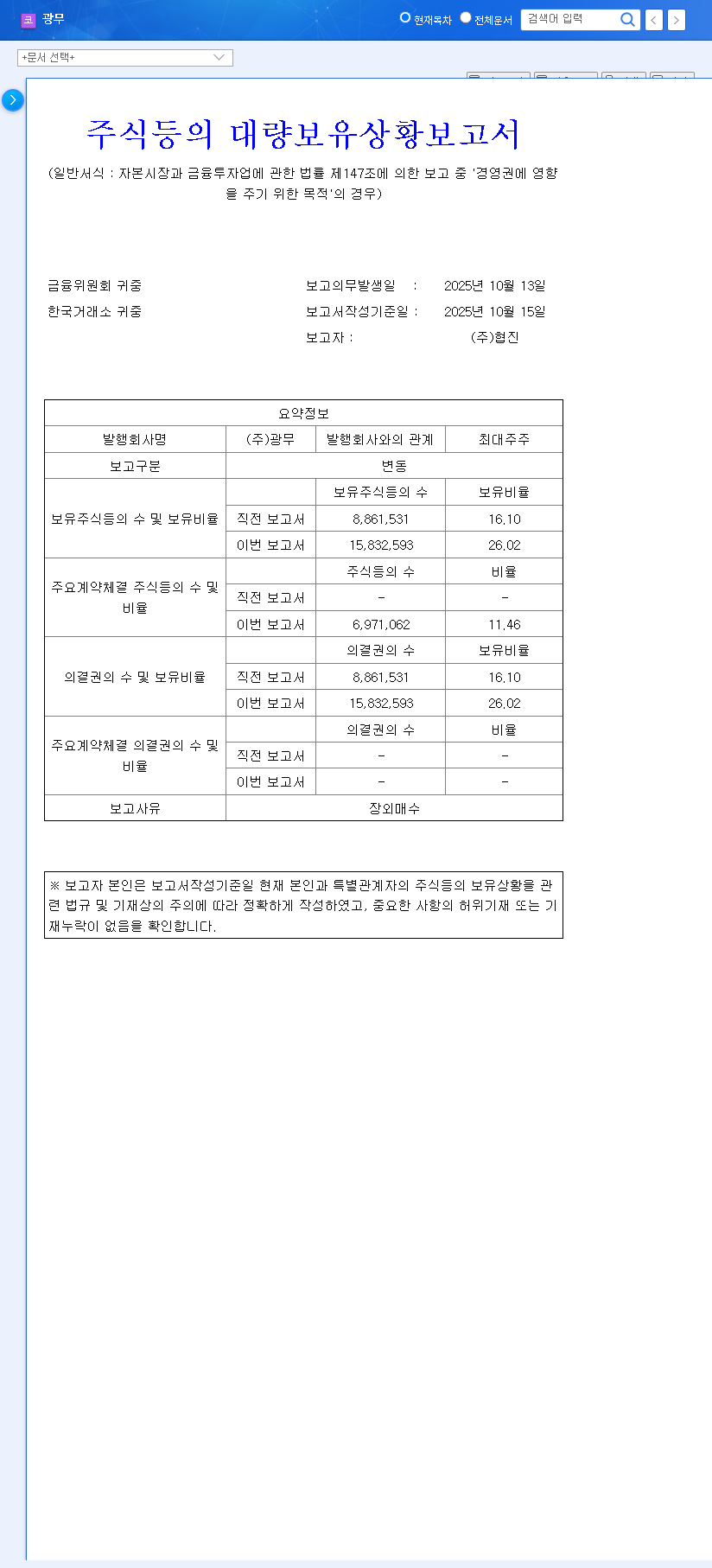

The HeunguOil stock price is currently under intense scrutiny from the investment community. A recent disclosure revealed a significant stock sale by a major shareholder, coinciding with the company’s troubling shift to an operating loss in its H1 2025 earnings report. This combination of events has created a perfect storm of uncertainty, leaving many investors wondering about the future trajectory of this leading Korean oil distribution company.

This comprehensive HeunguOil financial analysis will dissect the shareholder’s move, evaluate the company’s deteriorating fundamentals, and assess the broader market environment to provide a clear, actionable investment strategy. Is this a temporary dip or a sign of deeper structural issues? Let’s find out.

The Catalyst: Major Shareholder Discloses Stake Reduction

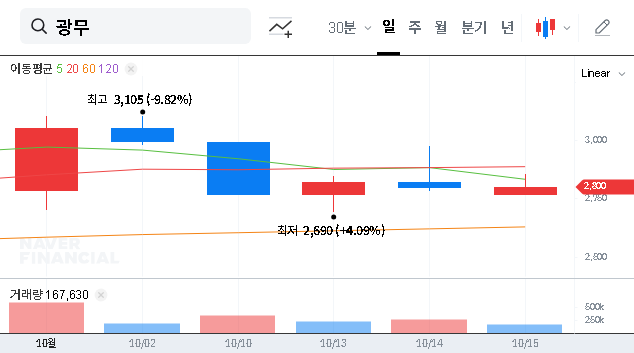

On October 24, 2025, a mandatory disclosure sent ripples through the market. HeunguOil announced that major shareholder Mr. Seo Sang-deok had reduced his holdings. The transaction, executed via open market sales, saw his stake decrease from 20.73% to 20.33%—a seemingly small but symbolically significant 0.4%p reduction. The stated reason was the ‘dissolution of special relationship and change in holding purpose’.

When a long-term, major shareholder sells, it often signals a lack of confidence in the company’s near-term prospects. This action, coupled with the official reasoning, raises critical questions about the company’s internal stability and future direction. The full Official Disclosure can be viewed on the DART system, providing transparent data on the transaction.

Diagnosing HeunguOil’s Financial Health

The shareholder sale isn’t happening in a vacuum. It’s set against a backdrop of weakening corporate fundamentals, making this HeunguOil investment case particularly challenging.

1. The Alarming Shift to Unprofitability

For the first half of 2025, HeunguOil’s performance took a nosedive. Revenue fell by 7.8% year-over-year, but more alarmingly, the company swung from profit to an operating loss of KRW 980 million and a net loss of KRW 380 million. This transition to unprofitability is a major red flag for investors who rely on consistent earnings.

2. Operational Headwinds and Cash Flow Concerns

The problems extend beyond the top line. The company’s inventory turnover ratio plummeted from 41.50 to just 19.28 times. This indicates that products are sitting in storage for much longer, tying up capital and suggesting a severe sales slowdown. Compounding this issue, operating cash flow was a negative KRW 7.26 billion, meaning the core business is burning through cash instead of generating it—an unsustainable situation. For more on how to interpret these metrics, review our guide to fundamental analysis.

3. The Silver Lining: A Strong Balance Sheet

Despite the grim operational picture, HeunguOil maintains a robust financial structure. Its debt-to-equity ratio is an impressively low 17.17%, and it holds substantial tangible assets and investment properties. This strong balance sheet provides a cushion and some resilience, but it cannot indefinitely mask poor operational performance.

HeunguOil is currently facing a ‘triple whammy’: deteriorating performance, a challenging macroeconomic environment, and wavering confidence from a major HeunguOil shareholder. This combination is likely to exert significant downward pressure on the stock price in the short term.

Market Volatility and External Pressures

HeunguOil’s internal struggles are amplified by external factors. As an oil importer and distributor, the company is highly sensitive to macroeconomic trends.

- •Exchange Rate Risk: The rising KRW/USD and KRW/EUR exchange rates directly increase the cost of importing raw materials, squeezing profit margins.

- •Oil Price Fluctuations: International oil prices have been volatile, making cost management difficult. According to data from the U.S. Energy Information Administration (EIA), prices fluctuated significantly in H1 2025, directly impacting HeunguOil’s cost of goods sold.

- •Limited Monetary Policy Benefit: While global interest rates are stabilizing, the positive impact on HeunguOil is minimal due to its already low debt load.

Investor Action Plan: How to Approach HeunguOil Stock

Given the confluence of negative factors, a cautious and disciplined approach to investing in HeunguOil stock is paramount. At this juncture, the risks appear to outweigh the potential rewards.

Key Monitoring Points:

- •Performance Turnaround: Watch for a return to positive operating cash flow and profitability in subsequent quarterly reports.

- •Strategic Initiatives: Monitor company announcements for new business strategies, such as cost-cutting measures or diversification into alternative energy, that could signal a new growth phase.

- •Shareholder Movements: Keep a close eye on any further stake changes from Mr. Seo Sang-deok or other major institutional holders.

In conclusion, our current investment recommendation for HeunguOil is ‘Hold’ or ‘Cautious Approach.’ The company’s solid asset base is a positive, but until there is clear evidence of a fundamental business turnaround, the investment appeal remains low. Prudence dictates waiting for confirmation of improved market conditions and internal corporate changes before committing new capital.