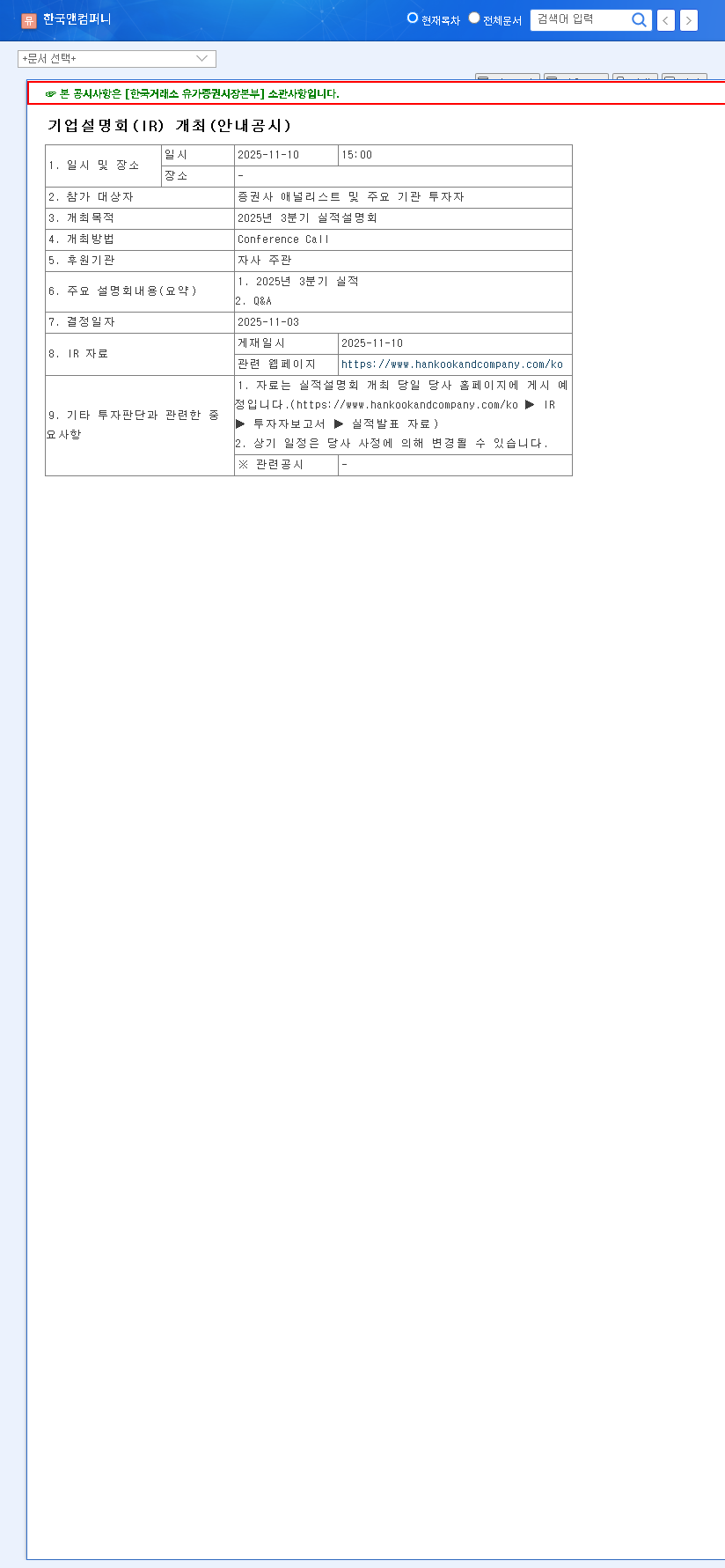

The upcoming HANKOOK & COMPANY Q3 Earnings Call, scheduled for November 10, 2025, represents a critical juncture for investors. This event is more than a routine financial report; it’s a pivotal moment that will shed light on the company’s ability to navigate persistent profitability challenges and sustain its recent revenue recovery. For stakeholders, this call will be the primary source for gauging the firm’s future trajectory and the stability of its management strategy.

This comprehensive analysis dissects the key variables at play, offering deep insights into the company’s fundamental health, the potential market impact of the earnings release, and an actionable roadmap for both short-term and long-term investors. We will explore everything from financial performance metrics to the macroeconomic headwinds and tailwinds affecting HANKOOK & COMPANY’s stock analysis.

Event Details and What to Expect

Mark your calendars: HANKOOK & COMPANY will host its Q3 2025 Earnings Call (IR) on November 10, 2025, at 3:00 PM KST. The event will begin with a presentation of the third-quarter performance, followed by a crucial Q&A session with analysts and investors. For official confirmation and documentation, please refer to the company’s Official Disclosure on DART. The market will be listening intently for management’s commentary on future growth strategies and plans to address current financial weaknesses.

Core Financial Diagnosis: Strengths and Weaknesses

A thorough review of HANKOOK & COMPANY’s financials reveals a mixed picture. While there are green shoots of recovery in some areas, significant challenges remain that require urgent attention from leadership.

The central question for investors is whether the modest revenue recovery can translate into meaningful profitability improvements, especially given the company’s high debt load and declining capital efficiency.

Key Financial Metrics Under the Microscope

- •Revenue Trajectory: After a dip in 2023, revenue projections show a slow but steady recovery. The market anticipates confirmation of this trend in the Q3 report.

- •Profitability Crisis: Both operating and net income saw a significant decline in 2023 and are projected to remain low. This is the most pressing concern, and investors will demand a clear strategy for margin improvement.

- •Return on Equity (ROE): A dramatic fall from 19.11% in 2022 to a projected 1.23% in 2025 signals a severe drop in capital efficiency. This metric reflects how effectively the company is using shareholder equity to generate profits.

- •High Leverage: The debt-to-equity ratio remains at a high level, hovering around 270%. While manageable, this level of debt can limit financial flexibility and increase risk during economic downturns. For more on this, see our guide to understanding key financial ratios.

Macroeconomic and Management Factors

Beyond the balance sheet, external market forces and internal governance play a crucial role in HANKOOK & COMPANY’s performance. Recent changes in the boardroom, while potentially disruptive, could also signal a positive shift towards stronger governance and ESG focus.

External Economic Influences

- •Currency Fluctuations: As an export-heavy business, a rising USD/KRW exchange rate is beneficial. However, shifts in the EUR/KRW rate must be monitored for their impact on European market profitability.

- •Commodity Prices: Declining prices for key raw materials like lead and rubber can provide a significant cost advantage and boost margins, a topic often covered by sources like Bloomberg’s commodity index.

- •Interest Rate Environment: Rising global interest rates could increase borrowing costs, putting further pressure on the company’s already leveraged financial position.

Investor Action Plan & Final Outlook

The HANKOOK & COMPANY Q3 Earnings Call will likely trigger stock price volatility. A positive report that beats expectations and outlines a clear path to profitability could provide strong upward momentum. Conversely, a failure to address the core issues could lead to significant downward pressure.

Strategies Based on Investor Profile

For Short-Term & Active Traders: Pay close attention to whether the announced EPS and revenue figures meet, exceed, or fall short of analyst consensus. The management’s forward-looking guidance for Q4 and 2026 will be the primary catalyst for immediate price action.

For Mid-to-Long-Term Investors: Look beyond the headline numbers. Focus on the substance of the Q&A session. Are the strategies for improving margins credible? Are there concrete plans to deleverage the balance sheet? Is the new board composition leading to more robust long-term value creation? Your focus should be on the sustainability of the business model.

In conclusion, while HANKOOK & COMPANY shows signs of stabilizing revenue, its path forward is fraught with challenges. This earnings call is a crucial test of management’s ability to steer the company toward sustainable profitability and regain investor confidence.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made with the consultation of a qualified financial professional.