The latest KT Corporation earnings announcement for Q3 2025 has sent significant ripples through the investment community. As a cornerstone of the Korea telecommunications industry, the company reported preliminary figures that fell dramatically short of market consensus, triggering what is being widely described as a significant KT earnings shock. For investors holding or watching KT stock, this raises critical questions about the company’s current health and future trajectory. This comprehensive analysis will dissect the Q3 2025 results, explore the underlying causes for the underperformance, and provide a clear-eyed view on what this means for your investment strategy.

Anatomy of the Q3 2025 KT Earnings Shock

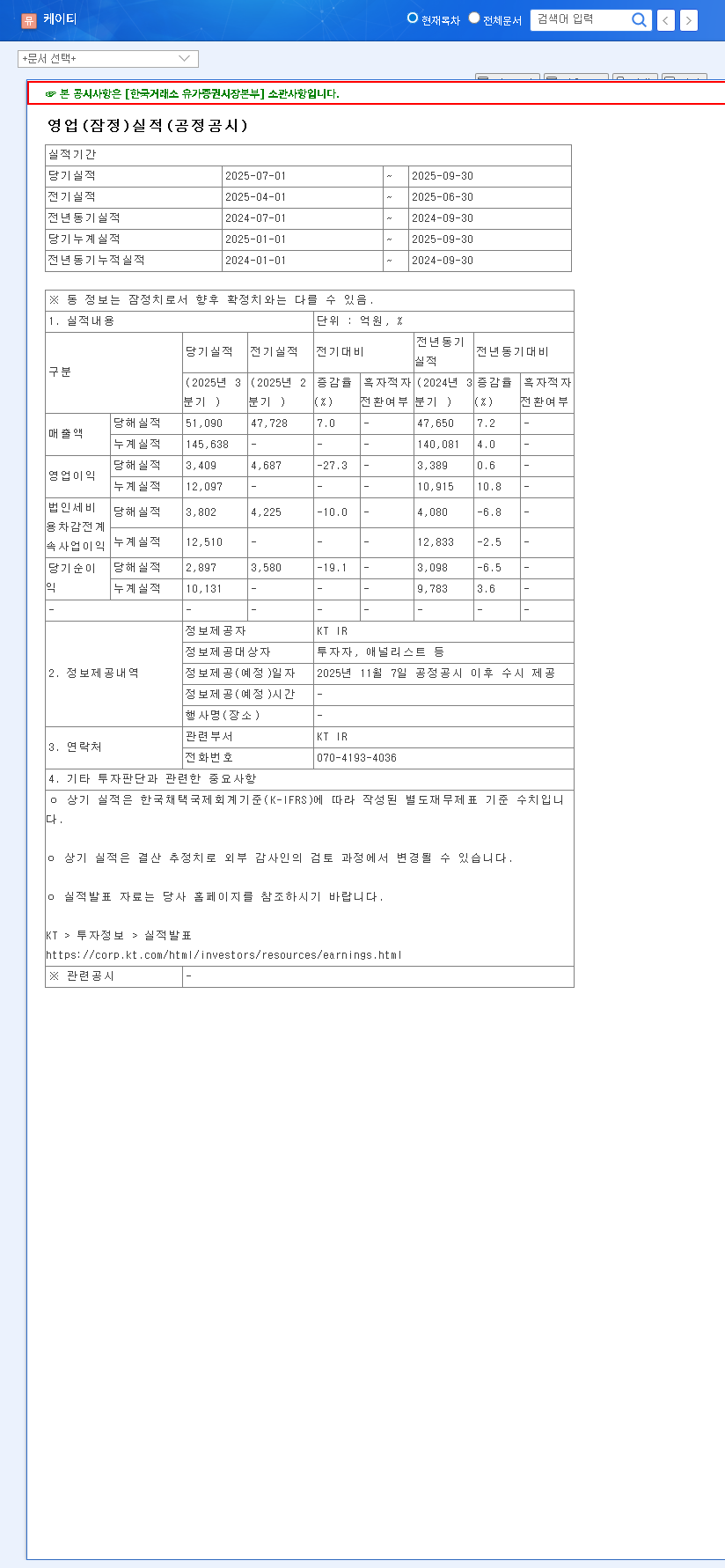

On November 7, 2025, KT Corporation released its preliminary Q3 operating results, which immediately raised alarms. The figures, confirmed in their Official Disclosure, revealed a stark disconnect between expectations and reality.

- •Revenue: 5.109 trillion KRW, a staggering 26.0% below the market forecast of 6.9127 trillion KRW.

- •Operating Profit: 340.9 billion KRW, missing expectations of 513 billion KRW by 33.9%.

- •Net Income: 289.7 billion KRW, which was 26.9% lower than the anticipated 395 billion KRW.

A revenue miss of over 25% isn’t merely a quarterly dip; it’s a significant deviation that signals potential underlying challenges in core operations, competitive positioning, or the delayed monetization of new ventures.

Unpacking the Causes: Why Did KT Falter?

This underperformance isn’t the result of a single factor but rather a convergence of internal and external pressures. A thorough KT stock analysis requires understanding these multifaceted issues.

The AICT Transformation Dilemma

KT is aggressively pivoting to become an ‘AICT’ (AI + ICT) company. This involves heavy investment in future growth engines like AI, 6G, cloud services, and Urban Air Mobility (UAM). While strategically sound for the long term, these ventures are capital-intensive and have not yet reached a scale where they can offset weaknesses in the legacy telecom business. The short-term result is a strain on profitability without immediate, corresponding revenue growth, a key factor in the recent KT Corporation earnings report.

Core Business Headwinds & Competition

The traditional telecommunications market is mature and fiercely competitive. KT faces constant pressure from rivals, leading to price wars and high marketing costs. Furthermore, ongoing litigation related to 5G service quality not only poses a financial risk but also damages brand reputation. These factors create a challenging environment for revenue growth in their primary business segment, a topic we explore further in our analysis of the 5G market in South Korea.

Macroeconomic Pressures

Global economic uncertainty also plays a role. As noted by leading financial analysts at sources like Bloomberg, fluctuating interest rates can increase borrowing costs for a capital-intensive company like KT, impacting investment plans and margins. While the company engages in hedging, sustained high rates and volatile exchange rates create an unpredictable financial landscape that can suppress investor sentiment.

Investor Playbook: Navigating the Uncertainty

Given the sharp miss, our investment opinion on KT Corporation is a cautious ‘Neutral.’ The company is caught between a challenging present and a promising, but not yet realized, future. Investors should weigh the following points carefully.

Key Monitoring Points for a Turnaround

- •Q4 Guidance: The next earnings call is critical. Look for a clear explanation of the Q3 miss and a realistic, achievable guidance for Q4 and 2026.

- •AICT Monetization: Watch for tangible evidence that the AICT strategy is translating into revenue. This includes new major contracts for KT Cloud or successful launches of AI-based B2B services.

- •Cost Discipline: Investors need to see that management is exercising strong control over operational and capital expenditures to protect profit margins during this transitional period.

- •Subsidiary Performance: Monitor the growth of connected subsidiaries like KT Skylife, KT Alpha, and KT Genie Music. Strong performance from these units can help diversify revenue streams and cushion blows from the core telecom business.

In conclusion, while the KT Q3 2025 results are deeply concerning, the company’s fundamental strengths—a stable financial structure, a leading market position, and a forward-looking AICT strategy—should not be entirely discounted. The path to stock price recovery will depend on management’s ability to execute its strategy and deliver tangible results that rebuild investor confidence. Prudent investors should remain on the sidelines, closely monitoring for signs of a credible turnaround before committing new capital.