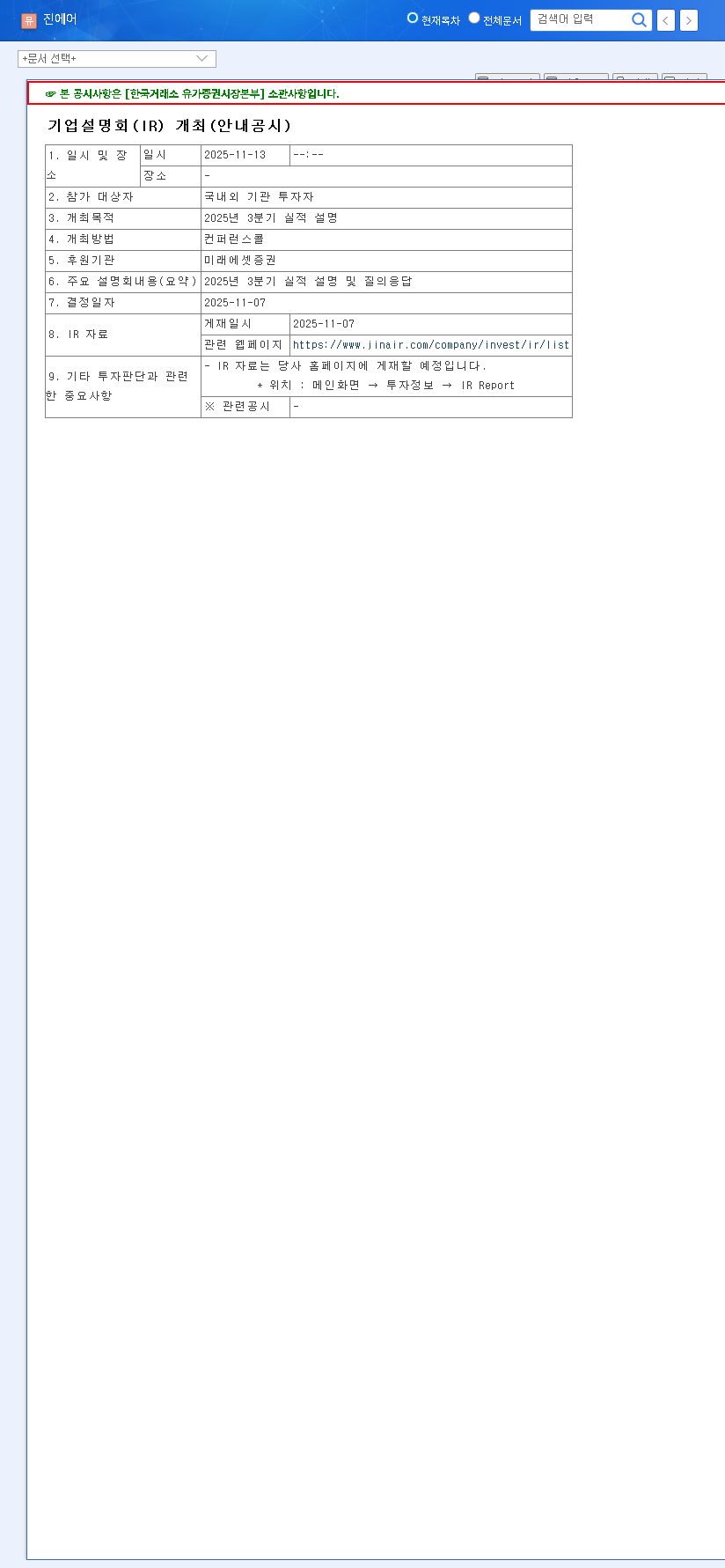

The latest Jin Air Q3 2025 earnings report for JIN AIR CO,.LTD. (272450) has sent a wave of concern through the investment community. After a promising turnaround earlier in the year, the preliminary Q3 results revealed a significant miss on all key metrics, plunging the company back into a loss. This downturn raises critical questions: Is this a temporary bout of turbulence, or does it signal a systemic issue within the competitive Low-Cost Carrier (LCC) market? This comprehensive Jin Air stock analysis will dissect the factors behind the earnings shock, evaluate the potential for recovery, and outline a clear Jin Air investment strategy for navigating the path ahead.

Breaking Down the Q3 2025 Earnings Shock

Jin Air’s preliminary Q3 2025 operating results fell dramatically short of consensus market expectations, marking a troubling second consecutive quarterly loss. These figures, released in the company’s Official Disclosure, paint a stark picture:

- •Revenue: KRW 304.3 billion (12.0% below the expectation of KRW 347.5 billion)

- •Operating Profit: KRW -22.5 billion (a staggering 249.0% miss from the expected profit of KRW 15.1 billion)

- •Net Profit: KRW -27.5 billion (a 341.0% deviation from the expected profit of KRW 11.4 billion)

This significant deterioration in profitability, especially when compared to the same period last year, suggests that multiple powerful headwinds are impacting the airline’s financial health.

A perfect storm of soaring operational costs, fierce price wars in the LCC market, and softening consumer demand created significant headwinds for Jin Air in Q3 2025, erasing earlier gains and raising concerns about the sector’s health.

Root Cause Analysis: Why Did Performance Decline?

The poor 272450 earnings are not the result of a single issue, but a convergence of challenging external and internal factors.

1. The High-Cost Structure Squeeze

Airlines are notoriously sensitive to macroeconomic volatility. For Jin Air, this was particularly acute. The continued strength of the US dollar amplified the cost of debt and aircraft leases, which are largely priced in foreign currency. Simultaneously, elevated global oil prices, as reported by leading financial news outlets, directly increased fuel expenses—the single largest cost for any airline. Compounded by domestic inflation driving up labor and operational costs, Jin Air’s fixed cost base became a significant burden on its bottom line.

2. Intensifying LCC Market Competition

The South Korean LCC market analysis reveals an environment of hyper-competition. With several carriers like Jeju Air and T’way Air vying for market share, price wars have become rampant. The aggressive discounting on popular routes to Japan, even during the peak summer travel season, severely eroded profit margins. While Jin Air succeeded in growing passenger volume, it came at the cost of profitability, indicating that the demand recovery was not strong enough to offset the cutthroat pricing environment.

3. Rising Financial Burdens

With a high debt-to-equity ratio, Jin Air is particularly vulnerable to changes in interest rates. The global trend of monetary tightening has increased the company’s interest expenses, adding another layer of financial pressure and constraining its ability to invest in growth or weather further economic shocks.

A Strategic Roadmap for Investors

Given the disappointing Jin Air Q3 2025 earnings, investors must adopt a cautious and strategic approach. Short-term volatility is likely, but long-term potential hinges on management’s ability to navigate these challenges.

Short-Term Strategy: Observe and Verify

In the immediate aftermath of this report, a ‘watch-and-see’ stance is prudent. The stock price will likely face downward pressure as the market digests the news. Avoid knee-jerk reactions and instead focus on monitoring management’s forthcoming response and any guidance they provide for Q4 and beyond.

Mid-to-Long-Term Checkpoints for Your Jin Air Investment Strategy

For a potential turnaround, investors should look for concrete evidence of strategic adjustments. For those learning how to analyze airline stocks, these are the key areas to watch:

- •Cost Control Initiatives: Look for announcements on enhanced fuel and currency hedging strategies. Is the company taking steps to improve aircraft operational efficiency and cut non-essential spending?

- •Route Profitability Focus: Is management re-evaluating its route network to prioritize high-yield destinations over volume? A shift away from heavily contested, low-margin routes would be a positive sign.

- •Synergy with Korean Air: As a subsidiary of Korean Air, Jin Air has a unique potential advantage. Watch for deeper integration, such as codesharing agreements, joint marketing, or operational synergies that could provide a competitive edge.

- •Macroeconomic Tailwinds: A sustained drop in global oil prices or a strengthening of the Korean Won against the US dollar would provide significant and immediate relief to Jin Air’s cost structure.

Conclusion: A Cautious Outlook for 272450

The Jin Air Q3 2025 earnings report is an undeniable setback that highlights the profound challenges facing not only the company but the entire LCC industry. While the stock is likely to face a period of bearish sentiment, a complete write-off would be premature. The path to recovery will be difficult and contingent upon disciplined cost management, smart strategic pivots, and a more favorable macroeconomic environment. For now, investors should remain diligent, closely monitoring the key checkpoints before committing further capital. The coming quarters will be critical in determining whether Jin Air can navigate this turbulence and regain altitude.