The upcoming HYBE Q3 2025 earnings report is poised to be a pivotal moment for investors and market analysts alike. As the global entertainment powerhouse, home to superstars like BTS and SEVENTEEN, prepares to unveil its third-quarter performance, all eyes are on whether it can sustain the positive momentum from its H1 2025 turnaround. This deep dive provides a critical HYBE stock analysis, exploring the key growth drivers, potential risks, and strategic questions that will define the company’s trajectory.

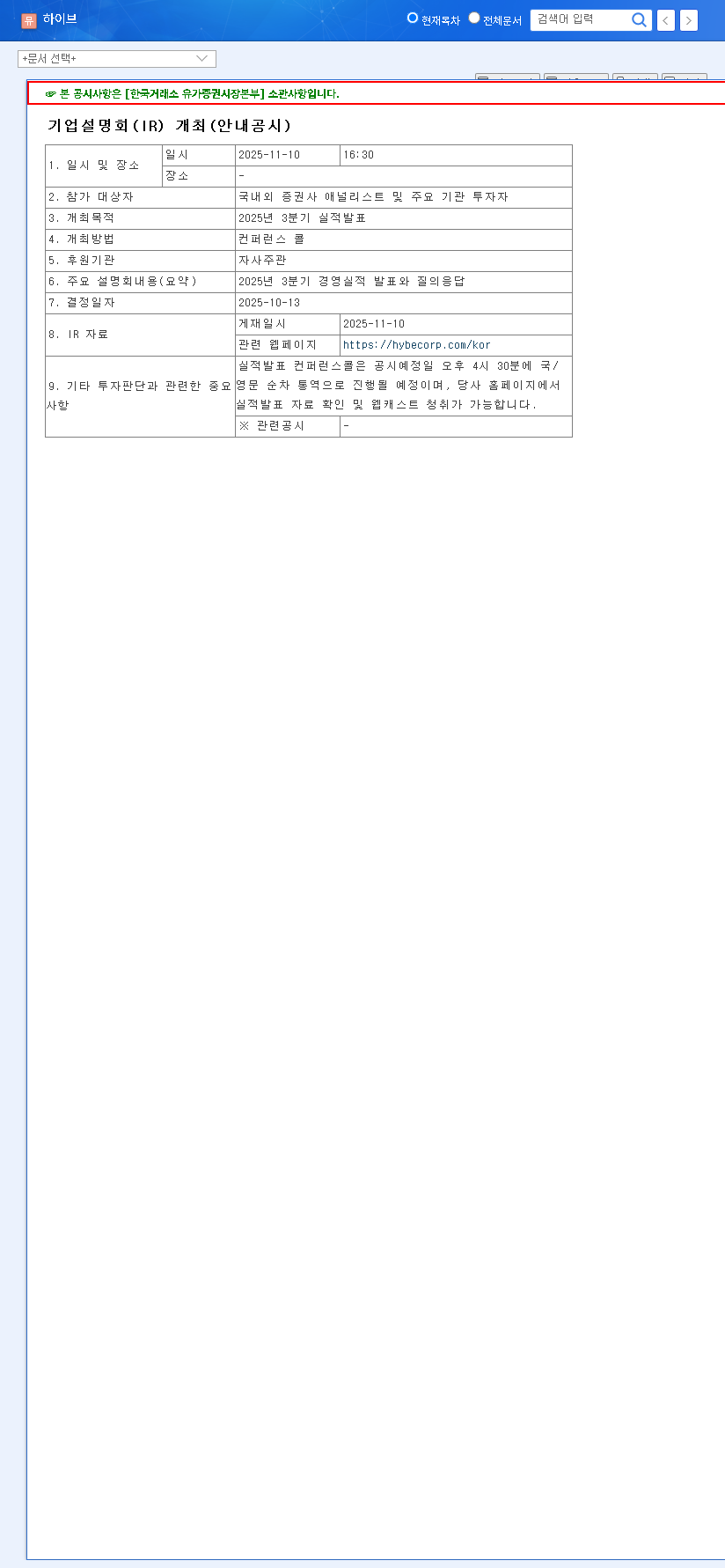

HYBE has officially scheduled its investor relations (IR) conference call to present the Q3 2025 results and host a Q&A session on November 10, 2025, at 4:30 PM KST. The announcement, available for public review in the Official Disclosure, sets the stage for a report that will offer crucial insights into the health of its diverse business segments.

Core Growth Engines Under the Microscope

The significance of the HYBE Q3 2025 earnings report lies in its ability to validate the company’s multi-pronged growth strategy. Investors will be scrutinizing three primary pillars of HYBE’s business model.

1. The Power of IP and Fandom Monetization

At its core, HYBE is an intellectual property (IP) giant. The consistent revenue from its artist roster, driven by a deeply loyal global fandom, is its biggest strength. This includes:

- •Album and Music Sales: Consistent high-volume sales from established acts and successful debuts from new groups.

- •Tours and Live Events: The return to full-scale global tours represents a massive revenue stream that directly impacts profitability.

- •Merchandise (MD) and Licensing: High-margin revenue generated from leveraging powerful artist brands across various products.

2. Weverse Platform: The Fan Economy Super-App

The Weverse growth trajectory is a key focus for long-term investors. More than just a fan community app, Weverse is evolving into an integrated ecosystem for content, commerce, and communication. The Q3 report should provide updates on user acquisition, engagement metrics, and the platform’s success in onboarding third-party artists, which is crucial for scaling. For a deeper look, you can read our guide on The Future of the Weverse Ecosystem.

Weverse’s ability to lock in fans and create new monetization channels is central to HYBE’s strategy of reducing dependency on the cyclical nature of album releases and tours. Its performance is a bellwether for HYBE’s future valuation.

3. Global Expansion and M&A Synergy

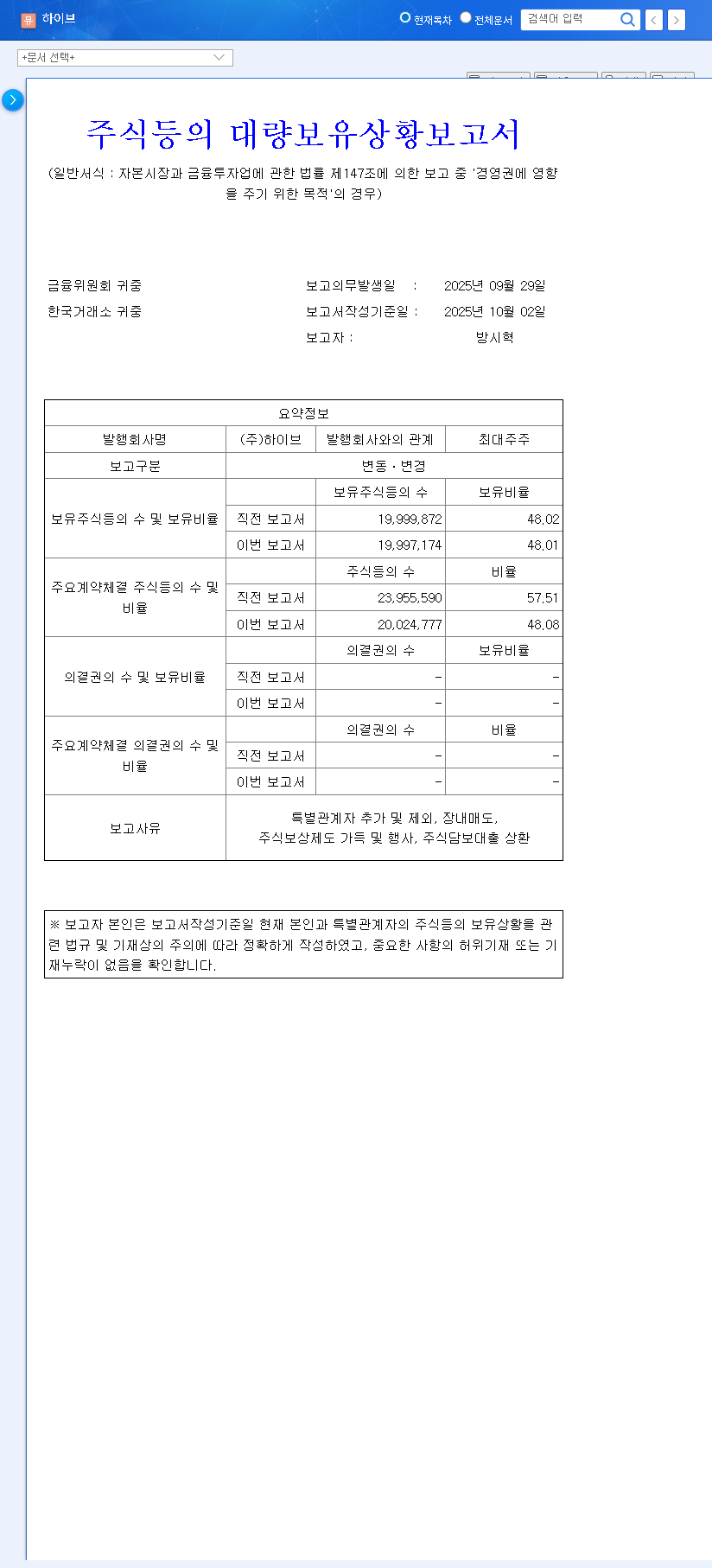

HYBE’s acquisition of Ithaca Holdings and the establishment of various overseas subsidiaries marked a bold move into the global market. The HYBE financial report for Q3 will be the latest test of this strategy. Investors will want to see tangible evidence of synergy, such as successful global projects for existing K-pop acts and the performance of international artists under the HYBE America umbrella. This expansion is critical for de-risking and tapping into larger, more mature markets.

Financials and Future Scenarios: What to Expect

After turning a net loss in 2024 into a significant net profit in the first half of 2025, maintaining profitability is paramount. The Q3 numbers will be compared not only to the previous year but also to the market consensus estimates compiled by sources like Bloomberg.

Positive Scenario (Bull Case)

A strong upward move in HYBE’s stock could be triggered if the company reports earnings and revenue that beat expectations. Key catalysts would include higher-than-anticipated album sales, robust growth in Weverse’s monthly active users (MAUs), and positive forward guidance for Q4 and 2026. A clear, detailed roadmap for new ventures in gaming or AI would further boost investor confidence.

Potential Risks (Bear Case)

Conversely, the stock could face short-term pressure if the HYBE Q3 2025 earnings fall short of forecasts. Potential headwinds include macroeconomic factors like currency fluctuations impacting overseas profits, rising operational costs, or slower-than-expected progress in monetizing new business segments. Any ambiguity regarding artist contract renewals or future activity schedules could also introduce uncertainty.

Investor Action Plan for the IR Call

Beyond the headline numbers, seasoned investors should listen closely during the Q&A session for management’s tone and strategic priorities. Key areas to focus on include:

- •Profitability Margins: Is the H1 2025 profitability trend sustainable? Look for details on operating margins across different segments.

- •New Artist Pipeline: What is the status of upcoming debuts? New groups are vital for long-term, sustainable IP generation.

- •Capital Allocation: How does management plan to deploy its cash reserves? Are further M&A activities or increased R&D investments planned?

In conclusion, the HYBE Q3 2025 earnings call is far more than a simple financial update. It’s a critical stress test of the company’s ambitious vision. A report that demonstrates strong execution, clear strategic direction, and sustained profitability could solidify its position as a top-tier global entertainment investment. Conversely, any signs of weakness could invite a period of cautious reassessment from the market.